Help Your College Grad Become an Investor

Key takeaways

- Helping a new graduate get started in the world of investing can be a great gift that can pay off in the long term.

- Many young adults put off investing because it feels intimidating or they assume they'll do it later, but the potential effect of compounding over decades can be a real asset for a young person.

- Matching a graduate's savings contributions can encourage good habits and help them fund near-term goals.

- Funding an IRA can jumpstart their retirement savings, and a Roth IRA can be a practical option for many young workers, as long as they have earned income. But be mindful of gift taxes.

- Investing in stocks or funds tied to brands or causes they care about can make investing feel more relevant, but it works best alongside a savings account with money set aside for an emergency, so young investors are less tempted to sell investments when they need the cash.

- Automated investing services can simplify the process by building a diversified portfolio based on as little, in some cases, as a short questionnaire. That can appeal to beginners who want an easier path to getting started in a comprehensive way.

Finding the right gift for a college graduate can be tough. It's nearly impossible to pick out the latest gadget—let alone the latest fashions—and giving just cash may strike some as too impersonal. So, what can you give a young person, just starting out, that would be useful and meaningful?

Consider opening up the world of investing.

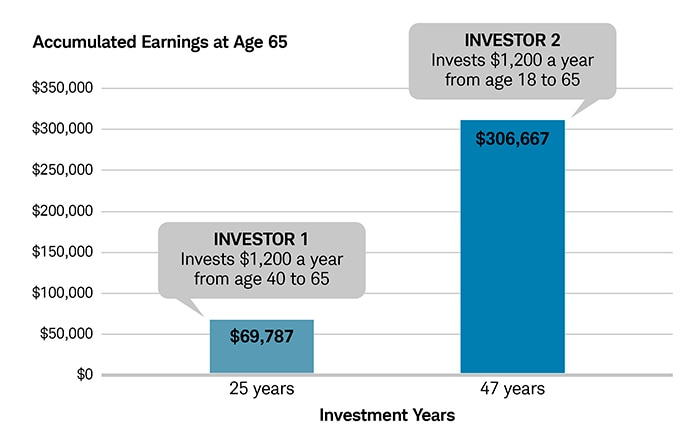

Many young people find the idea of investing intimidating or figure they'll wait until they have more money to work with. That's a shame because if they delay, they might miss out on one of the most powerful drivers of return: time in the market. Time spent in the market and the power of compounding can have a substantial impact on the value of a portfolio. And the earlier your college grad starts investing, the greater the potential benefit.

Time and compounding make a lifelong difference

Source: Schwab Center for Financial Research

Hypothetical examples are for illustrative purposes only and are not intended to represent the past or future performance of any specific investment. Investing involves risk including loss of principal. The balances shown represent the amount contributed and the earnings compounded annually. The examples assume a hypothetical average rate of return of 6%, reinvestment of dividends and capital gains, and no current taxes paid on earnings in a retirement plan account.

But how can you help a young person start down the path to a lifetime of investing and saving? Consider the following gift ideas:

1. Match savings contributions

Saving can be hard to do on a small salary, but it's an important skill to learn. Encourage your new graduate to open a savings account to stash away money for an apartment, a new car, or some other goal—and as an incentive, you can make the initial deposit and offer to match a portion of their contributions.

Keep in mind that taxes may apply on gifts, depending on the amount gifted. In 2026, you can give up to $19,000 per recipient ($38,000 if you're giving as a married couple) without reducing your lifetime gift exemption (currently $15 million if you are a single filer and $30 million for couples). Check with your tax advisor or the IRS website for more information.

2. Fund an IRA

Help your new grad open a tax-advantaged individual retirement account (IRA) to jumpstart their retirement investing. IRAs can be effective savings tools, especially if your grad isn't yet working for a company that offers a workplace retirement plan like a 401(k).

Roth IRAs, which are funded with after-tax dollars and offer tax-deferred growth and earnings, as well as tax- and penalty-free withdrawals in retirement, are particularly practical for younger investors, who are likely to be in a low tax bracket and, as a result, might not get a significant up-front tax deduction from a traditional IRA. (Withdrawal of earnings from a Roth IRA are generally tax- and penalty-free if the account has been open for at least five years since the first contribution and the withdrawals are taken after age 59½.)

Roth IRAs also provide flexibility, since contributions (but not investment returns) can be withdrawn at any time without tax or penalty. (Earnings, however, are subject to taxes and/or penalties depending on the individual's age, how long the account has been open, and the purpose of the withdrawal.) But even though you can withdraw contributions without taxes and penalties from a Roth IRA, grads should be encouraged to keep the funds invested for retirement and to keep the funds potentially growing over the long term.

To fund a Roth IRA, the graduate has to have earned income that's greater than or equal to any contributions made to the account. You'll also want to consider the potential gift tax liability unless funding the IRA is your only gift to them, since the annual gift-tax exclusion is much higher than the maximum allowable IRA contribution, which is $7,500 in 2026 for those under 50.

Also, if you have excess money in a 529 plan, you can potentially rollover up to $35,000 of unused 529 assets into the account beneficiary's Roth IRA. But you should read up on the rules before you make any moves.

3. Give stocks with youth appeal

The stock market can be intimidating to young people, who often don't know where to start. Once again, the great thing is that time is on their side. They should have plenty of time to potentially recover if a high-growth stock runs out of steam or a portfolio begins its life a bit unbalanced.

To pave the way, help the recipient establish a brokerage account if they don't have one already. Once that's out of the way, consider piquing their interest in investing by gifting individual stocks in companies they like or shares in a mutual or exchange-traded fund (ETF) that invests in sectors that interest them, like technology or biotech, perhaps.

If they're socially conscious, consider gifting them shares of an environmental, social, and governance (ESG) fund. There are dozens of such funds in the market that seek to invest in companies engaged in environmental or social justice causes, or companies that are advocating for changes in business practices.

In each case, be sure to communicate the importance of an emergency fund that allows the young investor to leave investments in long-term positions when times get tight. They should understand that their investments aren't a piggy bank, investing is a long-term endeavor, and if they need cash in tough times, they should draw from an emergency fund first.

4. Automated investing

Automated investment advisory services—or robo-advisors—can help build a diversified portfolio that's appropriate for various goals and time horizons.

For young people, robo-advisors might have a lot of appeal, and funding an account could be a great gift for new grads. And it's easy to get started. Typically, most investors only need to answer an online questionnaire to establish their goals, risk profile, and timeline before reviewing a recommended portfolio. There's no need to speak to a human investment professional (unless they want to), and many robo-advisors have additional tools to help track performance and progress toward goals—all easily monitored on a smartphone.

Bottom line

Your young grad might not be starting out with a lot of money, but they have at least one invaluable asset—time. And helping them take their first steps today on a journey of saving and investing might be the greatest gift you ever give them.