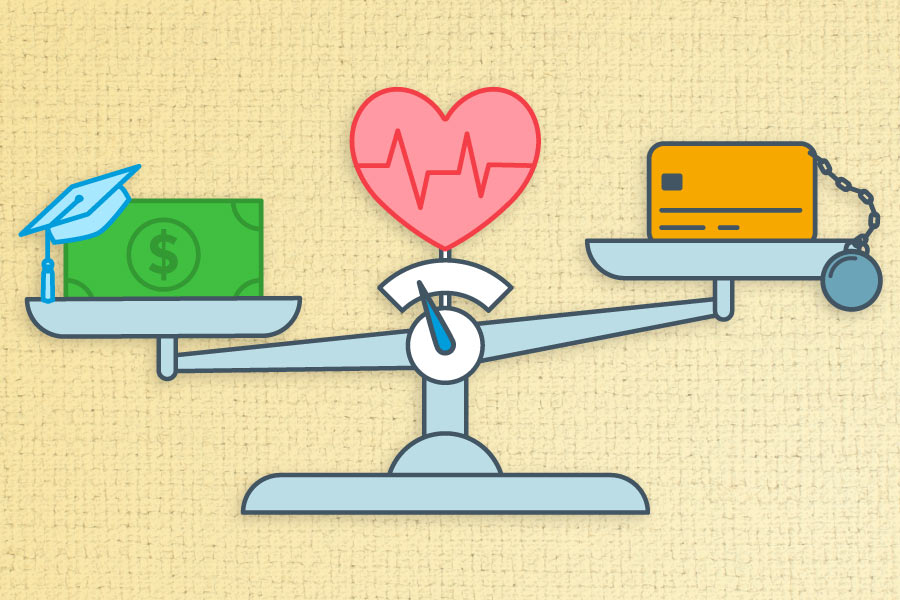

Good Debt vs. Bad Debt: A Wellness Screening

Is all debt bad?

Is all debt bad?

You'll often hear financial pros talk in terms of "good debt versus bad debt," with "good" debt describing things that aim to build your net worth or help you increase your lifetime earnings, such as a home mortgage, business loan, or student loan.

"Bad" debt would be borrowing and paying interest on depreciating assets, like a boat, RV, furniture, laptop, TVs, clothes, etc., or any debt that carries a high interest rate, such as a payday loan or a high-interest credit card.

- Healthy debt: Aims to increase your long-term net worth

- Unhealthy debt: Predatory loans and debt to finance depreciating assets

-

Healthy debt: Aims to increase your long-term net worthMortgageUnhealthy debt: Predatory loans and debt to finance depreciating assetsCredit cards and other revolving debt

-

Healthy debt: Aims to increase your long-term net worthStudent loansUnhealthy debt: Predatory loans and debt to finance depreciating assetsLoans for vehicles or boats

-

Healthy debt: Aims to increase your long-term net worthLoans for technical trading, certifications, job skillsUnhealthy debt: Predatory loans and debt to finance depreciating assetsLuxury goods (hot tubs, designer clothes, jewelry, etc.)

-

Healthy debt: Aims to increase your long-term net worthBusiness loansUnhealthy debt: Predatory loans and debt to finance depreciating assetsPayday loans, title loans, and other high-interest debt

Credit: what comes before debt

Framing debt in terms of good versus bad might not tell the whole story. Before you have debt, you have credit. Credit refers to your borrowing capacity–it's what a lender allows you to borrow based on different factors, such as your credit history, income, assets, other debt, etc. Consequently, to tell the whole story of good or bad debt, you also need to include the decision to use credit.

For example, doctors and nutritionists like to frame food choices in terms of good versus bad for your health. There's good and bad cholesterol, good and bad carbs, and good and bad types of fats. But when consumed in excess, even the good stuff can negatively affect your health.

And yes, there can be too much of a good thing.

In economics, we call it diminishing marginal utility: For each additional unit added, the extra benefit is less and less until you reach the unit that actually does more harm than good.

In economics, we call it diminishing marginal utility: For each additional unit added, the extra benefit is less and less until you reach the unit that actually does more harm than good.

"Good" debt turned bad

Case in point: your mortgage. Borrowing to finance a home can be a good thing because home prices have historically appreciated over time. Sure, you pay interest on a home mortgage, but that interest may be tax deductible, which means you may be able to save on your tax bill.

Plus, assuming it's your primary residence, you may save money that would have otherwise gone to renting a home or apartment. The cost of owning a home can go up, but the cost of a mortgage is generally fixed over its loan term, and that savings can be invested elsewhere like into an emergency fund or your 401(k).

On the other hand, buying more house than you can afford can make you cash-poor and thus vulnerable to a cash squeeze that might force you to max out a credit card or take out a payday loan. This is where a decision to take on a mortgage, which is typically considered a "good" debt, can go bad.

