5 Tips for Weathering a Recession

Recessions are a regular part of the economic cycle, which means planning ahead is essential. You can't control the economy, but you can take steps to help protect your savings, manage debt, and keep your goals on track. Here are some smart ways to prepare when the economy shifts.

1. Build up your cash reserves

The first step in preparing for a recession is to shore up your cash reserves. Otherwise, you may be forced to sell stocks during a market decline, locking in losses and undercutting your portfolio's capacity to recover.

Aim to have three to six months' worth of living expenses in a relatively safe, liquid account—such as a high-yield savings account, interest-bearing checking account, money market savings account, or a short-term investment like a money market fund or short-term CD—plus enough cash to cover any upcoming sizable expenses, like tuition.

For retirees, cash reserves ideally should be larger. Retirees often benefit from holding a portion of their portfolio in relatively stable, liquid investments to help cover near-term spending needs during market downturns. This approach may help reduce the need to sell stocks or other more volatile investments when markets are under pressure.

2. Stay invested

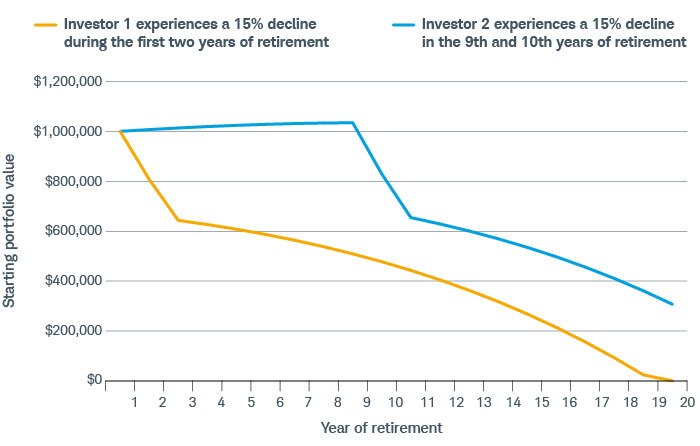

Making a large withdrawal from your savings during a downturn—especially if the decline occurs in the first few years of retirement—can seriously erode your portfolio's longevity.

Source: Schwab Center for Financial Research.

This hypothetical example is only for illustrative purposes. Both hypothetical investors had a starting balance of $1 million, took an initial withdrawal of $50,000, and increased withdrawals 2% annually to account for inflation. Investor 1's portfolio assumes a negative 15% return for the first two years and a 6% return for years three through 19. Investor 2's portfolio assumes a 6% return for the first eight years, a negative 15% return for years nine and 10, and a 6% return for years 11 through 19. These scenarios do not reflect expenses, fees, or taxes.

2. Hold firm

When market volatility increases, it's natural to feel anxious—but selling during an economic downturn can do more harm than good. Investing is a marathon, not a sprint, and staying invested can be one of the most effective ways to keep your long-term financial plan on track.

Trying to time the market usually backfires. That's because not only do you need to time when you sell, you will need to time when you buy back into the market as well, and missing just a few of the top-performing days can dramatically lower your return. For example, the annualized total return1 of the S&P 500 Index from 2006 to 2025 was 11.0%, but if you moved your portfolio into cash after a market drop and missed the top 10 days during that same period, the annualized total return dropped to 6.6%. Keep in mind that past performance is no guarantee of future results.

As long as you have sufficient time and liquidity—whether from wages, retirement income, or cash reserves—it's important to stay the course so you can benefit from any eventual recovery.

Instead of pulling out of the market, focus on maintaining your strategy. That means reviewing your portfolio and adjusting as needed—such as trimming investments that have become overweight and reinvesting in areas that are underweight. These refinements can help you stick to your target allocation and take advantage of the lower prices a down market often provides, without abandoning your long-term plan.

3. Stick with your allocation

When the market is falling, it's natural to want to wait until it recovers to put more money in, but you should really be doing the opposite if you can afford it. As famed investor Warren Buffett once put it: "Bad news is an investor's best friend. It lets you buy a slice of America's future at a marked-down price."

Still, there are a couple of caveats:

- Don't use your emergency savings for new investments. You might be tempted to dip into that pool for especially tempting opportunities, but they're called emergency funds for a reason.

- Don't hoard cash hoping to land a bargain. The sooner your money is in the market, the sooner it can benefit from the effects of compounding, whereas we know that trying to pinpoint the perfect time to get in is notoriously difficult.

- Don't use funds that you need soon. A steep downturn in the market, and potentially your diversified portfolio, can last for several years. Make sure you have the time horizon to weather any losses or hold your cash in an interest-bearing savings or checking account, or stable assets like money market funds or CDs—especially if you're expecting a large expense or purchase in the short term.

4. Find ways to boost cash flow and cut expenses during economic uncertainty

Building additional income streams can help you avoid tapping your investments at the worst possible time and keep your financial plan on track. You might:

- Review your budget. Identify nonessential spending and redirect those funds toward savings or debt repayment.

- Start a side hustle. If possible, consider ways to supplement your primary income, such as freelancing, consulting, or monetizing a skill.

- Sell unused items or assets. A quick declutter can bring in cash, and even potentially reduce expenses such as storage fees, insurance, and/or maintenance costs.

Diversifying your income during a recession can make your finances more recession-proof and help you stay invested for long-term growth.

Schwab clients can log into their account to use our research tools:

- For high-quality stocks: Use the Stock Screener and select one or more of the following:

- For low debt: Under Financial Strength, select Debt to Equity (MRQ), then <1.

- For positive earnings: Under Valuation, select Price/Earnings (TTM), then <10 and 10–20.

- For strong cash flow: Under Financial Strength dropdown, select Cash Flow Per Share (TTM), then 10–15, 15–20, and >20.

- For low volatility: Under Analyst Ratings, select SER Volatility Outlook, then Low.

- For lower-volatility sectors: Use the Stock Screener and under Basic, select Sectors and Industries.

- For fundamental index funds:

- Research fundamental exchange-traded funds using the ETF Screener. Under Portfolio, select Weighting Scheme dropdown, then Fundamental.

- Research fundamental mutual funds using the Fund Screener. Under Basic and then Search By, select Fund Name and type "fundamental" in the search field.

- For longer-maturity bonds: Use the Bonds & Fixed Income tool to select a range of maturity dates under Maturity/Yield.

5. Manage debt and protect your credit

Lenders often tighten credit standards during recessions. That means your credit score—and how you manage debt—becomes even more important. Here's what to do:

- Pay down high-interest debt first, especially credit card debt. Credit card balances and personal loans can quickly become a burden if your income drops or rates rise. Reducing these balances lowers your monthly obligations and frees up cash flow.

- Stay current on student loans and other essential expenses. Missing payments can damage your credit score and make future borrowing harder. If you're struggling, explore options like income-driven repayment plans or deferment.

- Avoid taking on new debt unless necessary. Preserving flexibility is key when uncertainty looms. If you must borrow, compare rates and terms carefully.

- Check your credit score and credit report regularly. A strong credit score can help you qualify for credit if you need it later. Review your report for errors and improve your score by paying bills on time and keeping credit utilization low.

- Don't close old accounts unnecessarily. Keeping older accounts open can help maintain your credit history and utilization ratio.

- Create a plan for your financial situation. If you're carrying significant credit card debt or worried about job security, consider building a budget that prioritizes essentials and debt repayment. This can help you stay afloat if income drops.