Listen on Apple Podcasts, Google Podcasts, Spotify or copy to your RSS reader.

Can You Invest in Crypto Without Buying Crypto Directly?

For investors looking to gain exposure to the crypto space, what are some alternatives to buying crypto directly?

MARK RIEPE: As I record this episode, a story that's been dominating the news is the collapse of another cryptocurrency-related company. In this case it’s the cryptocurrency exchange FTX.

The story got me thinking about how certain investments, strategies, or sometimes the people behind them become incredibly popular and generate enthusiastic followers.

Today, we're going to be exploring some of the psychological factors behind this phenomenon and then talk about investing in cryptocurrency in general and the companies that are associated with it and its underlying technology.

I'm Mark Riepe, and this is Financial Decoder, an original podcast from Charles Schwab. It's a show about financial decisions and the cognitive and emotional biases that can cloud our judgment.

Cryptocurrencies have been around for about 10 years now, but their popularity as an investment spiked in the last few.[1]

In fact, as of April 2022, one survey found that more than 80% of crypto investors had only been investing in crypto for two years or less.1

At least five factors contributed to this surge in popularity.

- The first was availability. More exchanges were offering ways to invest in cryptocurrency and the crypto economy.

- Second, it was easier to use cryptocurrencies as a method of payment. Not only that, but retailers were using their acceptance of cryptocurrencies as a way of showing how hip they were.

- Third, governments around the world began studying the idea of officially sanctioned digital currencies and in some cases actually creating them.

- Fourth, the underlying technology of the blockchain started to grow considerably as companies studied all kinds of applications for it beyond currencies.1

- But the fifth factor, and in my opinion by far the most important one, was the surge in investment performance of cryptocurrencies and related investments.

In my experience, when any type of investment, not just cryptocurrencies, performs well, it will attract attention, and with the advent of social media and the 24-hour news cycle, it is easier than ever to spread the word.

When the happens, investors want to get in on the action. In short, investors get FOMO, or fear of missing out. I don’t think FOMO is a new phenomenon, as there are many history books that have chronicled investment manias going back centuries. But the term itself seems to date back to 2004, according to the World Journal of Clinical Cases.[2]

An instructor of psychology at Harvard, Natalie Christine Dattilo, says, "FOMO includes both the perception of missing out, which triggers anxiety, and compulsive behaviors, like checking and refreshing sites, to maintain social connections. It is closely related to the fear of social exclusion or ostracism, which existed long before social media."[3]

That point is important. FOMO isn’t a new thing that’s driven by social media. It taps into fundamental human emotions. Social psychologist and associate professor at the University of Oklahoma Erin Vogel summed it up well when she said that "Humans want to feel like we're included, like we belong to a group." 3

And that makes sense. Back when we were all hunter-gatherers, belonging to a group was vital to survival. This wiring in our brains that used to literally keep us alive triggers our "fight or flight" response, according to Dr. Dattilo.3

Today, while we don't have to be in a group at all times merely to stay alive, feeling bonded to other people combats feelings of stress. 3 In the case of FOMO and cryptocurrency, it's not much of a stretch to say that some people want to feel that they're part of an exclusive, successful group. One difficulty with this is that word "successful."

Social media adds fuel to the fire because, for the most part, people who have been or are investors usually only talk about investments when they’ve been successful.

As Dr. Vogel put it, "Especially in the age of social media, it's important to remind ourselves that other people's lives aren't as exciting or as perfect as they may seem." 3

This is especially important when it comes to hot investments. In many cases, the big money to be made happens early. By the time the masses jump in, the future returns to be had can often be modest or even non-existent if the price you paid to get in was at or near the top, and future prices returned to earth. In other words, we can learn a lot by looking at the past, but what ultimately matters is the future.

Joining me now is Inga Rachwald. Inga is a senior portfolio strategist supporting Schwab Asset Management here in San Francisco. Inga, thanks for being here today.

INGA RACHWALD: Thanks for having me, Mark.

MARK: Inga, many folks probably first learned about Bitcoin when it shot up in price in 2017, and then in 2021, another big bull run, not only in Bitcoin but in other cryptocurrency prices, and a lot of crypto ads during the Superbowl. Actually, though, you know, as we’re recording this, prices are way down from those peaks we saw earlier in the year. And while we did an episode in 2021 on some of the basics of cryptocurrency, maybe let’s just start out this episode by having you give us some background on crypto from your point of view. What are some of the basics that people need to understand?

