Bitcoin Mining Economics and the Pivot to AI

- Mining economics anchor bitcoin's valuation. Because bitcoin's supply cannot respond to price, miner cost of production has historically provided a reference point for downside support and near‑term fair‑value ranges. Given this, bitcoin's risk-reward might appear more attractive when prices trade near or below production costs.

- Artificial intelligence (AI) does not replace bitcoin mining—it reframes it as baseload infrastructure that can continuously run at a steady rate. While AI inference offers higher peak returns per megawatt hour (MWh), its intermittent demand and capital intensity make bitcoin mining the most efficient way to monetize power during off‑peak hours, preserving utilization and cash flow.

- Crypto miners pivoting to AI may reduce—not increase—structural risk to bitcoin. Diversified revenue streams improve miner resilience, lower forced selling, and support long‑term Bitcoin network security, suggesting that hybrid mining/high-performance computing (HPC) models strengthen rather than undermine bitcoin's fundamentals.

- When comparing bitcoin to bitcoin miners, whether publicly traded or privately owned, at current bitcoin prices, bitcoin may offer greater risk-reward compared to miners. When bitcoin trades near inefficient production costs, miners operate with compressed margins. Miners have historically outperformed late‑cycle, though these windows were typically short‑lived and peaked before bitcoin, which might suggest direct exposure to bitcoin may be more attractive today, but there are risks to investing in bitcoin and miners.

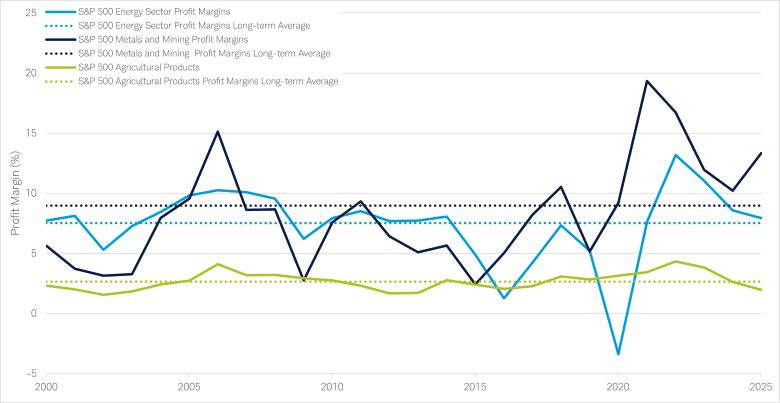

One common feature of commodity producers is slim profit margins. In general, commodity producers are price takers, and their primary competitive advantage is the ability to scale. In times of increased demand for a commodity (or when there is a shortage of supply), producers' margins can temporarily expand. Sometimes, other factors can influence producer margins, resulting in more sustainable competitive advantages. As an example, proven reserves in metals mining (which has a higher concentration of reserves), typically results in higher revenue per ton of metal processed and lower operating costs. Government support can also support margins, whether providing tax breaks or guaranteed purchases (which create price floors). The average U.S. large cap, publicly traded commodity producer has achieved single-digit profit margins over the long term, according to Bloomberg.

Commodity producers typically have single-digit profit margins

Source: Bloomberg, Schwab Center for Financial Research, as of 4/23/2026.

For illustrative purposes only and are not intended to be, nor should they be construed as, a recommendation to buy, sell, or continue to hold any investment.

According to S&P Global, the S&P 500 Energy comprises those companies included in the S&P 500 that are classified as members of the GICS® energy sector. The S&P 500 Metals and Mining Index comprises stocks in the S&P Total Market Index that are classified in the GICS Aluminum, Coal & Consumable Fuels, Copper, Diversified Metals & Mining, Gold, Precious Metals & Mining, Silver and Steel sub-industries. And the S&P 500 Agricultural Index is a sub-index of the S&P GSCI that provides available benchmarks for investment performance in the agricultural commodity markets. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly.

