Sector Views: Monthly Stock Sector Outlook

Schwab Sector Views is our six- to 12-month outlook for stock sectors, which represent broad sectors of the economy. The Schwab Center for Financial Research (SCFR) combines a factor-based approach with a market and economic assessment to determine the ratings. For the basics on sectors, please see Stock Sectors: What Are They? How Are They Used?

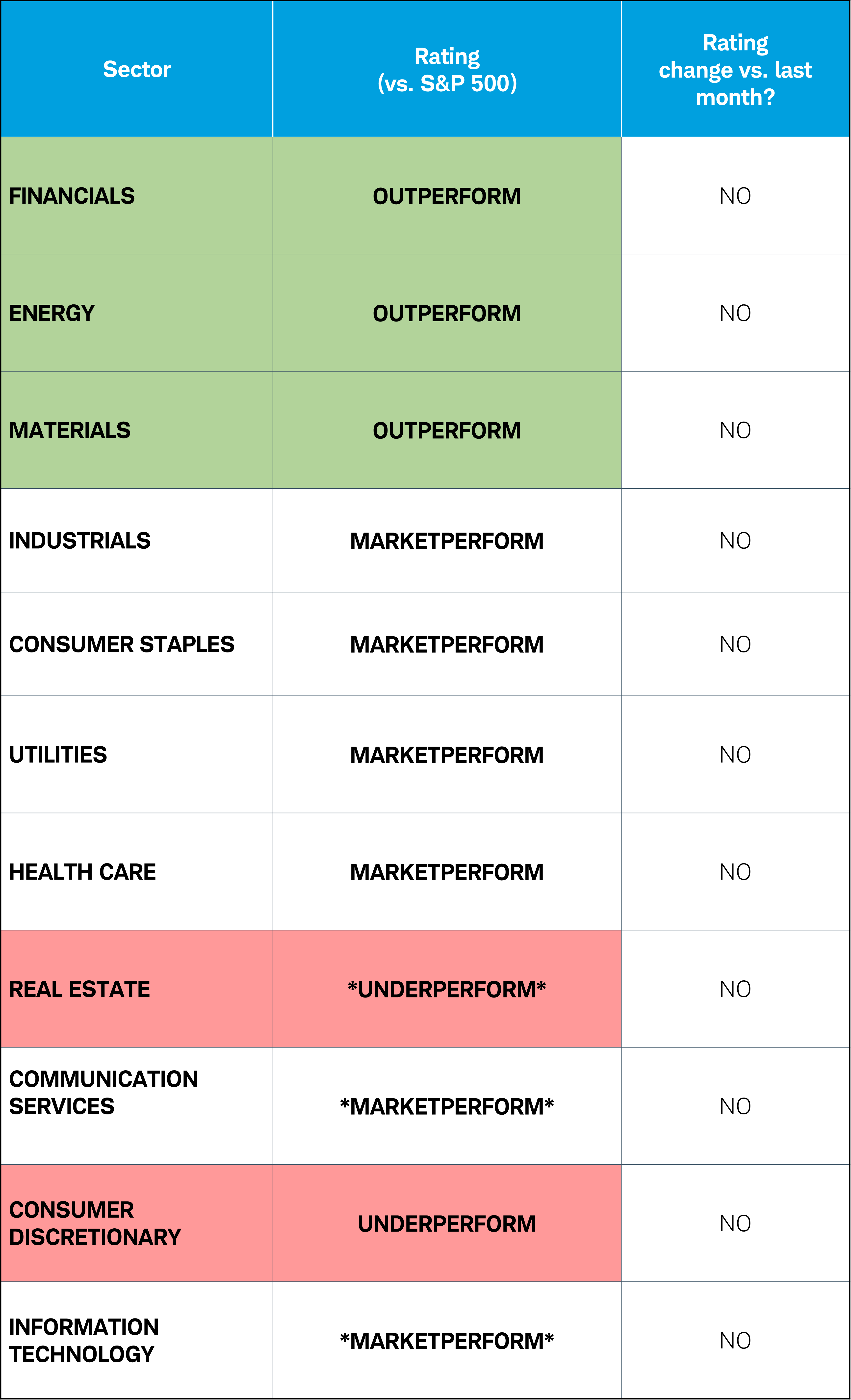

Sector views

Energy, Financials and Materials remain Outperform. Meanwhile, Information Technology is in last place based on factors, but we maintained our override and continue to rate it Marketperform. We believe its growth prospects are good and that the dominance of a few mega-cap stocks skews its factor-based position. Real Estate remains Underperform based on weak fundamentals, including high interest rates and still-rising vacancy rates. Communication Services slipped to ninth place, but as with Technology the dominance of a few stocks tends to skew its factor rankings.