INGA: So cryptocurrencies are digital assets, or currencies, that can be exchanged between parties, but without the use of a third-party intermediary, like a bank or payment processor to verify the transaction. The crypto part refers to the various encryption algorithms and cryptographic techniques that support cryptocurrency. A simple way I like to think about cryptocurrency is a group of like-minded individuals who come together and agree to follow certain standards or protocols for recording payments using a technology called blockchain, which we’ll talk a little bit more about in a bit, that removes the need to have an intermediary verify that transaction. So Bitcoin follows a certain protocol, for example. Ethereum, which is the second largest cryptocurrency, follows another protocol, etc.

Before cryptocurrency came to be, you had what was called the double-spend problem for digital currency. So if I had $100 in digital currency, I could spend it more than once, unless I had an intermediary, like a bank, to verify the transaction. With the technology that powers cryptocurrency, that verification of me spending that $100 can be done without an intermediary and is deemed to be difficult to falsify.

The cryptocurrency landscape is vast. People may be surprised to know that there are well over 10,000 types of cryptocurrencies that have various use cases. Bitcoin is the largest and most familiar, but there are other cryptocurrencies. For example, some called stablecoins, the largest of which is Tether, which seek to peg to fiat currency, like the U.S. dollar. And then there’s what’s called central bank digital currency, which is technically not a cryptocurrency because it would be managed by an intermediary, central bank in this case, and it is a fiat currency like the U.S. dollar, simply in digital form. This is something many countries around the world have adopted or are considering adopting in the future, with the U.S. being one of those countries considering that.

MARK: Tell me a little bit about why this was created in the first place. Why did crypto emerge? What kind of problems was it designed to solve?

INGA: Sure. Cryptocurrency’s existence really stemmed from this perceived mistrust of banks, government, other intermediary institutions, particularly following the '07-'08 U.S. financial crisis. But it also originated from a view that technology could make digital asset transactions faster and cheaper. For example, take cross-border transactions where someone wants to send money from the U.S. to another country. It’s pretty costly today to do so, and it is quite slow even if you’re going through a bank or a payment application. For example, I have family overseas, and I, you know, have a bank account. When I’ve sent money overseas, it’s been fairly expensive, and it took it several days to settle. So cryptocurrency is designed to make that transaction simpler and cheaper than sending fiat currency, but also keeping it secure.

MARK: I think in a lot of cases we actually take access to the financial system for granted in some respects. And I think that your example kind of illustrates that. Are there any other examples like that?

INGA: Definitely. The unbanked population, so simply someone who does not have a bank account. Globally, about 60% of adults have a bank account, but that leaves nearly two billion people who do not. But of those people who do not have a bank account, most do have access to a mobile phone, so they can make online payments. So for someone who doesn’t have a bank account, cryptocurrency can be a particularly appealing option for sending money or making payments. Cryptocurrency doesn’t care about your credit score, where you live. So enthusiasts like that democratization aspect of it.

MARK: Tell me about just sort of international adoption of this type of currency. You know, some countries have been talking about kind of adopting it, actually, as their currency. What can you tell me about that?

INGA: Yeah, overseas, I mean, El Salvador is an example where some 70% of the country doesn’t have a bank account, and they are heavily reliant on money sent home from family working overseas. So Bitcoin was actually adopted as legal tender to facilitate money transfer.

Bitcoin has also seen popularity in third-world countries where there’s persistently high inflation challenges. So take Venezuela, for example. the country’s experienced inflation so high that the local currency was actually devalued to the point where it became almost worthless. So Bitcoin, even with its volatility, was viewed as a more stable option.

MARK: Inga, you mentioned earlier that cryptocurrencies, they’re taking advantage of this blockchain technology, and I think people have, you know, probably heard that term before, companies are starting to use it for various applications. But before we dive into that, could you just kind of explain in a little bit more detail, the difference between blockchain and crypto? How are they the same? How are they different?

INGA: Sure. Sure. Blockchain is the technology that records the cryptocurrency transaction among individuals. It’s really a shared database of who sent the money to whom, how much, what time. If you think about those inter-office envelopes some of us may still use to send documents internally, with the red twisty string around it, that show the name of the sender, the name of the recipient, blockchain kind of functions the same way. But it’s obviously executed via a network of computers. The goal of blockchain is to allow that digital information to be recorded and distributed, but not edited, so you can’t go back and change the information, and that’s how you remove the intermediary from the equation. Different currencies use blockchain differently, which is how you arrive at those different use cases. So Bitcoin’s use case is to, essentially, function as money.

