Guide on Taking Social Security: 62 vs. 67 vs. 70

Key takeaways

- Claiming Social Security at 62 reduces your monthly benefit—by as much as 30% compared to your full retirement age.

- Your full retirement age is when you're eligible to receive 100% of your benefit amount.

- Waiting beyond full retirement age increases your benefit by about 8% per year until age 70.

- Delaying until age 70 can increase your monthly Social Security payments by up to 24% compared to claiming at full retirement age.

- The best claiming age depends on your specific situation, including your health, income needs, and expected lifespan.

Deciding when to take Social Security depends heavily on your circumstances. You can start collecting Social Security benefits as early as age 62 (or sooner if you're disabled), wait until you reach your full retirement age, or hold off until age 70. (If you're a survivor of another Social Security claimant, you can start receiving benefits—based on their earnings—as early as age 60.)

Taking benefits earlier provides income sooner but also locks in a lower monthly payment. Delaying, however, increases your monthly benefit for the rest of your life. So, if you can afford to wait, holding off on receiving Social Security can increase your monthly income and provide more financial security for retirees over a long retirement. But it's a fraught question for many retirees, filled with tradeoffs and uncertainty.

To understand how these tradeoffs work, it helps to start with your full retirement age.

What's full retirement age?

Your full retirement age (FRA) is the age at which you're eligible to receive your full Social Security benefit. Eligibility is based on your year of birth.1

- If you were born in...

- Your full retirement age is...

-

If you were born in...1958Your full retirement age is...You've already hit full retirement age.

-

If you were born in...1959Your full retirement age is...66 and 10 months

-

If you were born in...1960 or laterYour full retirement age is...67

How much will my Social Security benefits be?

Your annual Social Security statement lists your projected monthly benefits between age 62 to 70, assuming you continue to work and earn about the same amount through those ages. You can request a copy of your annual statement or view it online on the Social Security Administration (SSA) portal.

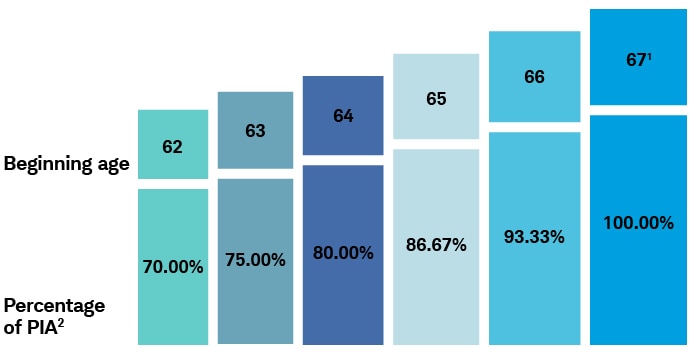

What happens if I take Social Security benefits early? Age 62 through 67

If you choose to take your own Social Security benefit before your full retirement age, your monthly payments will be permanently reduced. The earlier you claim them, the larger the reduction.

In general, claiming at 62 can reduce your benefit by as much as 30% compared to waiting until your full retirement age.

This chart shows how your monthly benefit is reduced based on the age you begin claiming Social Security.

Effect of taking retirement benefits early (DOB: January 2, 1960)

Source: SSA.gov

For illustrative purposes only.

1Represents full retirement age based on DOB January 2, 1960

2PIA = The primary insurance amount is the basis for benefits that are paid to an individual.

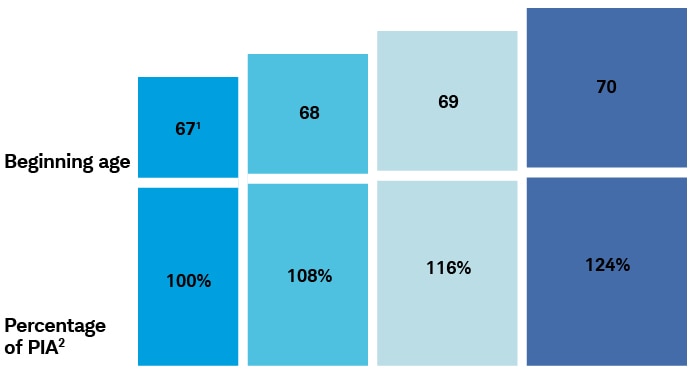

What happens if I delay taking my Social Security benefits until age 70?