Sector ratings

Source: Schwab Center for Financial Research, as of 4/15/2024.

The ratings Outperform, Marketperform, and Underperform reflect SCFR's opinions about the likelihood that the sector will perform better (outperform), about the same (marketperform), or worse (underperform) than the broader S&P 500®index during the next six to 12 months. Asterisks (*) mean that SCFR overrode the factor model in determining the rating. Sectors are based on the Global Industry Classification Standard (GICS®), an industry analysis framework developed by MSCI and S&P Dow Jones Indices to provide investors with consistent industry definitions. Sectors are listed in the above chart in order of their performance in five factors that are shown in the chart below. The information here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Investing involves risk, including loss of principal.

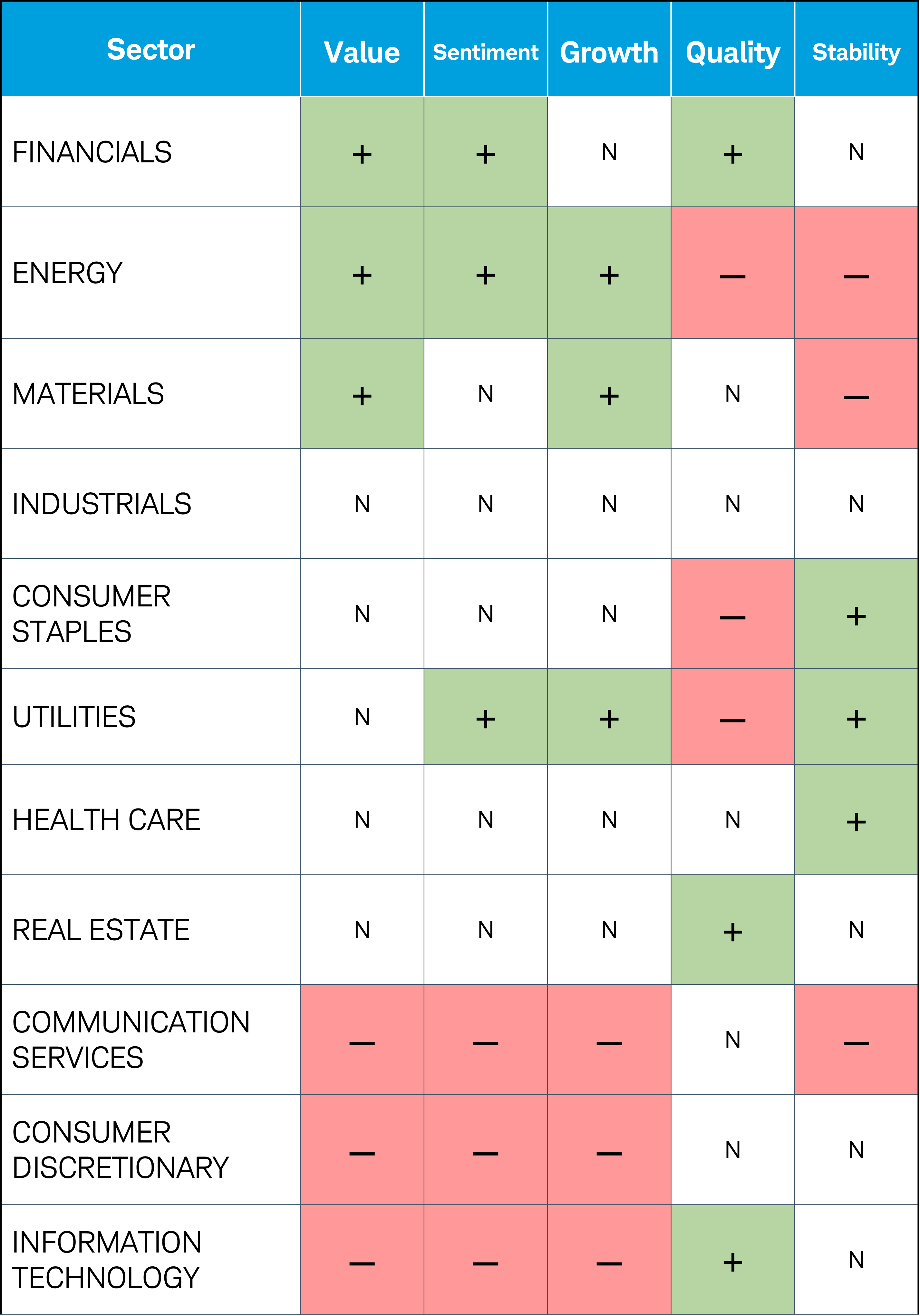

Factors behind the stock sector ratings

Source: Schwab Center for Financial Research, S&P Dow Jones Indices, as of 04/15/202424.

Sectors are ranked as positive (+), neutral (N) or negative (—) for each of the five factors based on the sector's relative ranking (from 1-11) in each factor: 1-3 is positive, 4-8 is neutral, and 9-11 is negative. See Important Disclosures for an explanation of the Value, Growth, Quality, Sentiment and Stability factors and their inputs. The Schwab Center for Financial Research reserves the right to override the Schwab Sector Views Model; see "Sector Views Process" below for an explanation of how SCFR determines its ratings.

Sector performance

| Sectors (in alphabetical order) | Weighting in S&P 500 (%) | Trailing six-month performance (%) | Trailing 12-month performance (%) |

| Communication Services | 9.0 | 25.7 | 52.1 |

| Consumer Discretionary | 10.3 | 14.4 | 30.7 |

| Consumer Staples | 6.0 | 13.4 | 2.4 |

| Energy | 3.9 | 11.5 | 14.5 |

| Financials | 13.2 | 22.1 | 26.6 |

| Health Care | 12.4 | 8.3 | 5.5 |

| Industrials | 8.8 | 20.9 | 25.6 |

| Information Technology | 29.6 | 24.6 | 48.5 |

| Materials | 2.4 | 16.6 | 13.8 |

| Real Estate | 2.3 | 10.4 | 3.4 |

| Utilities | 2.2 | 11.5 | -4.5 |

| S&P 500 index performance for the trailing six or 12 months (%) | 18.7 | 27.2 |

Stock sector commentary

(Sectors are listed in alphabetical order)

Communication Services sector (rating: Marketperform)

Positives: Communication Services relies heavily on advertising and subscription-type revenue, which tends to rise when the economy is expanding.