Ethereum, which is the second largest cryptocurrency, also has a component that functions like money, but that’s not its core goal. Ethereum’s use case is designed to support other services like decentralized applications, smart contracts, which are agreements between parties on areas like insurance, lending, ownership claims, and also what are called non-fungible tokens, or NFTs. These can take the form of art or music, for example, and are coded to be unique.

And the processes used to validate transactions on the blockchain also vary. Bitcoin uses what’s called a proof-of-work component to validate a transaction, and this requires a massive expenditure of computational energy. People might be interested to know that annually the process of creating Bitcoin consumes more energy than is used by the country of Finland, which is a nation of about five and a half million people. Ethereum uses what’s called a proof-of-stake mechanism to validate transactions, and it’s deemed much more energy-efficient relative to that proof-of-work approach.

So the takeaway here is that blockchain as a technology has other applications beyond simply supporting cryptocurrency as digital currency. Because the transaction is viewed as difficult to alter, you have companies now like Walmart or Home Depot who have started to use blockchain technology to manage their supply chains. Some people believe that smart contracts could replace a lot of the manual paper-based contracts we go through today. Think about all the paperwork and legal components required to purchase a house and prove ownership, for example. Blockchain is a potential path to digitizing these types of contracts in a secure way.

MARK: Inga, let’s talk a little bit about how to actually invest in this space, in cryptocurrency. Certainly, one way is to open an account on a crypto exchange, which have been in the news quite a bit lately as we’re recording this, and just kind of own it directly. But there are other indirect ways for people to get exposure, as well. So let’s start with crypto ETFs. How do they work?

INGA: At the time of recording, there are no ETFs in the United States that are able to hold cryptocurrencies directly. With crypto-related ETFs, there are generally two main types. The first being a futures-based ETF that invests in Bitcoin futures contracts, for example. Unlike cryptocurrencies, which remain largely unregulated, futures trade on the commodity exchanges registered with the CFTC, the Commodities Futures Trading Commission. While these ETFs provide somewhat of a direct exposure to Bitcoin, it's important to remember futures ETFs have to renew or roll forward their contracts regularly. So, if the longer futures price is higher than the expiring contract on the date of renewal, that difference can eat into funds returns. Then you have equity ETFs. These tend to invest in stocks of companies involved in the cryptocurrency space, areas like cryptocurrency miners, investors, or exchanges. And then there are some ETFs that invest more broadly in, for example, anything that involves blockchain technology.

MARK: There are a couple of other ways that … people may have heard of trusts and owning futures contracts directly, as opposed to going through an ETF that then owns those. So let’s start with trusts—how do those work?

INGA: Sure. Trusts participate in cryptocurrency markets through a closed-end structure that owns the underlying cryptocurrency, like Bitcoin, and attempts to track the price of the specific cryptocurrency. Since these are publicly traded trusts that report to the U.S. Securities and Exchange Commission, there is that element of regulatory oversight of the investment vehicle, and it can mitigate investor concerns about storing cryptocurrency, custody of it, and the security of that versus owning cryptocurrencies outright. The challenge is these trusts can trade at a premium relative to underlying value of the cryptocurrency. They can also be quite expensive and subject to lockup periods, often of six months or more.

MARK: By expensive you mean the expense ratio that the company charges for running the trust, is that right?

INGA: Exactly.

MARK: And let’s talk about directly owning a futures contract. There are a number of futures contracts listed, for example, or their prices tied to Bitcoin. How do those work, and how do they differ from owning an ETF that owns futures contracts?

INGA: When you buy and sell Bitcoin futures contracts, you speculate on Bitcoin’s future price. It’s like two parties coming together and betting where one thinks Bitcoin will go up in price in the future, and the other bets that Bitcoin will decline in price. The person who gets it wrong pays the other party a cash settlement, which can be quite large. So futures can be pretty risky and expensive. Some investors like the futures format because unlike the largely unregulated cryptocurrency space, futures in the U.S. are regulated by the Commodities Futures Trading Commission.

MARK: Inga, so we’ve talked a lot about these kind of different approaches that are indirect, you know, not owning the actual cryptocurrency directly. So maybe just kind of sum it up for us. What are some of the advantages and what are some of the disadvantages of going the indirect method?