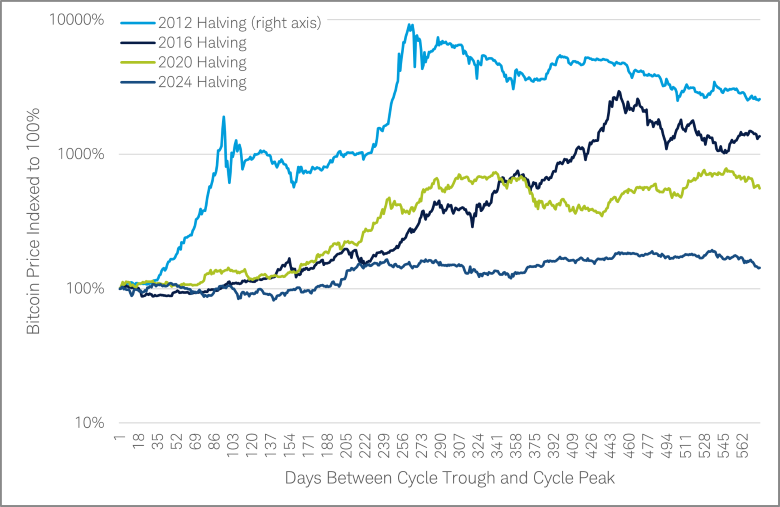

Historically bitcoin has been a cyclical asset. This cyclicality stems from its pre-programmed supply shortage every 210,000 blocks (about four years), when the creation of new bitcoins is again slowed. Three things generally happen when there is a supply shortage of other commodities: 1) new supply comes online; 2) substitute products capture share; or 3) there's demand destruction, which happens when consumers stop buying a product due to high prices or short supply. Bitcoin cannot have new supply come online. Few cryptocurrencies are widely perceived as direct substitutes for bitcoin. It is the original cryptocurrency, has the leading market share, and owners of bitcoin have actually historically benefitted from this disinflationary supply growth, facilitated by the progressive reduction of new coins. The supply shock was purposely designed as a feature of the bitcoin blockchain that could potentially benefit investors in the long run.

As a result, prices have historically overshot to the upside as the market has tried to find a new equilibrium price post bitcoin halving. Eventually there is demand destruction and prices fall, which has typically resulted in crypto winters or deep bear markets that last for several months at a time and are accompanied by negative investor sentiment.

Bitcoin's halving has historically kicked off a bull market, followed by deep bear markets due to demand destruction and negative investor sentiment

Source: Bloomberg, Schwab Center for Financial Research, as of 4/30/2026.

Past performance is no guarantee of future results. For illustrative purposes only and are not intended to be, nor should they be construed as, a recommendation to buy, sell, or continue to hold any investment.

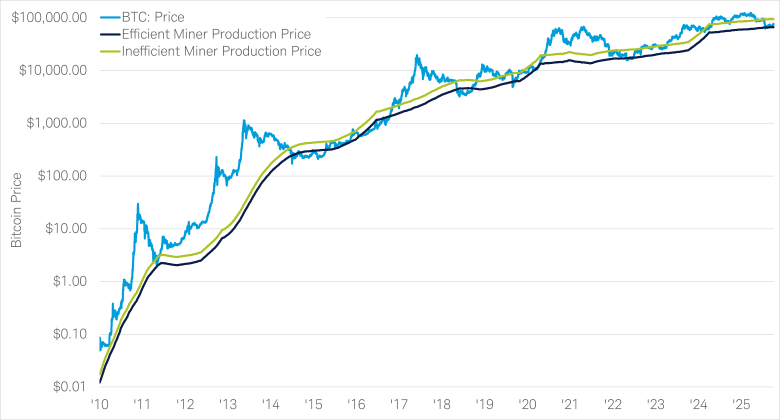

Following bitcoin's peak of $126,000 reached in October, it fell to $60,000, appearing to have found its bear market bottom. Historically, bear market bottoms have been reached near bitcoin's cost of production for efficient miners, and near its 200-week simple moving average. Both of these metrics were around $60,000 in February. But keep in mind that past performance is no guarantee of future results. We previously made the case that bitcoin's market cap to inefficient miner production prices is our preferred method of valuing bitcoin. Taking that analysis a step further, it is important to understand what miner production prices can tell us about the fair value of bitcoin.

