3 Estate-Planning Fallacies in the Post-OBBBA Era

With apologies to Mother Nature, few sunsets have been more scrutinized than the provision in the Tax Cuts and Jobs Act of 2017 that doubled the federal estate and gift tax exemption—which was due to expire, or sunset, at the end of 2025.

Instead, the One Big Beautiful Bill Act (OBBBA) not only made permanent the historically high exemption but also increased it from $13.99 million per person in 2025 to $15 million per person in 2026, adjusting annually for inflation thereafter.

"In the wake of the OBBBA's passage, many clients canceled estate-planning meetings thinking they'll no longer be subject to estate tax," says Matt McColl, a director of tax, trust, and estate with Schwab's Wealth Strategies Group. "But estate planning is about much more than taxes."

"Regardless of the potential tax burden, you still need to focus on matters like asset protection and how your wealth will be transferred—foundational issues that can be major headaches if not managed correctly," adds Austin Jarvis, director of estate, trust, and high-net-worth tax planning research at the Schwab Center for Financial Research. "The headline is the federal estate and gift tax exemption, but you shouldn't ignore the fine print."

With that in mind, here are three common fallacies of estate planning post-OBBBA, and what you can do to safeguard your estate.

Fallacy No. 1: I don't have estate tax issues anymore

Most estate-planning guidance focuses on federal taxes, but that's not the only possible tax liability:

- State estate and inheritance taxes: Twelve states, along with the District of Columbia, impose their own estate tax—and five states impose inheritance taxes (see "The states' slice"). What's more, while a surviving spouse can inherit any unused portion of a deceased spouse's federal estate and gift tax exemption, only Hawaii and Maryland do the same for the state exemption. "A lot rides on where you reside—and, if you create a trust, in which state your trust resides," Austin says.

Generation-skipping transfer tax (GSTT): If you gift or bequeath assets to beneficiaries two or more generations younger than you, the GSTT could apply.

You can give away up to $15 million to beneficiaries two or more generations removed without triggering the GSTT; however, you must explicitly assign part of your GSTT exemption when giving a skip gift. (Such gifts will also count against your estate tax exemption.)

For example, let's say a woman makes a $100,000 distribution from her estate (or trust) to her granddaughter to help pay for her granddaughter's wedding. The $100,000 would automatically count against the woman's federal estate and gift tax exemption; however, she would also need to explicitly assign $100,000 of her GSTT exemption to the distribution—lest it be subject to a GSTT of 40%. (Distributions in excess of the lifetime GSTT exemption are also taxed at 40%.)

"For high-net-worth families aiming to provide for grandchildren or more distant generations, careful planning can help ensure the transfer of those assets—before and after the estate holder's death—remains shielded from the GSTT," Austin says.

The states' slice

Federal estate taxes may get top billing, but state estate and inheritance taxes can be costly in their own right.

-

State

-

Estate tax exemption

-

Estate tax rates

-

State

Connecticut

Estate tax exemption

Same as federal exemption

Estate tax rates

12%; capped at $15 million

-

State

District of Columbia

Estate tax exemption

$4.99 million

Estate tax rates

11.2%–16%

-

State

Hawaii

Estate tax exemption

$5.49 million

Estate tax rates

10%–20%

-

State

Illinois

Estate tax exemption

$4 million

Estate tax rates

0.8%–16%

-

State

Maine

Estate tax exemption

$7 million

Estate tax rates

8%–12%

-

State

Maryland

Estate tax exemption

$5 million

Estate tax rates

0.8%–16%

-

State

Massachusetts

Estate tax exemption

$2 million

Estate tax rates

0.8%–16%

-

State

Minnesota

Estate tax exemption

$3 million

Estate tax rates

13%–16%

-

State

New York

Estate tax exemption

$7.16 million

Estate tax rates

3.06%–16%

-

State

Oregon

Estate tax exemption

$1 million

Estate tax rates

10%–16%

-

State

Rhode Island

Estate tax exemption

$1.8 million

Estate tax rates

0.8%–16%

-

State

Vermont

Estate tax exemption

$5 million

Estate tax rates

16%

-

State

Washington

Estate tax exemption

$3 million

Estate tax rates

10%–35%

-

State

-

Inheritance tax exemption

-

Inheritance tax rates

-

State

Kentucky

Inheritance tax exemption

$1,000

Inheritance tax rates

0%–16%

-

State

Maryland

Inheritance tax exemption

$1,000

Inheritance tax rates

0%–10%

-

State

Nebraska

Inheritance tax exemption

$100,000

Inheritance tax rates

0%–15%

-

State

New Jersey

Inheritance tax exemption

$25,000

Inheritance tax rates

0%–16%

-

State

Pennsylvania

Inheritance tax exemption

$0

Inheritance tax rates

0%–15%

Fallacy No. 2: I can just unwind my current plan or trust

The once-looming threat of a lower estate tax exemption prompted many wealthy families to employ irrevocable trusts and other estate-planning strategies to help lessen the tax hit. Irrevocable life insurance trusts (ILITs), in particular, were used to keep proceeds from a life insurance policy separate from one's taxable estate in order to help cover taxes and other estate settlement costs, with any remainder passing to beneficiaries.