INGA: Sure. Indirect approaches like equity ETFs that hold a basket of stocks may offer a more diversified and potentially less volatile path than direct ownership of a cryptocurrency or if you were to try to hand-pick two or three stocks associated with the cryptocurrency space yourself. The disadvantage is that equity ETFs may not necessarily correlate to the crypto or Bitcoin movement, price movement, so you may not get that direct play on cryptocurrency that you might be looking for. This is where you really have to do your research because these equity ETFs differ. Some invest in anything related to blockchain, for example, which is the technology, again, that underlies cryptocurrency. So you could have a consumer company like Walmart, which relies on blockchain for its supply chain needs, but it’s not necessarily in the cryptocurrency business. Other equity ETFs look for companies with a lot of exposure to the cryptocurrency economy. For example, you might be surprised to know that companies like Overstock.com. I think about buying towels or light fixtures from there, but they have been accepting Bitcoin as payment since 2014. MicroStrategy is another example. It’s a software company unrelated to the cryptocurrency business, but they hold billions of dollars worth of Bitcoin on their balance sheet. So you may get more correlation or exposure to Bitcoins with companies like these if that’s your end goal. At the end of the day, we really don’t know which cryptocurrency or related company may or may not do well, so owning more than one company or cryptocurrency could be a good path for clients who want that exposure, but don’t necessarily want to bet on one component of the space.

MARK: Yeah, so, essentially, a diversification argument, right? At the end of the day, it’s very hard to predict these things, but if you think the whole area will do well, a diversified approach will give you better odds of success.

INGA: Precisely.

MARK: So how do you see kind of crypto fitting into someone’s portfolio? What kind of role does it play?

INGA: Cryptocurrency is still a speculative space for investors, particularly since they’re not regulated by any central bank or government, and, instead, operate on a decentralized network. The more direct approaches to investing in Bitcoin—be it direct ownership, futures ETFs, or trusts—are tied to one underlying cryptocurrency, and, as such, they can be incredibly volatile and subject to … subject the investor to substantial losses.

Some of those indirect approaches, like equity ETFs that, instead, hold a basket of stocks related to the cryptocurrency economy can serve as a complement to a client’s core diversified portfolio, but as a very small portion, and knowing that that allocation could still be risky and volatile.

From an asset allocation perspective, some crypto enthusiasts have touted crypto as a hedge to inflation or as a low correlation to the broad equity market. And while there have been short periods where some of these trends have borne out, they’ve since reversed course. So these points, frankly, need more time to study.

MARK: Inga, you mentioned regulation and how the kind of crypto space is largely unregulated right now. Do you think that’s sustainable? Do you think that’s going to change or maybe play out in a different way? Will Bitcoin and other cryptocurrencies end up being regulated just like other securities or maybe like other types of asset classes that people invest in?

INGA: Regulation, for sure, is the big open question, and clarity for regulators that pave the way for investor protection could be a path to future adoption. The current regulation for cryptocurrencies vary from country to country. Some countries have put an outright ban on cryptocurrencies, while others have allowed them, but with certain restrictions. Within the United States, there are a lot of options on the table at the moment when it comes to cryptocurrency. Biden issued an executive order in March of 2022 for regulators to develop a framework to oversee the cryptocurrency market and assess which regulatory body or bodies will take the lead in that endeavor. The U.S. Securities and Exchange Commission, the SEC, says it views cryptocurrencies as securities and will apply existing securities laws to digital assets. On the other hand, the Commodities Futures Tradition Commission, or CFTC, classifies Bitcoin and Ethereum as commodities. So there is still some debate as to whether regulation will come from the FTC or the CFTC or both.

MARK: Yeah, and I think that uncertainty, I think in a lot of ways, that kind of pervades the whole history of … the whole history of this space has been, you know, a lot of evolution, things changing, a lot of volatility. So maybe just let me ask you kind of a big picture question: What do you think is next for crypto?

INGA: There is no question that cryptocurrency has been highly volatile. We've seen this crypto winter experienced in 2022. And although there are well over 300 million crypto users globally, and it’s estimated that around 15% of U.S. adults own digital assets, there are still a lot of elements for investors and regulators to work through. The regulatory piece is probably the biggest one. Many people view that oversight, transparency, investor protection—largely achieved through regulation—as really the only way crypto can attain legitimacy in mainstream finance and society.

And then there’s blockchain. The technology, as we talked about earlier, has many applications outside of just supporting cryptocurrency. So that’s an area to watch, as well.

MARK: Yeah, I think that’s especially important. Any time there’s a big innovation, the initial use case is not necessarily … you know, ends up being kind of the most important use case as that innovation kind of weaves its way throughout society.