Efficient bitcoin miners are similar to other commodity producers with higher proven reserves, scaled operations, or government subsidies. It is important to note that within the U.S., the bitcoin mining industry has not been propped up by government subsidies and we are only saying this as an analogy. Bitcoin miners cannot technically have "higher proven reserves of bitcoin," but they can have lower cost of energy and an efficient application-specific integrated circuit (ASIC) which provides a similar scenario. Miners with less efficient equipment and mining hardware should have a cost of production closer to bitcoin spot prices. By incorporating margin profiles for other commodity producers, we could deduce that the fair value of bitcoin should in general be a minor premium to the cost of production of inefficient miners over the long term. Today inefficient miners have a production cost near $95,000, according to data from Glassnode as of May 22, 2026, a figure that remains unchanged as of April 30, 2026.

It is important to note that we are not suggesting this as a price target. As bitcoin's price rises, it historically has enticed more miners onto the network. As more miners enter the network, the bitcoin difficulty adjustment (the self-regulating mechanism that keeps block production steady) increases, resulting in a higher cost of production. Ultimately the price of bitcoin and number of miners on the network have a reflexive relationship, where both can influence one another in either direction. What our analysis does suggest, however, is a near-term, point-in-time fair value. We used a multiple of bitcoin's price relative to the cost of producing it as our core method for valuing bitcoin.

Historical prices for bitcoin, efficient miner production, and inefficient miner production

Source: Glassnode, Schwab Center for Financial Research, from 7/17/2010 to 4/30/2026.

Past performance is no guarantee of future results. For illustrative purposes only and are not intended to be, nor should they be construed as, a recommendation to buy, sell, or continue to hold any investment.

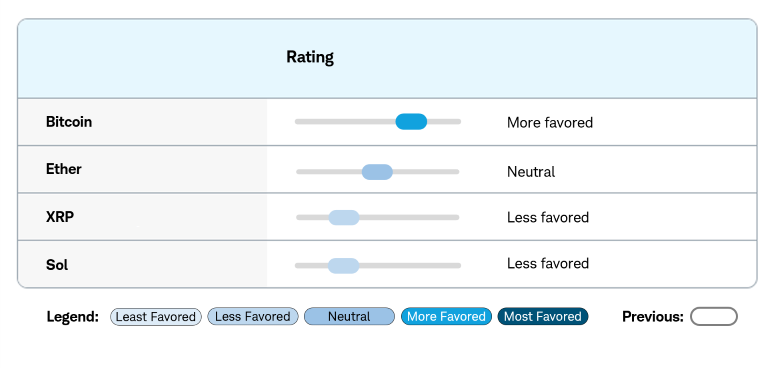

As the cryptocurrency mining industry has matured, participants have begun to hedge production, similar to other commodity producers. This helps navigate the boom/bust nature of the industry. With bitcoin currently below its cost of production for inefficient miners, we feel this reduces the demand for other cryptocurrencies which have historically required sustained momentum in bitcoin to participate in upside. In "A Dream of Spring Amid Crypto Winter," we published our preferred cryptocurrency favorability views.

Summary of Schwab's cryptocurrency views

Source: Schwab Center for Financial Research, as of 4/30/2026.

Note: These favorability views are our preferences for cryptocurrencies relative to their peers. The views reflect a six- to 12-month outlook and may change as markets evolve. Views do not guarantee future returns and are not a forecast that an asset will rise or fall. They are not a recommendation. An unfavorable view does not mean the investment should be avoided, nor does a favorable view mean the asset must be included in a portfolio. An asset can be held for diversification. We suggest using these views as a guide, incorporating the accompanying rationale and other insights.

