How Should Investors Respond to Higher Inflation?

Conventional financial wisdom dictates that, unless you're an active trader, it's best to tune out the noise of daily market news and take the long view with your investments. That's not hard when the market is up. However, the recent surge in inflation and ensuing volatility have turned normal market noise into an earsplitting cacophony.

"Investors are seeing prices spike and their portfolio balances drop simultaneously—a one-two punch if ever there was one—but it's important to remember that inflation isn't going to be this high forever," says Mark Riepe, CPA®, head of the Schwab Center for Financial Research. "Of course, that doesn't mean you can afford to ignore it."

Here's a look at how rising prices are changing the investing landscape and how investors might adjust their financial plans in response.

Red alert

The Consumer Price Index (CPI) has been on a steep and steady ascent since the spring, when a four-decade high of 8.5% in March, only to set a fresh high in June of 9.1%—more than quadruple the Federal Reserve's long-term target of 2%.% The stock market has been struggling as a result, driven by fears that the Fed's interest rate hikes—which totaled a combined 1.5 percentage points between March and June—would drive the economy into a recession.

"The best antidote to high inflation is interest rate hikes, which tamp down spending—and therefore demand—by making borrowing more expensive," Mark says. "But when the Fed is forced to hike rates rapidly, as it's doing now, it can cause a lot of short-term pain in the markets, if not a full-on recession."

A receding threat?

Whether inflation retreats this year or not, it's already having an impact on long-term return expectations.

"This period of high inflation is likely to be transitory in the grand scheme of things, but it’s persisted long enough that it's impacted market expectations," says Veeru Perianan, director of multi-asset research at Charles Schwab Investment Advisory, Inc.

Each year, Veeru and his team update their return forecasts for the next decade for five key asset classes. Their latest adjustments consider the near-term effects of price increases, high stock-market valuations, and interest rate hikes, but also include long-term expectations for inflation, which they believe will be far lower than this year's levels. As a result, the forecasts for some asset classes have actually improved over last year's estimates.

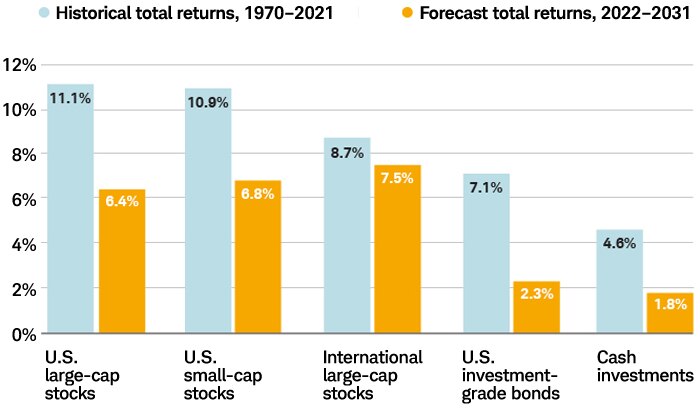

Ray of light

While overall returns are forecast to be lower over the next decade, certain asset classes' prospects have brightened since 2021.

Source: Charles Schwab Investment Advisory, Inc.

Historical data from Morningstar Direct, as of 12/31/2021. U.S. large-cap stocks are represented by the S&P 500® Index, U.S. small-cap stocks are represented by the Russell 2000® Index, international large-cap stocks are represented by the MSCI EAFE Index, U.S. investment-grade bonds are represented by the Bloomberg U.S. Aggregate Index, and cash investments are represented by the Citigroup 3-Month Treasury Bill Index. Total return equals price growth plus dividend and interest income. The example does not reflect the effects of taxes or fees. Numbers rounded to the nearest one-tenth of a percentage point. Past performance is no guarantee of future results.

It may seem counterintuitive for three of five asset classes to potentially benefit from an environment of rising rates, but here's why it makes sense:

- Cash investments (higher): When interest rates rise, savers make more money on their interest-bearing savings accounts, money market accounts, and certificates of deposit.

- U.S. investment-grade bonds (higher): Investors who hold existing bonds to maturity can use their principal repayments to purchase new bonds offering higher coupons.

- International large-cap stocks (higher): The past decade was marked by a period of underperformance for international stocks. As a result, many foreign companies are now undervalued relative to their U.S. peers despite comparable growth prospects, likely positioning them for outperformance in the coming years.