So last question for you. What advice do you have for someone who, maybe they’ve been thinking about investing in crypto. Maybe they’ve listened to this podcast. They’ve heard all the different … very different ways of participating in this. They’re a little overwhelmed by it all, but they’re still interested. What do you tell them? What should they do next?

INGA: Sure. There’s no question that the choices can be overwhelming in this space, and investors need to be aware of certainly the volatility in this space, as well. You definitely want to sort out whether you’re looking for more of a direct ownership approach, whether that be a trust- or a futures-based approach, or do you want to invest in a strategy that takes into account the broader set of cryptocurrencies or blockchain-related stocks? If it’s the latter, a few things there. Understand the strategies of crypto-economy exposure. Is it targeting blockchain technology companies or crypto-related companies? Second thing, understand the selection and weighting process. Is it actively managed? Is it passively managed? How is it weighting the securities within that portfolio? And then, last, compare costs, expense ratios. The cost of these funds can really significantly vary, so you do want to know what plays into your portfolio.

MARK: Inga Rachwald is a senior portfolio strategist for Schwab Asset Management in San Francisco. Inga, this has been great. Thanks for being here today.

INGA: Thanks for having me, Mark.

MARK: In addition to all the great points Inga made, I'd like to add a few issues to emphasize.

Number one: You should always understand what you're investing in.

Before your put your hard-earned savings into a digital currency, a company that makes money from exchanging currencies, or an account that promises high rates of return, ask yourself a few questions. Do you know how the technology works? Do you know how the sponsor of the investment makes money? What are their legal obligations toward you as an investor? What role is the asset playing in your portfolio? How would your portfolio be affected if the price went to zero?

A related point is to trust your instincts. I know it’s a cliché, but if something seems too good to be true, it probably is. The good news about the information revolution is that there’s plenty of information out there. Look for it, evaluate it, and use it when it makes sense.

Make sure you understand where that information is coming from, and be sure to seek out sources who take a skeptical view of whatever it is that you’re considering.

Second, I talk a lot about diversified portfolios on this podcast because they have proven to be an effective way to invest over the years. Diversification of asset classes, asset types, and strategies can generally protect you from the volatility associated with investing in only one asset type.

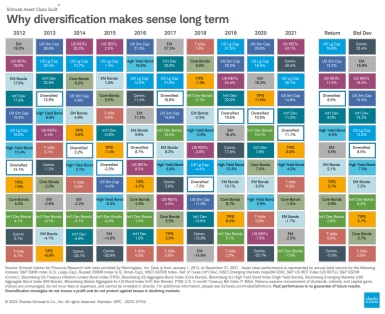

At the Schwab Center for Financial Research, we produce a lot of charts, and one is called the quilt chart. I've got a link to it in our show notes.

For each calendar year, it shows how each asset class performs. Each asset class has a box with its own color, and its return is typed into the box, and we stack the boxes from highest to lowest for each calendar year.

What the chart shows is that over the long run, there's no discernible pattern to the rotation among the top performers.

That’s where the name "quilt chart" comes in. When you look at all these years, the colors or asset classes are all over the place, and it looks like some crazy quilt. The point we’re trying to make for investors is that trying to catch the wave of any asset is almost impossible.

But having a broad array of investments in your portfolio means that in most years, some will vastly outperform the others, but the portfolio overall will end up with a smoother ride.

Lastly, crypto is still considered to be an emerging field. There are plenty of technology issues to be sorted out, legal structures for different types of investments, and plenty more companies to rise and fall. It also wouldn’t surprise me if there are new use cases for the underlying technology.

As these developments unfold, don’t recklessly charge ahead, and ignore or arrogantly dismiss all the warning signs or doubters. Listen to the evangelists as well as the doubters.

And don't let your emotions carry you away with the crowd. Ask yourself what could go right with any investment, but also what could go wrong, and compare both sets of possibilities against your goals as an investor that are enumerated in your financial plan.

If you'd like to learn more about investing in crypto at Schwab, check out Schwab.com/Cryptocurrency.

That site lists a number of cryptocurrency coin trusts, crypto stocks, and other ways you can get exposure to crypto without buying crypto directly.

Thanks for listening. And if you've enjoyed the show, please leave us a review on Apple Podcasts.

We'd also love a personal recommendation, so if you know someone who might like the show, please tell them about it and how they can follow us for free in their favorite podcasting app.

If you prefer your podcasts on YouTube, we have some of our previous episodes posted there, as well.