"In the wake of the OBBBA, some folks may be wondering if there's any way to regain control of those assets," Austin says. Although it may be possible to sell your policy or dissolve your trust, there are several things you should consider first:

- All beneficiaries typically need to agree on selling the policy or dissolving the trust.

- Unwinding irrevocable trusts can be expensive, depending on lawyer fees and the complexity of the assets—and that's in addition to the thousands of dollars already spent establishing the trust.

- You cannot recover whatever portion of your estate tax exemption you've used.

- You may not qualify for a new policy in the future. "Let's say the exemption comes down," Austin says. "There's no guarantee you'll be able to obtain another life insurance policy if you're too old or have had a disqualifying health event."

"Before dissolving your trust, examine your reasons for creating it in the first place," Matt says. "Don't let the tax tail wag the dog."

Fallacy No. 3: I don't really need to worry about the size of my estate

"When it comes to the tax code, permanent just means there's no sunset in place," Austin says. "However, we're rewriting the tax code more frequently than we used to, so just because the estate tax exemption is permanent today doesn't mean it can't change in a matter of years."

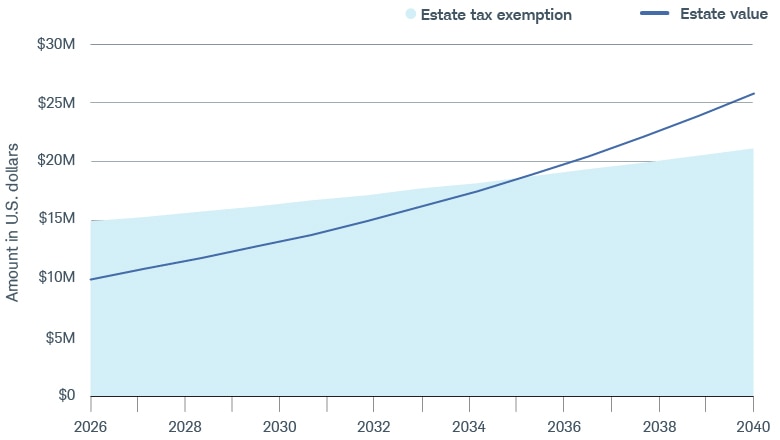

In addition, while the new exemption limit is significant, even the annual inflation adjustment may not keep up with the growth of your portfolio, to say nothing of your other assets.

Exceeding the exemption

Assuming 7% returns and 2.5% inflation, an estate worth $10 million today would surpass the inflation-adjusted exemption in 2035.

Source: Schwab Center for Financial Research.

For illustrative purposes only. Dividends and interest are assumed to have been reinvested, and the example does not reflect the effects of taxes or fees. Assumes an individual estate value of $10 million, 7% estimated annual return, and 2.5% inflation rate. Individual situations will vary. Not intended to be reflective of results you can expect to achieve.

Think bigger picture

The recent changes serve as a reminder that estate planning is about more than minimizing taxes. "Regardless of estate size or tax exposure, it's important to ensure that you've adequately prepared for life's uncertainties, your family is well cared for, and your intentions are clear," Austin says. Key safeguards include:

- Avoiding court: "Have you put in place protections to avoid probate—the often costly and lengthy legal process of adjudicating your will?" Matt asks. "That's a question I'd ask whether you have $20 million or $2 million."

- Designating guardianship for minor children: "Creating such provisions can ensure your children are cared for by those with whom you're most comfortable," Austin says.

- Directing the distribution and management of your estate should you become incapacitated: "Designating powers of attorney, selecting a successor trustee, and putting in place other directives can help safeguard your best-laid plans," Austin says.

- Protecting beneficiaries from creditors: "Do you have heirs in a high-liability profession or with substance-abuse disorders? Any number of vulnerabilities can potentially divert your wealth if you don't plan properly," Matt says.

- Addressing personal wishes: "From your preference for funeral arrangements to who should receive items of sentimental value, declaring your intentions can help avoid confusion and disputes among surviving family members," Austin says.

"When it comes to estate planning, the subject of taxes can sometimes distract from less tangible issues, like what the money's for," Matt says. "Now that there's less of a focus on federal estate taxes, I'm encouraging clients to spend more time thinking about what kind of legacy they'd like to leave."

Discover more from Onward

Keep reading the latest issue online or view the print edition.