The views are positioned across a five-point spectrum: Least Favored, Less Favored, Neutral, More Favored and Most Favored. The Schwab Center for Financial Research (SCFR) sets these views. The investment approach incorporates a wide range of quantitative data and qualitative inputs that assess the current market environment relative to historical context. Past performance is no guarantee of future results.

With mining metrics being the primary way we value bitcoin, it's important to understand one of the recent trends in bitcoin mining—pivoting these businesses to high-performance computing (HPC) for AI models. Some market participants wonder what the future holds for bitcoin miners given the more attractive economics that come from AI relative to bitcoin mining. We previously established key debates for four of the largest cryptocurrencies. Now we add another key debate for bitcoin: How will miner pivots toward AI impact bitcoin's network security?

Summary of key debates

- Cryptocurrency

- Sector

- Industry

- Industry Standard Network Effects

- Leading Market Share

- Scalability

- Tokenomics

- Key Debate(s)

- Trading Range

- Current Valuation

-

CryptocurrencyBitcoinSectorFoundational NetworksIndustryStore of ValueIndustry Standard Network Effects✔️Leading Market Share✔️Scalability❌TokenomicsBelow AverageKey Debate(s)

- Quantum Risk

- Miner pivot to AI

- Halving Cycle Persists?

Trading Range0.75x-2x Inefficient Miner ProductionCurrent Valuation0.8 Miner Production-

CryptocurrencyEtherSectorFoundational NetworksIndustrySmart Contract PlatformIndustry Standard Network Effects✔️Leading Market Share✔️Scalability❌TokenomicsAverageKey Debate(s)Ethereum scalabilityTrading Range40x-70x Market Cap/ "GDP"Current Valuation33x Market Cap/ "GDP"

-

CryptocurrencyXRPSectorFoundational NetworksIndustryStove of ValueIndustry Standard Network Effects❌Leading Market Share❌Scalability✔️TokenomicsBelow AverageKey Debate(s)Store of value or smart contract?Trading Range0.1x-0.4x Market Cap/Transfer VolumeCurrent Valuation0.2x Market Cap/Transfer Volume

-

CryptocurrencySolSectorFoundational NetworksIndustrySmart Contract PlatformIndustry Standard Network Effects❌Leading Market Share❌Scalability✔️TokenomicsAbove AverageKey Debate(s)Expand beyond meme trading?Trading Range20x-100x Market Cap/ "GDP"Current Valuation18x Market Cap/ "GDP"

Bitcoin key debate: How will miner pivots toward AI impact bitcoin's network security?

Over the past few years, every major publicly traded bitcoin miner has announced a pivot toward AI data centers. To fund this transition, many have sold bitcoin, which was historically held on their balance sheets. Previously they would monetize these holdings to upgrade their ASIC fleets due to the bitcoin halving, or to meet debt obligations as they came under pressure in bear markets. These sales are due to a fundamental pivot in business models.

This has resulted in a new fundamental debate for bitcoin—if all the large miners pivot to HPC, does that leave the network vulnerable? Public miners are some of the largest bitcoin miners, and as a result, a shift away from their bitcoin mining operations could potentially leave the network vulnerable to bad actors. The more miners that are active on the bitcoin network, the more computing resources it takes to maintain the network. Bitcoin's proof‑of‑work mechanism is designed so that participants with significant computing resources are economically incentivized to secure the network—earning block rewards—rather than attack it. Adversarial behavior is typically more costly and value destructive.

As bitcoin has grown, its security has been supported by a large and globally distributed crypto mining network, making majority control via a 51% attack economically prohibitive. While a single miner or a group of miners, called a mining pool, is unlikely to gain outright control, increasing concentration or coordinated behavior among miners can elevate the risk of temporary transaction censorship, particularly under economic or regulatory pressures.

As more large miners leave the network, this increases the concentration among the remaining miners, which could theoretically impact the network's security. While many mainstream bitcoin investors may not put much of a premium on the decentralized nature of the protocol, it is in fact a fundamental aspect of the Bitcoin blockchain.

