Calculating Risk on Vertical Options Spreads

Option traders will sometimes trade a consistent quantity when initiating vertical spread trades. Although this method keeps the contract numbers orderly, it ignores the fact that each vertical spread has a different risk profile based on a few considerations:

- Is it a debit spread or a credit spread?

- How wide is the spread (the difference between the strikes)?

- How much did you pay (for a debit spread) or collect (for a credit spread)?

With this information, you can determine the amount of risk and potential reward per spread. After that, we'll show you how to choose your trade size by looking at a trade's risk parameters in the context of your overall portfolio risk.

Remember the multiplier: For the examples below, remember to multiply the options premium by 100, the multiplier for standard U.S. equity options contracts. An options premium of $1 is really $100 per contract.

Debit spread

When placing a debit spread, the risk amount is the price of the spread plus any transaction costs. The potential reward equals the spread width minus the debit price and transaction costs. For example, let's look at a spread using XYZ. This spread includes the purchase of the 40-strike call and the sale of the 42-strike call of the same expiration date (the "XYZ 40-42 call vertical" in trader parlance). Let's assume a trade price of $0.60.

In this scenario, the risk amount would be $60 per spread. The potential reward would be the difference (spread width) between the strikes ($2) minus the debit amount ($0.60), which equals $1.40 or $140 per spread (minus transaction costs).

Credit spread

To determine the risk amount of a credit spread, take the width of the spread and subtract the credit amount. The potential reward on a credit spread is the amount of credit received minus transaction costs. To illustrate, let's say you sold the XYZ 36-strike put and bought the XYZ 34-strike put (the "XYZ 36-34 put vertical") for a $0.52 credit. To calculate the risk per spread, you'd subtract the credit received ($0.52) from the width of the vertical ($2), which equals $1.48 or $148 per spread (plus transaction costs). Your potential reward would be your credit of $0.52 or $52 per spread (minus transaction costs).

