The Case for Income Annuities When Rates Are Up

Bonds and cash investments aren't the only assets offering potentially higher income these days. Income annuities—insurance products offering a guaranteed lifelong retirement "paycheck"—are also offering higher payouts than they have in years (though, the returns are different than those offered by bonds, as we'll see below).

This could be good news for two kinds of people:

- Anyone interested in using a chunk of their savings to buy a single premium immediate annuity (SPIA)—that is, an annuity that starts making payments within the coming 12 months or even right away. These contracts can offer payouts for life, covering the purchaser (annuitant) and, for an additional cost, a spouse. They could make sense for people who are in good health, concerned about outliving their savings, or value having a predictable income stream (in combination with Social Security payments and their investments). Of course, as we'll see below, there may be limits to how much of your savings you should consider committing to an annuity, as you'll want to retain the flexibility and liquidity that your regular investment portfolio provides.

- Certain investors who previously bought a deferred annuity—that is, an annuity promising to make payments at a future date, with the potential for tax-deferred growth along the way—which they haven't "annuitized" yet by converting it to income payments. These investors could consider annuitizing their existing contract now or potentially even exchanging their contract for a new SPIA, assuming they prefer the features and meet certain criteria, which we'll cover below. After all, it's generally preferable to annuitize when payouts in the market are higher, as that locks in future payouts.

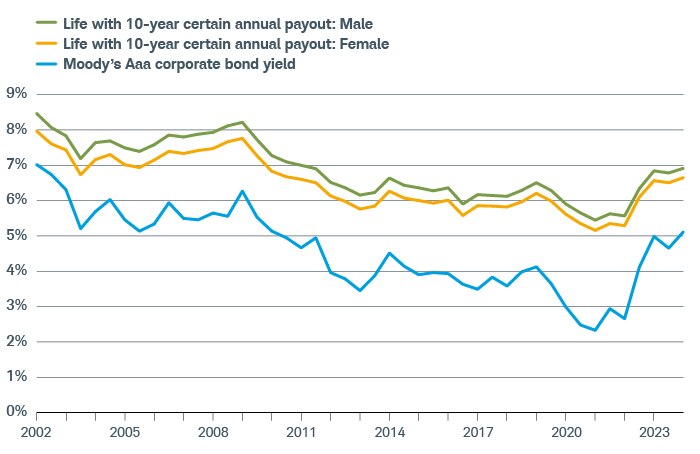

Before we get into the details, it's worth asking up front: How much better are payouts today? We looked at 21 years of data and found SPIA payout rates, like the average Moody's Aaa corporate bond yield, are now at their highest levels in over a decade.

Moving up

Source: Schwab Center for Financial Research. For illustrative purposes only. Past performance is no guarantee of future results. Payout rates are life payments for single male and female annuitants, with a guaranteed 10 years of payouts whether the annuitant lives or dies during that period. (As of September 2023). The payout rates shown represent average payout rates from a representative selection of income annuities today. Historical annuity annual payout rates are from immediateannuities.com's Comparative Annuity Reports and Annuity Shopper Buyer’s Guide.

The Moody's Aaa Corp. Bond Yield was taken from the St. Louis Federal Reserve.

So, here are some things to consider.

For the annuities newbie

Annuities are contracts between you and an insurance company. Depending on what type you select, an annuity can provide fixed or variable returns, opportunities for tax-deferred growth, flexible withdrawals, and other features, including leaving a legacy to an heir. Fees and charges—including sales commissions—will vary by the annuity and distributing firm.

With a single premium immediate annuity, you hand a portion of your savings (the premium) over to an insurance company, which in turn provides you with monthly payments that, depending on the option selected, can continue for the rest of your life (assuming the insurer remains solvent).

For example, if you were a single woman turning 65 on November 6 and living in California, you could potentially pay an insurer $200,000 and receive an immediate monthly income of $1,274, or $15,288 a year, for life. For an additional cost, you could add optional features, such as coverage for your spouse or payments that automatically increase in value to help combat inflation.

For a sense of what's available at Schwab, you can use our Income Annuity Estimator.

An income annuity isn't a savings account that you draw down month by month until you hit zero. If it were, the $200,000 in the example above would be gone in about 19 years, assuming you withdrew $1,160 a month and earned 3% interest on the remainder. Nor are the payments like interest from bonds or dividends from stocks. Annuity payout rates will almost always be higher. Why? Unlike those other sources of income, which don't include your principal, an annuity payout includes a combination of principal plus an additional return that comes from investments made by the annuity company.

