The Ins and Outs of the New Trump Kids Accounts

As part of the One Big Beautiful Bill Act passed in July 2025, new Trump accounts give eligible American children born between January 1, 2025, and December 31, 2028, a one-time deposit of $1,000 from the U.S. government. They also allow parents and others to contribute a total of up to $5,000 annually in after-tax dollars.

"The government contribution is a great perk, but the absence of an earned-income requirement is even more exciting," says Hayden Adams, CPA, CFP®, director of tax planning and wealth management research at the Schwab Center for Financial Research. "Now, you can help your child start saving for retirement as soon as they're born rather than waiting until they get a job, as is the case with a custodial IRA."

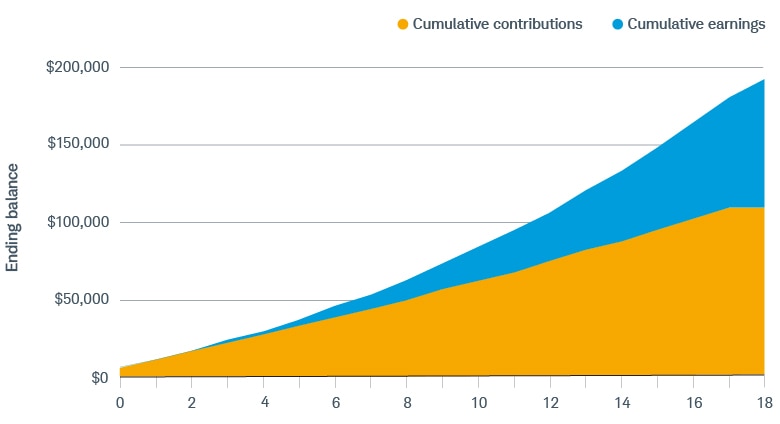

Indeed, a child born today who receives the initial $1,000 deposit plus maximum contributions to their account annually could end up with more than $191,000 by the year they turn 18.

A serious head start

A Trump account opened at a child's birth and funded with the maximum amount each year could grow to more than $191,000 by the time the child is 18.

Source: Schwab Center for Financial Research.

Assumes 2026 government contribution of $1,000 and parental contribution of $5,000 for a child born in 2026, followed by annual parental contributions of $5,000, which are adjusted for inflation at a rate of 2.3% beginning in 2028. Parental contributions continue through the year the child turns 17. Assumes investment growth of 6%. Dividends and interest are assumed to have been reinvested, and the example does not reflect the effects of fees, which would cause performance to be lower. For illustrative purposes only. Individual situations will vary. Not intended to be reflective of results you can expect to achieve.

While the finer points of the accounts are still being hashed out—they're expected to be available after July 4, 2026—here's what we know.

Eligibility

- An account can be established for any child with a Social Security number who is age 17 or younger for the entire calendar year in which the account is opened.

Government contribution

- Only U.S. citizens who have a Social Security number and are born between 2025 and 2028 are eligible for the $1,000 deposit.

- The $1,000 deposit doesn't count toward the $5,000 annual contribution limit.

Contribution limits

- Annual contributions are capped at $5,000 in 2026 and are indexed to inflation beginning in 2028.

- A parent's or child's employer may contribute up to $2,500 in 2026 (indexed to inflation beginning in 2028)—which doesn't count toward the employee's taxable income but does count toward the annual limit.

- Federal, state, and local governments, along with charities, can contribute tax-free to a child's account without impacting the annual limit.

- In the year the child turns 18, the account becomes subject to the same contribution rules governing traditional IRAs.

Investments

- Contributions must be invested in funds that track a qualified U.S. stock index, do not use leverage, and do not have annual fees and expenses of more than 0.1%. (A qualified U.S. stock index is the S&P 500® or any other index that's composed primarily of the stocks of U.S.-based companies and for which regulated futures contracts are traded on a qualified board or exchange. Industry- or sector-specific indexes do not qualify.)

Withdrawals

- The money generally can't be withdrawn before the account owner turns 18.

- When the child turns 18, the account becomes subject to the same withdrawal rules governing traditional IRAs.

Taxes

- While personal contributions aren't tax-deductible, neither are they subject to federal taxes when withdrawn. That said, withdrawals of any earnings or pretax amounts will generally be taxed as ordinary income.

- Early-withdrawal penalties apply for distributions taken before age 59½ unless used for qualified expenses, such as certain higher education costs or the purchase of a first home (up to $10,000).

Sources: One Big Beautiful Bill Act, 2025. | The Council of Economic Advisers, "Trump Accounts Give the Next Generation a Jump Start on Saving," whitehouse.gov, 08/29/2025.

Discover more from Onward

Keep reading the latest issue online or view the print edition.