Mining economics vs. high-performance computing (HPC) economics

The fundamental question miners must solve is: What is the best use of their power? To answer this question, they must choose the activity that maximizes their energy utilization between HPC and bitcoin mining. To do this, we analyzed the net revenue per megawatt hour (MWh, the units of energy that measure the amount of energy produced or consumed over time) generated by training, inference, and bitcoin mining. We conducted a one-time simulation of a level playing field where each activity had the same wholesale cost of energy and assumed the data centers were using the most efficient semiconductors for each activity. We used current estimates of wholesale energy prices ($40/MWh according to the U.S. Energy Information Administration), to understand the benefit today of mining versus HPC. We also used current estimated prices of GPU (graphics processing units) and ASICs. The goal was to attempt to create a comparison where data centers have similar cost inputs (energy) and can determine their semiconductor fleet based on current costs of different types of semiconductors. Note that this was not intended to be a historical analysis of cost versus revenue, but to be a point-in-time analysis based on the current cost of mining versus HPC.

Training is primarily done by companies that aim to use the resulting large language models (LLMs) to monetize software and other services down the line. It is highly capital intensive and has a negative return on a net revenue/MWh basis. Inference had the most attractive economics, followed by bitcoin mining. In a simple apples-to-apples comparison of net revenue/MWh, inference was the clear winner and would support the idea that miners should abandon mining completely.

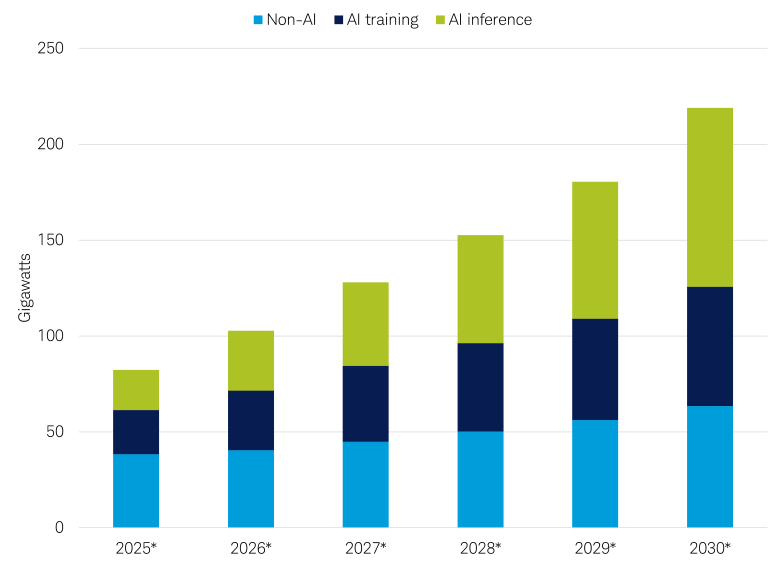

Demand for inference currently occurs primarily during business hours, which would leave the data center underutilized. In a recent report on opportunities in AI infrastructure, we highlighted that inference could reach more than 50% of data center demand by 2030. Training is expected to grow, but at a slower pace than inference. One thing that could impact both training and inference would be capital constraint. To be clear, this is not a "bear case for AI," but it is important to understand how the impacts of capital constraint could shift AI data center economics, and what that might mean for bitcoin miners.

Power demand from AI data has been causing bitcoin miners to pivot to high-performance computing (HPC)

Source: McKinsey Data Center Demand Model published in December 2025.

*All years are estimated. A gigawatt is a power measurement that quantifies large-scale energy capacity for things like data centers and power plants. It is significant to look at the growth in data center demand by workload in the context of gigawatts to illustrate the growth of demand of energy consumption for AI-related activities like AI training and AI inference. For illustrative purposes only and are not intended to be, nor should they be construed as, a recommendation to buy, sell, or continue to hold any investment.