- U.S. large-cap and small-cap stocks (lower): To date, U.S. companies have had little trouble passing on price increases to consumers, allowing earnings expectations to remain strong. Despite the recent market correction, the big gains in 2021 contributed to high valuations, potentially undercutting future returns for large- and small-cap companies alike.

Lackluster prospects

Despite some positive news for three of the five major asset classes, Veeru and his team expect annual returns over the next decade to be significantly lower than their historical averages.

Lower your expectations

Returns for all five key asset classes are forecast to be significantly lower than their historical averages over the next decade.

Source: Charles Schwab Investment Advisory, Inc.

Historical data from Morningstar Direct, as of 12/31/2021. U.S. large-cap stocks are represented by the S&P 500® Index, U.S. small-cap stocks are represented by the Russell 2000® Index, international large-cap stocks are represented by the MSCI EAFE Index, U.S. investment-grade bonds are represented by the Bloomberg U.S. Aggregate Index, and cash investments are represented by the Citigroup 3-Month Treasury Bill Index. Total return equals price growth plus dividend and interest income. The example does not reflect the effects of taxes or fees. Numbers rounded to the nearest one-tenth of a percentage point. Past performance is no guarantee of future results.

"Consensus forecasts, including those from the Fed, anticipate lower-than-average economic growth in the U.S. in the coming decade," Veeru says. In fact, economists expect 2.3% GDP growth per year, on average, over the next 10 years—a meaningful decline from the average annual growth rate of 3.1% since 1948—even after accounting for the possibility of increased economic activity in the near term.

What to do now

How you navigate the next year or two will depend on where you are in life.

For those on the cusp of or in retirement:

- Take heart: As challenging as higher prices can be, Social Security benefits are indexed to inflation, so your annual payments should keep pace with higher prices. In fact, Social Security benefits received a 5.9% increase in 2022—the largest in 40 years—and could see a similar boost next year if inflation persists.

- Temper your near-term spending: Since Social Security likely doesn't cover all your expenses, you may need to make some short-term moves to adjust for higher prices. "If you have some spending flexibility, now's the time to use it," Mark says. "My mom, for example, is going to repair her existing car rather than buy a new one. Those kinds of relatively minor sacrifices can make it much easier to ride out the storm."

- Capture higher rates: Also remember that while higher prices can be painful, the resulting rise in interest rates can help fixed income investors. After inflation cools, rates will level off and may even fall again, so it's important to replace your maturing bonds with higher-yielding options while they last so you can hopefully boost your total income over time.

- Reassess as needed: Finally, don't forget to revisit your retirement plan whenever your needs or the markets demand it. "Most retirees I work with have the same question: 'Am I going to run out of money?'" says Susan Hirshman, director of wealth management at Schwab Wealth Advisory, Inc. "That's a difficult question to answer on your own, but a trusted advisor can help you run the numbers—and think through the potential solutions."

For those not on the cusp of or in retirement:

- Ignore the noise (even when it's deafening): "It's hard to think about the long term when you have short-term bills to pay," Mark says. "But if you're able to absorb the price increases and stick to your plan, this period shouldn't have much of an impact on your future goals."

- Practice good portfolio hygiene: While you shouldn't pay too much attention to daily market gyrations, you should still be checking in on your portfolio from time to time, both to make sure you haven't strayed too far from your target asset allocation—and that your allocation is still appropriate for your circumstances.

"I know we beat this drum a lot, but diversification and rebalancing really can help smooth out your portfolio performance when short-term disruptors like inflation roil the markets," Susan says.

For example, even with this year's volatility, many investors may still be overconcentrated in domestic companies thanks to last year's run-up in U.S. stocks. If that's the case for your portfolio, you might consider shifting some of that money over to international stocks—which are expected to outperform their U.S. counterparts in the coming decade—as part of your rebalancing efforts.

Parting wisdom

"It's always a good idea to revisit the assumptions in your financial plan anytime you're feeling uncertain about the future," Mark says. "Maybe you're less comfortable with risk than you originally thought, or your long-term return expectations are too high. Whatever the reason, reviewing your plan, ideally with the help of an advisor, can help you pinpoint trouble spots and reposition your portfolio for future success."