But that's not all. What makes annuities unique is that the insurer generally guarantees that it will make these payments for a defined period—say, 20 years—or for the rest of your life and, potentially, the life of a spouse if you choose that option. Like with other insurance products, insurers gather their annuitants in "pools," under the assumption that some of them will live longer-than-average lives, while others will pass sooner. That allows the insurer to use any leftover balances from those who pass earlier to help pay income to those who live longer.

In theory, this means that if our 65-year-old from above lived to be 95, she'd collect over $417,600 from her $200,000 annuity contract.

Keep in mind, though, that these contracts are irrevocable. Once you pay the premium, you get a brief "free look period" ranging from 10 days to a month during which you can change your mind and ask for your cash back. After that, you're locked into the contract. That said, some contracts do offer an option—called a cash refund option—to pay out any leftover premium to a beneficiary if you were to die before receiving payments equal to at least the original premium.

So, whether this is a good investment depends not only on how long you live but also what you value. One investor might prefer the certainty that comes from a guaranteed income they can't outlive, even if it means giving up control of a chunk of their savings. Another might think it better to keep ahold of their savings and leave them invested in the market, potentially for bigger returns or a bigger legacy for their family. Both approaches can work and, for some investors, combining both approaches may work even better.

If you are nearing or in retirement, consider categorizing your expenses as either essential or discretionary. In our view, it makes sense to think about covering some, if not all, of your essential expenses with predictable or guaranteed income sources like Social Security, pensions, and possibly annuities.

So, how much should you commit to an annuity? Based on our research, you could consider starting with between 10% and 25% of your savings for an income annuity, but not more than 50%. Consider keeping the rest invested to suit your spending needs and offer growth potential.

It may be best to work with a financial professional to help think through the pros and cons, the costs, and the different benefit options available.

For those who already have a deferred annuity

If you purchased a deferred annuity sometime in the past but haven't annuitized that contract yet, consider working with a qualified financial planner or directly with an annuity specialist to decide what to do next. You could certainly consider annuitizing your existing contract. In some cases, though, it's possible you could receive higher payouts or secure additional benefits by exchanging the deferred contract for a single premium immediate annuity from another insurer.

This isn't a given, so here are important questions and considerations you'll want to weigh:

- Are you out of your surrender period? An insurer may penalize you if you withdraw from your contract before the end of your surrender period—a period typically lasting between three and eight years. Other factors to compare are guaranteed benefits, differences in features, costs, services, and the financial health of the insurer.

- What is the annuitization rate the insurance company is offering? Investors can, and should, shop around, based on age, terms, and other factors.

- How much do you want to annuitize? You don't need to annuitize the entire annuity. You can annuitize just part of it. Are you paying for an optional withdrawal benefit rider? These riders, offered on some deferred annuities, can allow you to take systematic withdrawals from your annuity without having to annuitize.

Here's an example of how this might work. A single 65-year-old man paid $100,000 for a deferred annuity when he was 40. After 25 years, that annuity has grown to $350,000. He checks his contract and finds that if he annuitizes now, his insurer will pay $1,750 a month, or $21,000 a year, for the rest of his life. If he finds that amount attractive, he could choose to annuitize now.

If not, he could also check with a qualified income annuity specialist to see if he might find a more appealing contract offering a higher payout or other options that aren't covered by his existing contract. For example, he might find that a different insurer is offering a single premium immediate annuity paying $1,947 a month, totaling $23,364 a year, for the rest of his life, plus a guarantee to continue payments for 20 years whether the man lives that long or not. With that option, he could arrange to name his nephew as a beneficiary, who would receive payments for the remainder of the 20-year period if the man died prematurely.

If he preferred the second option—assuming he'd passed his surrender period, wouldn't be surrendering other valuable features from his existing contract, and had fully considered any additional costs or commissions—he could exchange his deferred annuity for the new single premium immediate annuity.

Remember, deferred annuities can also be used for other purposes, including leaving a legacy. But the details matter, including when you may be required by the insurer to start annuity payments, and other factors. Read the contract closely and work with a qualified planner or specialist before making any decisions.

The bottom line

Annuities can be complex, but their income guarantees can potentially complement many different retirement income strategies. And even though payout rates are generally higher today, shopping around could be worth it.

The annuities market is vast, with many different guarantees and options available, so be sure to work with a financial planning professional or experts who can look out for your best interest before making any irrevocable decisions.