Risks: The sector may underperform if economic growth slows. A persistent risk is the dominance of bigger members, which command a large share of the sector's market cap and thus determine much of its performance.

Consumer Discretionary sector (rating: Underperform)

Positives: Companies tend to be sensitive to economic activity, as consumers buy discretionary items more readily when job growth is strong and interest rates are low.

Risks: Concentration risk is high for the sector, with the two largest members accounting for nearly half of the total market cap The other half of the sector is also at risk of any further softening in consumer spending and/or income growth.

Consumer Staples sector (rating: Marketperform)

Positives: Consumer Staples companies tend to be relatively insensitive to economic activity, as consumers buy staples regardless of economic conditions.

Risks: Companies can face shrinking profit margins in an inflationary environment without the pricing power to offset higher costs. Weaker earnings growth has made these stocks look expensive relative to the broader market.

Energy sector (rating: Outperform)

Positives: Energy stocks are generally supported by relatively high oil prices. The sector has exhibited high-quality aspects given a relatively high interest coverage ratio—that is, companies are relatively well-positioned to pay interest due on outstanding debt—and a still-strong level of earnings.

Risks: Earnings growth might struggle if oil prices continue to fall on the heels of both relatively weak demand and a continued recovery in supply.

Financials sector (rating: Outperform)

Positives: Some segments benefited from rising interest rates, which allow banks to lend at higher rates and insurance companies to increase returns on collected policyholder premiums. The economy has proven to be relatively resilient in the face of one of the most aggressive tightening cycles in history.

Risks: It is still too soon to tell whether long and variable lags associated with monetary policy should be ignored, which means the economy is not yet out of the woods. With significant tightening in the pipeline amid the fallout from last year's banking issues, Financials' profits trajectory might struggle relative to the broader market, which can weaken the earnings profile of the sector.

Health Care sector (rating: Marketperform)

Positives: Health Care tends to do well even when economic growth slows, as most people will find a way to pay for necessary health care treatment even during tough economic times (although elective procedures often decline). It also can get a boost when heightened market volatility drives investors toward stabler choices.