A student loan is another example of what is normally considered "good" debt. Higher education is typically a good investment towards your future earnings potential and can enrich your life in other ways beyond money.

But financing that education through student loans can become bad if the loan repayment becomes overwhelming compared to the income you expect to receive. A number of studies point to student debt as a major reason why millennials may delay buying a home, saving for retirement, or working toward other long-term financial goals. Prior to the COVID-19 pandemic, the average student loan payment was nearly $400 per month, according to Federal Reserve data. That can certainly leave a dent in one's savings plan.

"Bad" debt turned good

Not all "bad" debt is bad. Case in point: credit cards. Not repaying your credit card balance in a timely way can put you quickly in over your head. But, for some individuals who can repay the balance in full, credit cards can be a good way to manage monthly cash flow, improve their credit, and potentially receive perks.

What about car loans? Loans on depreciating assets, such as cars and boats, are usually categorized as "bad" debt, but car loans can be argued either way. While reliable transportation can be important for your job security and advancement, a car also tends to drop in value the minute you drive it off the lot. For any loan, including car loans, it's important to negotiate the lowest interest rate for the shortest borrowing time.

Any time you buy more than what your finances can handle, the debt can shift from good to bad.

Your borrowing decisions matter just as much as the kind of debt you own. In other words, by borrowing smartly to help you achieve your financial goals, you can make more strategic decisions to improve your cash flow and net worth, just as you can by managing assets.

With your money as well as your health, moderation is key.

How to manage your credit

Step one to managing credit is to create a strategy. Financial professionals might suggest organizing your strategy as a set of rules and hierarchies, such as, "do this, not that," and "do this before that."

Here's a way to think about your borrowing decisions:

Know your limits for what you can borrow. Take a realistic inventory of your own capacity to repay loans. Don't take on more obligations than you're comfortable with–this is based on your risk tolerance as well as your financial capacity to take on debt. Think about whether you or your spouse/partner would be able to make the loan payments if either of you were to get sick or injured, lose your job, or pass away. A related concept is just because a lender allows you to borrow a certain amount of money, doesn't mean you have to use all of it. Common financial ratios can help you assess your limits.

- Debt-to-Income (DTI): This ratio measures your total monthly debt obligations divided by your gross monthly income from all sources. You commonly see this ratio with homebuying. Lenders typically like to see a DTI below 40% to 50% (including the mortgage). A lower ratio suggests you can potentially handle a mortgage with other debt obligations and living expenses. If you don't have a mortgage or plan to, you may want to stay below a DTI of 20%.

- Debt-to-Asset (DTA): This ratio measures your total liabilities divided by your total assets. A lower ratio suggests that you have better financial capacity to pay off your debt in case you ever need to use your financial assets. Typically, the older you are, the lower your DTA should be. It's not uncommon to see these ratios below 30% into your 50s and older.

Evaluate whether borrowing can help or hinder your life and financial goals. If you can't say that borrowing money could help you strategically manage your cash flows efficiently, help you further your life and financial goals, or help you grow your assets, then think twice about whether you should borrow money. Consider both sides of the balance sheet to understand how your current and potentially new debt obligations can help or hinder your financial plan. And be sure to plan for the unexpected.

Choose the best credit option to meet your objective. Some lending options may be more obvious than others, such as with a home, car, or college. But it's not always clear (like when you need to borrow money to purchase a home before your old home sells or when you need to tide over two periods of uneven cashflow). A qualified lending specialist or financial advisor may help you think about the different credit options available to you.

Seek to minimize the cost of credit. Choose the best terms and conditions for the loan to minimize the interest cost. Create a payoff plan by prioritizing loans and lines of credit that have the high interest while paying at least the minimum amount to keep all your debt obligations in good standing. Some high-net-worth households are better served by keeping low-interest debt, receiving any potential tax benefits, and investing the excess cash flow to pursue a higher long-term rate of return, within reason. It's like leveraging your wealth to try to build more over time.

Get help. You may choose to seek help from a financial professional who can help you stay on track. Periodic reviews of your financial situation can help identify changes along the way to help you reach your goals. For example, if interest rates drop, you may have a potential opportunity to reduce your monthly debt repayments.

If you're nearing retirement, consider reviewing your credit strategy with a financial advisor and developing a financial plan for paying off major items like new cars or home renovations once you've retired.

Using credit wisely can be a useful strategy, even in retirement. For example, a financial professional might be able to help you decide if you should spread payments out rather than taking a large lump sum out of your investment or retirement accounts to pay off debt.

Bottom line

Debt doesn't have to be bad for your finances if it's used wisely as part of an overall wealth-building plan. It pays to have a plan, make wise decisions that align with your goals, and have a strategy to pay off debt.