Conflict in the Middle East

While the human toll is unimaginable, the market's assessment is that the latest outbreak of war in the Middle East is unlikely to be a material risk to long-term investors

Early assessment

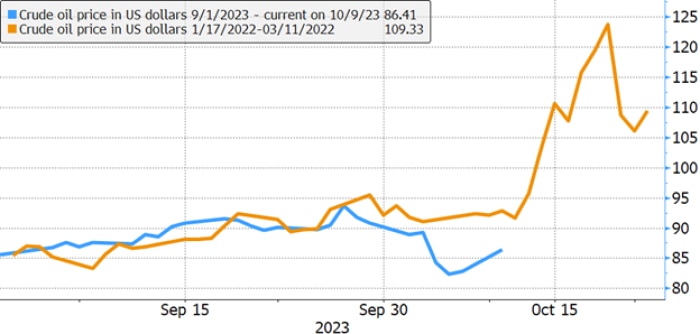

The primary spillover from conflicts in the Middle East has typically been felt in oil and gas prices. Notably, the rise in oil and gas today isn't nearly as significant as that of February 2022's attack on Ukraine by Russia. Oil prices are up 4% this morning, in contrast to the 35% rise over the two weeks starting the day before Russia's invasion on February 24. This larger impact makes sense; Russia supplied over 10% of the global oil and gas market, which were directly threatened. The current conflict seems to put supplies only at risk.

Crude oil prices compared with period around Russia's invasion of Ukraine

Source: Charles Schwab, Bloomberg data as of 10/9/2023.

Past performance is no guarantee of future results.

Although the rebound in oil has the potential to bolster inflation pressures, the price is still below where it was during September's U.S. consumer price index (CPI) reading. Both oil and gas remain small contributors to inflation in most developed countries. For example, in the U.S., energy goods and services account for roughly 7% of the overall CPI and is excluded from the core measures the Fed tends to use as a policy guide.

Market reaction

Recently stocks have been reacting to the big moves in the bond market. In theory, the market could either view the conflict as a risk-off development, pushing bond yields lower or the impact on oil means the conflict is inflationary, driving bond yields higher. Due to the national holiday, U.S. Treasury trading for Monday is confined to futures and they suggest the 10-year yield would be around 10 basis points (bps) lower, near 4.7%. German 10-year yields are down by about 12 bps and the UK 10-year is down by around 10. If the bond market is an indication, the focus seems to be on the risk-off rather than inflationary implications. But these moves are very mild given that Treasury yields have risen 70 bps since the start of September.

The dollar typically sees a rally during flare-ups in geopolitical risk as investors flee riskier assets to buy perceived safe-haven investments denominated in dollars like U.S. Treasuries. But the dollar is barely seeing any lift at all since the start of hostilities. Stocks are seeing only modest moves in early trading and the stock market volatility indexes are far from this year's highs.

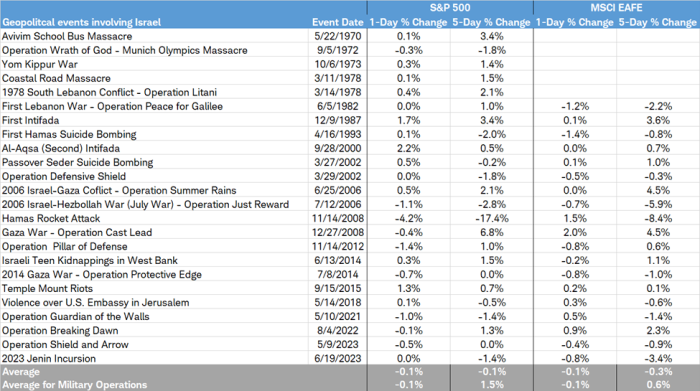

In general, a look back at past geopolitical events involving Israel reveals muted moves in U.S. and international stock markets. Initial reactions are often reversed over the subsequent five days.

Past stock market reactions have been muted

Source: Charles Schwab, FactSet data as of 10/9/2023.

Daily data for the MSCI EAFE Index is not available prior to 1/1/1980. Past performance is no guarantee of future results.

Risks

The relatively calm market reaction doesn't mean there aren't risks of escalation. A strong reaction from Israel could upset Saudi-Israel relations and make any oil supply increase by Saudi Arabia unlikely in the near-term supporting higher prices. The U.S. could potentially bolster sanctions against Iran, after tacitly allowing Iran to ship more oil in violation of sanctions given tight global supplies. If the U.S. cracks down on those shipments, it could further tighten supplies.

Tight supplies combined with low U.S. strategic petroleum reserves and stronger-than-expected job numbers on Friday suggest oil prices may remain firm after today's rebound, which followed a sharp drop in oil prices last week. This indicates continued support for the Energy sector, which had been the best-performing sector during the third quarter.

Oil and conflict

Oil prices have had diminishing reactions to Middle East instability over the years, perhaps because the developments have typically not resulted in sustained disruptions of energy supplies.

- Iranian threats to close the Strait of Hormuz to oil tankers have resulted in harassment, attacks, and/or interference with at least 15 internationally flagged merchant vessels in the narrow passage where one-fifth of the world's crude oil flows, according to U.S. Navy reports. Yet there has been no material disruption.

- Direct attacks on oil infrastructure, like the 2019 strike on Saudi Arabia's Abqaiq plant, have usually seen the facilities quickly fixed and brought back online.

- The redirection of oil flows in response to sanctions on Russia showed how quickly the industry can adapt.

- U.S. shale oil production has shown that it can respond quickly to price increases.

- The spare output capacity of Saudi Arabia has swelled to the highest level in years following this summer's production cutbacks and could be deployed, if needed.

Key takeaway

Geopolitical risk is ever-present, and specific developments may affect the markets from time to time. Although it's a constant undercurrent to investment outlooks, long-term portfolio performance tends to be more dependent on the economic cycle than geopolitical developments. Conflicts may flare up, but tend to not make investors bearish, outside of a recessionary global economy. During periods of even modest economic growth, the global market's response to perceived threats has tended to be short-lived.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.