The goal for a data center is to maximize utilization. While inference is forecast to be the fastest-growing segment of global data center workloads, these estimates do not incorporate the potential for capital constraint or how it could impact data center economics.

There are several reasons why data center capital expenditures (capex) could become more constrained. The first is that mega-cap tech companies are now spending so much of their cash flows on AI capex that they have begun issuing debt. Recently, Meta Platforms announced it was laying off 10% of its employees as it continues to spend on AI capex, which was interpreted by the market as a means to repurpose operating capital. As an example, Oracle's five-year credit default swaps (which are financial contracts that insure against the risk of default on a loan over a five-year period) market price have risen from nearly $40 last summer to over $160 as of late April 2026 as they continue to issue debt to fund AI capex. Circular financing (a financial arrangement where funds circulate between companies in a closed loop) concerns in the AI ecosystem might create a self-reinforcing and potentially unstable loop of investment and demand that might cloud genuine market value, which is giving investors caution about future spending.

Large language models (LLMs) are primarily commodity products, much like airlines. For example, there's little difference in experience and price when you're deciding to fly one airline versus another. You will likely pick one that is convenient. It's the same with LLMs—there is little differentiation between the model providers and there are low switching costs so consumers will likely choose what's most convenient. Beyond the models themselves being commodities, the computing resources are also commodities. Right now, the LLM providers are competing against one another to build "smarter" models. The primary input for a smarter model is higher computing power for model training. The issue is it appears scaling laws, which are empirical relationships that illustrate how certain variables affect the performance of a system when they are scaled up or down, may have been reached. Scaling laws indicate that there is little upside gained in terms of model intelligence by new capex spending.

If LLMs are extremely capex intensive commodities, it might suggest that there is not a need for multiple LLMs. Take for example the commercial airline business, which has consolidated to a handful of carriers in the U.S. Each offers an identical service to the other providers, with the differentiation being travel routes. LLMs are distributed and not capacity constrained (whereas seats on an airplane are), so the industry may not need more than one.

On top of all this, technology companies have not shown a return on their capex for LLMs. The general assumption is the models will be monetized down the line by other areas of their business. Historically, investors have not been kind to companies that overspend and underearn. The point of sharing this is not to offer a perspective on equities, it is to reinforce the potential for a more constrained capital spending environment than is currently forecast.

How would capital constraint impact mining and high-performance computing (HPC) economics?

To optimize power usage, data centers must choose a mix of the three activities: training, inference, and mining. Ultimately, if capital becomes more constrained, that results in less training. Training is a lower-utilization activity but it frees up more compute (the ability of a system to perform calculations at scale) for inference. Inference is primarily used during business hours. If there is less demand for training, inference can be spread over more data centers. If the HPC industry is like other industries, producers will likely be competing with one another and offering contracted rates. In price wars, no one wins except the customer. As a result, if capital becomes more constrained, there is less of a shortage of compute to provide inference and potentially more downtime, so bitcoin might become more attractive for maximizing data center utilization during off-peak hours. Below we look at five different scenarios to identify the potential outcomes of where bitcoin miners and data centers optimize their data center utilization.

Data center optimal utilization based on capital availability

- Scenario

- Training Demand

- Inference Demand

- Capital Availability

- Optimal Data Center Utilization

- Potential Impact on Bitcoin's Price

-

ScenarioATraining DemandHighInference DemandModerateCapital AvailabilityAbundantOptimal Data Center UtilizationTraining may occur, but returns are poor; inference + experimentationPotential Impact on Bitcoin's PriceLess constructive, miners are not training LLMs. Inference demand is intermittent during business hours.

-

ScenarioBTraining DemandFlatInference DemandStrongCapital AvailabilityAbundantOptimal Data Center UtilizationInference dominates AI use; training limitedPotential Impact on Bitcoin's PriceLeast constructive, inference has better economics and sustainable demand could pull miners away from the network for non-intermittent time periods. Less volatility revenue streams and steadier operating cash flows reward the shift away from mining.