Risks: Several companies in the sector (particularly in the biotechnology industry) have weak fundamentals. Downward pressure on earnings estimates is helping lift multiples—that is, stock price relative to earnings—especially for risky industries like biotechnology, which is a risk as interest rates stay elevated.

Industrials sector (rating: Marketperform)

Positives: Industrials often benefit when economic growth raises business confidence, resulting in new building projects, machinery purchases, increased airline travel and shipments.

Risks: Industrials may underperform in the aftermath of rate-hike cycles as investors anticipate that higher inflation and borrowing costs can begin to undercut business and consumer spending.

Information Technology sector (rating: Marketperform)

Positives: Information Technology tends to do well when strong economic growth encourages companies to invest in technology upgrades and consumers to buy new devices. Some of the larger members are not in the "long-duration" camp—companies expected to produce their highest cash flows in the future—given they have current earnings growth and strong cash positions.

Risks: Many companies in the sector trade at higher multiples (price relative to earnings), and a rising-interest-rate environment puts downward pressure on valuations. Heavyweights in the sector are associated with the "stay-at-home" group that did well during the pandemic shutdown, but may face pressure as investors broaden their focus toward other stocks.

Materials sector (rating: Outperform)

Positives: The Materials sector historically is sensitive to fluctuations in the global economy, the U.S. dollar, and inflationary pressures. In a less-severe recession, the sector's profitability might not take as large of a hit.

Risks: Stocks tend to underperform during rate-hike cycles as investors anticipate that higher inflation and borrowing costs will undercut business spending. Materials relies heavily on foreign demand, and a stronger U.S. dollar tends to weaken sales abroad.

Real Estate sector (rating: Underperform)

Positives: Real Estate, which consists primarily of commercial real estate investment trusts (REITs), tends to benefit from economic growth, which supports rent collections and property prices.

Risks: Most REITs borrow heavily, making them vulnerable to high interest rates. The longer-term outlook for real estate is in question given uncertainty about a full post-COVID return to offices and major metro areas.

Utilities sector (rating: Marketperform)

Positives: The Utilities sector has tended to perform relatively better when economic growth slows, as consumers usually cut spending on other items before they stop paying utility bills.

Risks: The sector is heavily indebted, especially relative to cash flow. Economic data have come in better than expected. Higher Treasury yields can lessen the attractiveness of Utilities stocks, which tend to pay relatively high dividends, because investors can get similarly high yields elsewhere.

How we evaluate stock sectors for this outlook

We begin with a data-driven evaluation of each of the 11 equity sectors based on five factors—Growth, Quality, Sentiment, Stability and Value. Multiple data points are used in this analysis, including estimated and historical dividend growth, cash flow, revenue per employee, price momentum, analyst price target revisions, sales growth variance, trading volume turnover, change in short interest, and the forward price-to-earnings ratio, which divides the share price by the estimated future earnings of the company.

The sectors are then evaluated relative to the S&P 500 index to arrive at one of three preliminary ratings: Outperform, Marketperform and Underperform. Once confirmed, these ratings will reflect our view of how the sector is likely to perform relative to the S&P 500 during the coming six to 12 months.

The Schwab Center for Financial Research bases its ratings approval on a combination of the quantitative model and a qualitative perspective on what's happening in the economy and markets. For example, there may be times when the model points toward a rating based on recent data, but SCFR's experts have strong reason to believe that an economic, market or geopolitical shift is underway that would change the sector outlook. In that case, SCFR may override the model.

How should I use Schwab Sector Views?

Investors should generally be well-diversified across all stock market sectors. You can use the S&P 500 allocations to each sector, listed in the Sector Performance chart above, as a guideline.

Investors who want to make tactical shifts in their portfolios can use Schwab Sector Views' Outperform, Underperform and Marketperform ratings as a resource. These ratings can be helpful in evaluating and monitoring the domestic equity portion of your portfolio.

Schwab clients can log into their accounts and use Schwab's Portfolio Checkup tool to help assess their sector allocations. If they decide to make adjustments, they can use the Stock Screener to research particular sectors. Schwab's ETF Screener and Mutual Fund Screener also can help identify funds that specialize in particular sectors. Investors and clients should consider this as only a single factor in making their investment decision while considering the current market environment.