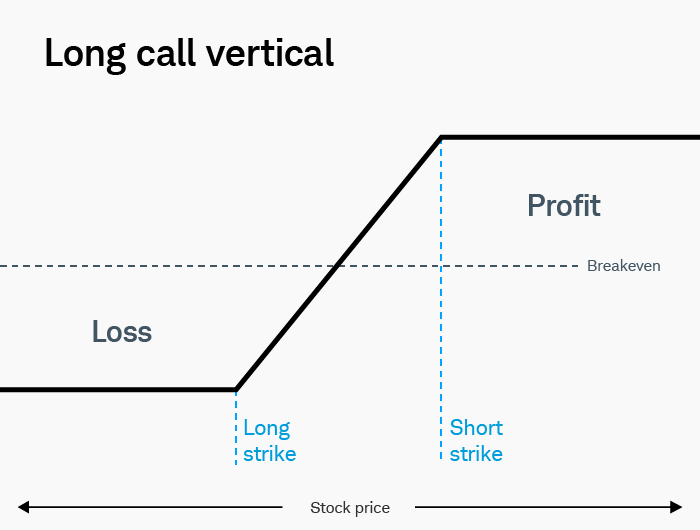

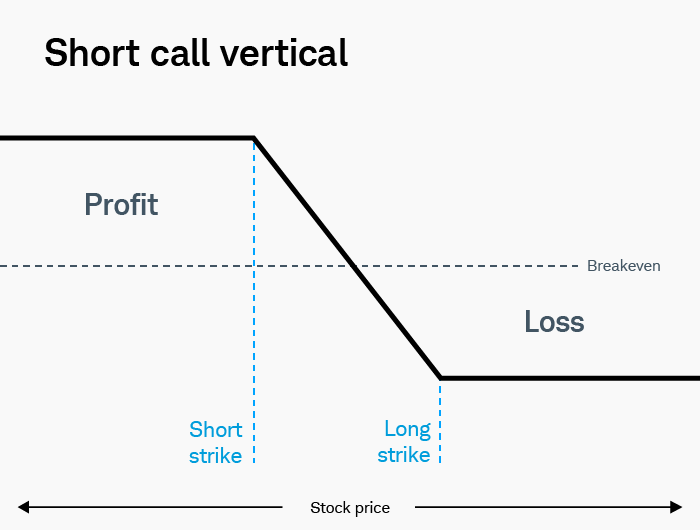

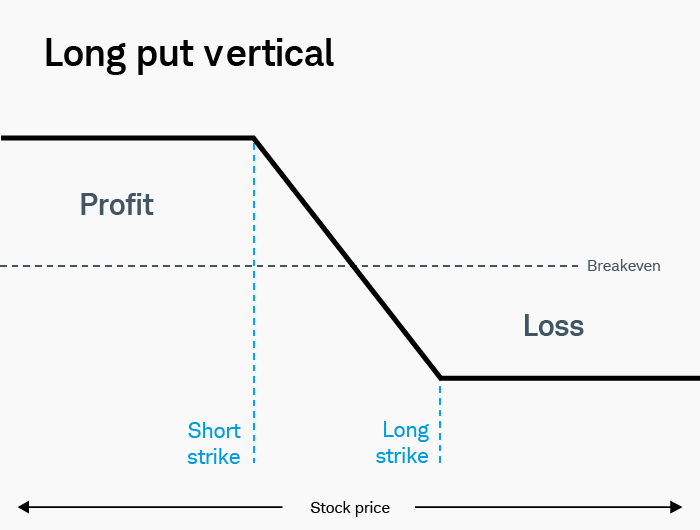

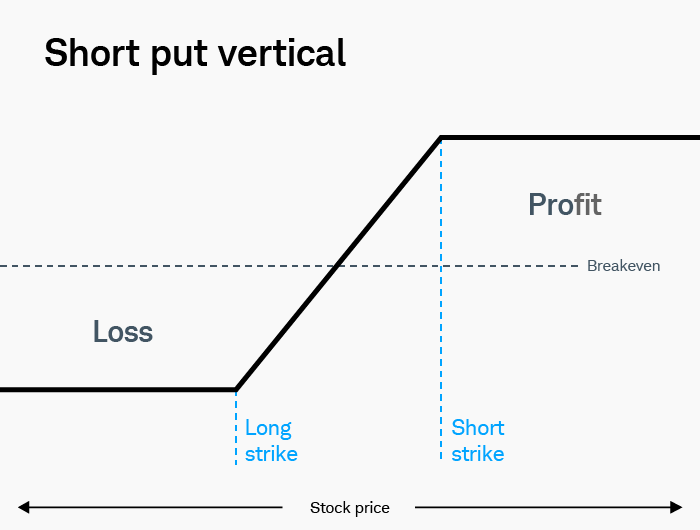

Need a visual description of vertical spread risk parameters? Here are illustrations of the four types of vertical spreads: long call, short call, long put, and short put.

Using dollars risked to determine trade size

Now let's take it a step further. Once you know your risk per spread, you need to determine how much you're willing to risk on the trade.

After you've set that dollar amount, you can calculate the maximum number of contracts you're able to trade and still stay within your risk parameters. It's a simple calculation of dividing the number of dollars you're comfortable risking by the total risk of the vertical spread.

Debit spread example

Suppose you've set $1,000 as the maximum amount you're willing to risk on a trade. Let's continue with the debit vertical spread example above—the XYZ 40-42 call spread that was purchased for $0.60 ($60 with the multiplier).

Because $60 represents your maximum risk per spread, you could buy 16.66 spreads ($1,000/$60). And because you can't trade partial contracts, and you don't want to exceed your maximum risk, you can round down to 16 contracts.

If XYZ stock stays below $40 through expiration, the spread would likely expire worthless and would lose $960 ($60 x 16), which is less than your $1,000 risk amount. This debit spread's potential profit would be $2,240 ($140 x 16) if XYZ is above $42 at expiration. And don't forget those transaction costs.

Credit spread example

For the credit spread, determining the number of contracts to sell is calculated by dividing $1,000 by the $148 per spread risk amount, which equals 6.76 contracts, rounded down to six spreads. If the spread went to its full value of $2—if XYZ stock closes below $34 at expiration—the loss would be $888 ($148 x 6 contracts). The potential reward would be $52 x 6 contracts or $312 (minus transaction costs).

Knowing your maximum risk and potential profit is one of the foundations of sound trading. Running through these simple calculations before you initiate a trade can help you keep your strategy in perspective.

The bottom line on vertical risk parameters and trade size

Keep in mind that the risk profiles above depict the profits and losses of vertical spreads at expiration, but the risks and rewards can change if an unexpected event occurs (or an expected event fails to occur) before or at expiration. For example, short options are sometimes assigned before expiration. Other times, an expected assignment or exercise at expiration might not occur. Here's a handy primer on what to expect at expiration of a vertical spread.

As a final note, we assumed a maximum trade risk of $1,000 but this number should be determined by asking yourself how much of your total trading capital you're willing to risk on any one trade. Some veteran option traders would tell you to keep that number relatively low. Some trades will go your way, and some will go against you, but no one trade should take you out of the game entirely.