-

ScenarioCTraining DemandFlatInference DemandStrongCapital AvailabilityConstrainedOptimal Data Center UtilizationBitcoin baseload + inference overlay optimalPotential Impact on Bitcoin's PriceNeutral. Short-term disruption for long-term stability. Stabilizes mining industry long-term to account for volatile crypto revenue.

-

ScenarioDTraining DemandWeakInference DemandModerateCapital AvailabilityConstrainedOptimal Data Center UtilizationMining preferred; limited inferencePotential Impact on Bitcoin's PriceConstructive. Limited demand for training puts pressure on data centers competing for inference. Miners can compete for inference contracts. Helps smooth out revenue volatility but potential to still have pressure on operating cash flows.

-

ScenarioETraining DemandWeakInference DemandStrongCapital AvailabilityVery constrainedOptimal Data Center UtilizationMining dominates; inference only if fully contractedPotential Impact on Bitcoin's PriceMost constructive. Constraints on capital mean limited training and data centers need to compete for inference contracts, resulting in more utilization for mining. Miners remain tied to volatile revenue streams which can put pressure on operating cash flows.

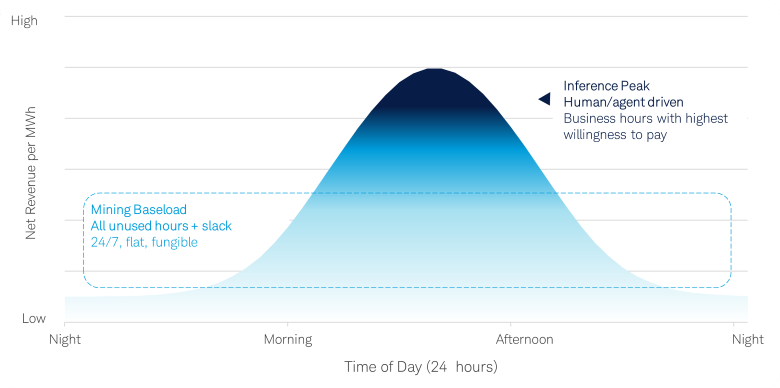

Today's compute shortage reflects simultaneous demand from the three activities. As capital becomes constrained, marginal training capacity is rationed first due to its low capital efficiency. Inference demand persists but is increasingly served by distributing workloads across existing data center infrastructure and concentrating utilization during peak demand windows. As a result, inference increasingly outbids other uses during peak periods, while bitcoin mining remains the rational baseload monetization of power during off peak hours, preserving utilization and cash flow.

Schwab's perspective on this key debate

Many investors closely track hashrate, as it has historically been correlated with bitcoin's price. Hashrate is the measure of computational power per second used when mining bitcoin. As miners have pivoted to AI, price and hashrate have diverged. More miners on the network have historically supported a higher price, because the cost of production for mining bitcoin increased through the network's difficulty adjustment. This historic relationship suggests that as miners pivot toward AI, this could result in near-term pressure on bitcoin's price.

Writer Mark Twain is often (slightly mis-) quoted as saying, "Reports of my death have been greatly exaggerated." For those who fear bitcoin miners' pivots to AI will weaken security of the blockchain network, we feel these fears are also exaggerated. Ultimately, HPC provides an alternate revenue source for miners that could make their businesses more resilient, which could be positive for the bitcoin blockchain in the long run. Over time, we feel a hybrid approach is the most likely outcome (scenario C above), where bitcoin mining is the baseload function and inference is overlayed on that activity during periods of high inference demand. That said, it would not surprise us if Scenarios A and B in the table above capture most of the headlines in the near term.

Bitcoin can be mined 24 hours a day, with data centers shifting their focus to inference during business hours

Source: Schwab Center for Financial Research, as of 4/30/2026.

For illustrative purposes only.

How might Washington have an impact on bitcoin mining?