And if you want more of the kinds of insights we bring you on Financial Decoder about how to improve your financial decisions, you can also follow me on Twitter, @markriepe, m-a-r-k r-i-e-p-e.

I’ve also been doing more posting on LinkedIn recently, so feel free to follow me there as well.

This is our last episode of our regular season, but we do have one more bonus for you before the year is out. Stay tuned for our 2023 Market Outlook episode, coming later in December.

For important disclosures, see the show notes and Schwab.com/FinancialDecoder.

[1] Csiszar, John, "6 Reasons Crypto Has Become So Popular in the Past Two Years," GO Banking Rates, Nasdaq.com, June 1, 2022, https://www.nasdaq.com/articles/6-reasons-crypto-has-become-so-popular-in-the-past-two-years

[2] Gupta, Mayank, and Sharma, Aditya, "Fear of missing out: A brief overview of origin, theoretical underpinnings and relationship with mental health," World Journal of Clinical Cases, July 6, 2021; 9(19):4881-4889, Fear of missing out: A brief overview of origin, theoretical underpinnings and relationship with mental health - PMC (nih.gov)

[3] Laurence, Emily, "The Psychology Behind the Fear of Missing Out (FOMO)," Forbes, September 30, 2022, https://www.forbes.com/health/mind/the-psychology-behind-fomo/

Investors should consider carefully information contained in the prospectus or, if available, the summary prospectus, including investment objectives, risks, charges, and expenses. Please read it carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including risk of loss.

Fiat curency is a government-issued currency that is not backed by a commodity such as gold.

Digital currencies, such as Bitcoin, are highly volatile and not backed by any central bank or government. Digital currencies lack many of the regulations and consumer protections that legal-tender currencies and regulated securities have. Due to the high level of risk, investors should view Bitcoin as a purely speculative instrument.

Virtual Currency Derivatives trading involves unique and significant risks. Please read NFA Investor Advisory – Futures on Virtual Currencies Including Bitcoin and CFTC Customer Advisory: Understand the Risk of Virtual Currency Trading.

Charles Schwab Futures and Forex LLC is a member of NFA and is subject to NFA’s regulatory oversight and examinations. However, you should be aware that NFA does not have regulatory oversight authority over underlying or spot virtual currency products or transactions or virtual currency exchanges, custodians, or markets.

You should carefully consider whether trading in virtual currency derivatives is appropriate for you in light of your experience, objectives, financial resources, and other relevant circumstances.

Please note that virtual currency is a digital representation of value that functions as a medium of exchange, a unit of account, or a store of value, but it does not have legal tender status. Virtual currencies are sometimes exchanged for U.S. dollars or other currencies around the world, but they are not currently backed nor supported by any government or central bank. Their value is completely derived by market forces of supply and demand, and they are more volatile than traditional fiat currencies. Profits and losses related to this volatility are amplified in margined futures contracts.

Currencies are speculative, very volatile, and not suitable for all investors.

Futures trading involves a high level of risk and is not suitable for all investors.

This information does not constitute and is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific advice is necessary or appropriate, Schwab recommends consultation with a qualified tax advisor, CPA, financial planner, or investment manager.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

All corporate names are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Diversification and asset allocation strategies do not ensure a profit and do not protect against losses in declining markets.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Correlation is a statistical measure of how two investments have historically moved in relation to each other, and ranges from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated.

Schwab Asset Management™ is the dba name for Charles Schwab Investment Management, Inc. Schwab Asset Management and Schwab are separate but affiliated companies and subsidiaries of The Charles Schwab Corporation.

Google Podcasts and the Google Podcasts logo are trademarks of Google LLC.

Spotify and the Spotify logo are registered trademarks of Spotify AB.

Apple Podcasts and the Apple logo are trademarks of Apple Inc., registered in the U.S. and other countries.

The cryptocurrency landscape is vast. There are well over 10,000 types of cryptocurrencies. For investors who are looking for exposure to this space, are there indirect opportunities that might reduce some of the risk? In this episode, Mark Riepe is joined by Inga Rachwald, a senior portfolio strategist for Schwab Asset Management. They discuss the development of various crypto and blockchain technologies, various use cases for specific cryptocurrencies, and financial instruments available to investors looking for indirect exposure.

Follow Financial Decoder for free on Apple Podcasts or wherever you listen.

Financial Decoder is an original podcast from Charles Schwab.

If you enjoy the show, please leave us a rating or review on Apple Podcasts.

Below is the asset class quilt chart that Mark refers to in the conclusion of the episode.