If you retire sometime between your full retirement age and age 70, you typically earn a delayed retirement credit (DRC) for your own benefits (but not spousal benefits). The higher baseline would last for the rest of your retirement and serve as the basis for future increases linked to inflation. In no situation should you postpone benefits past age 70.

For example, say you were born in 1960, and your full retirement age is 67. If you start your benefits at age 69, you would receive a credit of 8% per year multiplied by two (the number of years you waited). This means your benefit amount would be 16% higher than the amount you would have received at age 67. (This doesn't include any potential additional cost of living adjustments for inflation from age 67 to 69.)

This chart shows how your monthly benefit increases based on the age you begin claiming Social Security.

Effect of delaying retirement benefits (DOB: January 2, 1960)

Source: SSA.gov

For illustrative purposes only.

1Represents full retirement age based on DOB January 2, 1960

2PIA = The primary insurance amount is the basis for benefits that are paid to an individual.

How should I decide when to take Social Security benefits?

Several factors can help determine the best time to start Social Security payments, including your cash needs, life expectancy, marital status, and employment situation.

Your cash needs

If you're considering early retirement and you have sufficient resources (such as retirement savings, investments, or a pension), you may have more flexibility about when to claim Social Security. If you'll need your Social Security payments to make ends meet, you may have fewer options. You may want to consider postponing retirement or working part-time until you can receive your full benefit.

If you plan to retire before becoming eligible for Medicare, you'll also need to consider how you'll cover health insurance costs and potential long-term care expenses. Both of those can be major expenses in retirement and should be factored into a decision on when to begin claiming Social Security.

Your life expectancy

Claiming Social Security earlier results in smaller monthly payments paid over a longer period, while delaying benefits means fewer checks but a higher monthly amount. Life expectancy plays a key role in this decision: The longer you live, the more you may benefit from waiting to claim.

According to the Social Security Administration, the average life expectancy for a 65‑year‑old is about 84 for men and 87 for women, and for married couples, there's a strong likelihood that one spouse will live into their 90s.

To estimate your own life expectancy, you can use the SSA's life expectancy calculator.

Your marital status

If you're married, your spouse's age, health, and earnings history may affect when you claim—especially if one spouse is the higher earner. At full retirement age, you can generally receive either your own full retirement benefit or up to 50% of your spouse's benefit, whichever is higher.

If you're divorced and were married for at least 10 years, you may be eligible for benefits based on your ex‑spouse's record without affecting their benefits or those of their current spouse. Coordinating personal, spousal, and survivor benefits can be complex, so working with a financial planner may help.

Your employment status

Earning a wage (or even self-employment income) can reduce your benefit temporarily if you collect Social Security. If you haven't reached your full retirement age, $1 in benefits will be deducted for every $2 you earn above the annual earnings limit ($24,480 in 2026). In the year you reach your full retirement age, the reduction falls to $1 in benefits for every $3 you earn above a higher limit ($65,160 in 2026).

However, the month you hit your full retirement age, your benefits are no longer reduced, no matter how much you earn. In fact, the SSA will recalculate your Social Security payments to include the deducted amounts, resulting in higher benefits.

Don't use the reduction as the sole reason to cut back on working or worry about earning too much. That said, if you're still working, you may want to postpone Social Security either until you reach your full retirement age or until your earned income is less than the annual limit.

When should you claim Social Security benefits?

The best age to claim Social Security depends on your financial situation, health, and how long you expect to live. Claiming early provides income sooner but reduces your monthly benefit, while waiting can increase your retirement income for the rest of your life.

Consider taking Social Security benefits early if...

- You're no longer working and can't make ends meet without your benefits.

- You have health issues and don't expect the surviving member of the household to make it to average life expectancy.

- You're the lower-earning spouse, and your higher-earning spouse can wait to file for a higher benefit.

Consider waiting to take Social Security benefits later if…

- You're still working and make enough to impact the taxability of your benefits. (At least wait until your normal retirement age so benefits aren't further reduced due to earnings.)