Other industries receive billions of dollars in government subsidies annually. The agriculture and farming industry is heavily subsidized by the U.S. government through the Farm Bill. Energy producers benefit from tax credits, grants, accelerated depreciation, and loan guarantees. Semiconductors receive grants and tax credits through the CHIPS and Science Act.

Government support could be a powerful ally to the cryptocurrency industry. Even in scenarios A and B in the table above, where capital remains abundant, if larger miners were to completely abandon bitcoin, is it too much of an assumption that the government might support the industry?

One of the most underappreciated aspects of bitcoin mining is the bipartisan support cryptocurrency has across Congress and state governments. Twenty-eight states are exploring establishing strategic bitcoin reserves, with New Hampshire, Arizona, and Texas already passing laws establishing them.

While it is not our base case in the short term, government support for bitcoin mining would not come as a surprise to us.

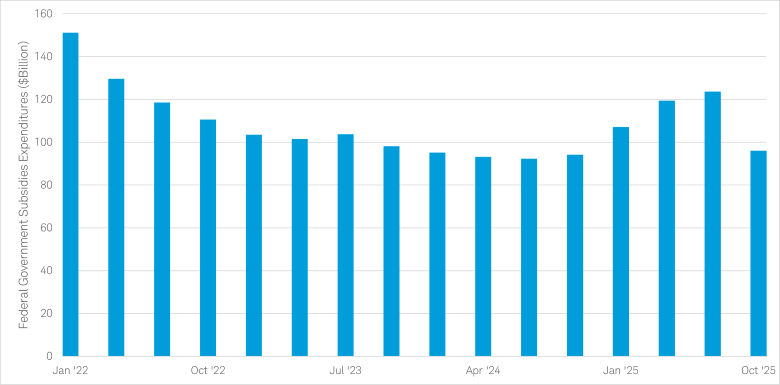

The federal government provided over $100 billion in subsidies from January 2025 to October 2025

Source: Federal Reserve Bank of St. Louis, Schwab Center for Financial Research. As of Oct. 1, 2025.

Considerations when thinking of investing in bitcoin miners or bitcoin

When deciding whether to invest in bitcoin or a publicly traded bitcoin mining stock, we would suggest referring to our cost of production valuation model. With bitcoin trading at a discount to inefficient miner production, that might suggest the average private miner with a less efficient ASIC fleet and higher energy costs is producing at a loss. The publicly traded miners are some of the largest miners on the network and tend to have the best equipment and mining hardware, so they are likely to produce at a discount to that level, which puts an element of conservatism in the framework. Public miners also must disclose their earnings on a quarterly basis, providing investors insight into profitability for these companies.

As bitcoin exceeds the cost of production for inefficient miners, the profit margins on miners expand, which creates a levered effect on the price of the miner relative to the price of bitcoin. That said, these periods tend to be short-lived and bitcoin miners have historically peaked before bitcoin peaks during its four-year halving cycle. That suggests that bitcoin may be relatively more attractive at these production costs compared to bitcoin miners, though past performance is no guarantee of future results.

Keep in mind that all cryptocurrencies are relatively new and due to their novel and unproven nature, reliable methods for estimating performance may not be available. The regulatory landscape for crypto is still evolving. Cryptocurrencies may be subject to potential encryption breaking, illiquidity and increased risk of loss. Theft, scams and fraud have been a factor to deal with, and if you decide to invest in crypto directly remember that there may not be an effective way to recover assets if they're stolen or lost. Investing in cryptocurrencies involves risk, including the risk of total loss of principal invested. Cryptocurrencies such as bitcoin are highly volatile, are not backed or guaranteed by any central bank or government; are not deposits; are not FDIC insured; are not SIPC protected; and lack many of the regulations and consumer protections that legal-tender currencies and regulated securities have. Spot markets on which cryptocurrencies trade are relatively new and largely unregulated, and therefore, may be more exposed to fraud and security breaches than established, regulated exchanges for other financial assets or instruments. Due to the high level of risk, investors should view digital currencies as a purely speculative instrument. Additional risks apply.