- Either you or your spouse are in good health and expect to exceed average life expectancy.

- You're the higher-earning spouse and want to be sure your surviving spouse receives the highest possible benefit.

For many people the break-even point (the point where delaying results in more lifetime income) falls in the late 70s or early 80s. If you expect to live beyond that point, waiting to claim may result in the maximum benefit.

Before deciding when to claim Social Security, it's also important to understand how your timing can affect Medicare enrollment.

Important: Social Security and Medicare timing

If you start Social Security benefits early, you'll automatically be enrolled into Medicare Parts A and B when you turn age 65.

Be aware that if you decide to wait to collect Social Security past age 65, you may still need to sign up for Medicare. Missing your enrollment window can delay coverage and result in higher lifetime premiums.

Before deciding when to claim Social Security, make sure you understand how your timing could affect your Medicare coverage and healthcare costs.

Bottom line: Consider delaying Social Security if you can

If you have a choice and are in good health, consider waiting as long as you can to claim Social Security benefits (but no later than age 70). A long retirement coupled with uncertainty about markets and inflation are the biggest risks. Delaying Social Security, if you can, is effectively an insurance policy against those challenges. But you should also consider getting professional advice: a financial advisor can help you determine the role Social Security will play in your overall retirement planning.

Social Security FAQ

How are Social Security benefits calculated?

Your Social Security benefit is based on your lifetime earnings, specifically your highest 35 years of earnings adjusted for inflation. The SSA averages those earnings and applies a formula to determine your benefit at full retirement age.

If you have fewer than 35 years of earnings, zeros are included, which can reduce your benefit.

Once you begin receiving benefits, your payments are adjusted over time through cost-of-living adjustments (COLA), which are designed to keep pace with inflation.

Can you change your Social Security claiming decision?

You may withdraw your Social Security application within the first 12 months and pay back to the government any benefits you received (including Medicare payments, if applicable, and taxes deducted). You'll have to reapply later when you want to restart your benefits, but be aware that you may cancel your application only once.

For example, let's say you elect to receive early benefits at a reduced rate at age 62, but then after a few months, you decide to go back to work. You could withdraw your Social Security application, return the months' worth of benefits, and then wait until you quit your job or need the income to restart your monthly checks at a higher payout.

Are Social Security benefits taxable?

Social Security benefits may be taxable, depending on your combined income. Withdrawals from traditional IRAs or other retirement accounts, along with other taxable income, can cause a portion of your benefits to be taxed—up to a maximum of 85%. For guidance on how this may affect your overall retirement income strategy, consider talking with a CPA or tax professional.

Can my kids inherit my Social Security benefit?

In addition to your spouse, dependent children and even grandchildren may be eligible to receive benefits when you die, become disabled, or retire. To qualify, your dependent must be unmarried and meet certain age requirements:

- Be under the age 18

- Or under age 19 and attending a primary or secondary school full time

- Or any age if they are disabled before the age of 22

For minors, payments stop when they turn 18. Benefits end for students when they graduate or two months after their 19th birthday, whichever comes first. Disabled family members can continue collecting your Social Security until they marry.

The rules are complex, especially around disability. Make sure to consult the appropriate benefit specialists at the Social Security Administration (SSA).

What is the future of Social Security?

For years, the Social Security Board of Trustees has warned against a projected shortfall that could lead to reduced benefits if Congress fails to act. That, of course, is only if Congress fails to act, which seems unlikely, and it's doubtful that Social Security retirement benefits would go away entirely.

The most obvious solutions include raising the retirement age or increasing the payroll tax rate, both of which Congress has implemented in the past to address similar insolvency concerns. Some solutions, however, are likely to be unpopular with Congress and voters alike, and we may not see any changes from Congress until the eleventh hour.

If concerns about Social Security's future make you consider claiming benefits early, it may be more effective to use that uncertainty as motivation to save more—and start saving earlier—for retirement.

1If your birthday is on the 1st of the month, the SSA determines your full retirement age and benefit as if your birthday were in the previous month (December of the year before if your birthday is on January 1).