Options Expiration: Definitions, a Checklist, & More

In an earlier era of options trading—two or three decades ago—attendance one day a month was virtually mandatory for market makers in the options trading pits of Chicago and other financial centers: options expiration day. Volume was usually heavy, and the potential for volatility was ever-present. In short, trading options on expiration day was seen as a time of opportunity and risk.

These days, however, with daily, midweek, and weekly options adding to the standard monthly and quarterly dates, options expiration happens every day of the week.

For traders new to options trading who don't quite understand all the terminology and logistics, expiration can also be a challenging or risky time. Here are a few things all traders should know if they want to avoid potential pitfalls and better understand the ins and outs of expiration day.

Basic options lingo

- Option holder/buyer. The buyer ("owner") of an American-style option has the right, but not the obligation, to exercise the option on or before expiration. A call option gives the owner the right to buy the underlying security at a specified price (the strike price—see below); a put option gives the owner the right to sell the underlying security at a specified price.

- Multiplier. When an option holder buys a put or call, they pay a premium. To arrive at the total cost of an options contract, the premium is typically multiplied by 100 (exceptions may exist with some nonstandard options contracts). This multiplier represents the number of shares in the contract. For example, if an option is trading for $1.40, the price of one contract, excluding fees, is $140, or $1.40 x 100 (multiplier).

- Expiration. Each option has an expiration date, which is when the contract expires and ceases to exist. It marks the final deadline for option holders to exercise their right to buy or sell the underlying security at a specified price. After expiration, the contract can no longer be exercised.

- Strike price. Each option also has a strike price. This is the fixed price at which an option holder can buy or sell an underlying security if the option is exercised before the contract expires.

- Moneyness. Options can either be in the money (ITM), at the money (ATM), or out of the money (OTM). An ATM option has a strike price at or near the price of the underlying security. A call option is ITM if the underlying security's price is above the strike price (opposite for puts) and OTM if the underlying security's price is below the strike price (reverse for puts).

- Option writer/seller. When a trader sells (or "writes") an American-style option (call or put), they may be assigned if the option is ITM on or before expiration day (and, in rare cases, even slightly OTM due to after-hours price movement, as described below). The option seller has no control over assignment and no certainty around timing. Assignment on a short call means the seller must deliver, or sell, the underlying shares at the strike price, while assignment on a short put means the seller must buy the underlying shares at the strike price.

- Options intrinsic value. This is the difference between a strike price and the underlying security's current price. For example, if a stock is trading for $51, a 50-strike call option has $1 of intrinsic value. If that option is trading for $1.40, the remaining $0.40 is known as extrinsic value, or time value. OTM options consist only of extrinsic value.

Options contract specs

American-style options can be exercised any time before the options expiration date, while European-style options can only be exercised at expiration. Standard U.S. equity options (options on single-name stocks) are American-style. Most options on stock indexes, such as the Nasdaq-100® (NDX), S&P 500® Index (SPX), and Russell 2000® Index (RUT), are European style.

Also, standard equity options are not cash-settled—actual shares are transferred during exercise/assignment. Options on broad-based indexes, however, are cash-settled in an amount equal to the difference between the settlement price of the index and the strike price of the option (times the contract multiplier).

Settlement and triple witching

Each quarter, on the third Friday in March, June, September, and December, contracts for stock index futures, stock index options, and stock options all expire on the same day. This so-called "triple witching" period may lead to greater trading activity and increased volatility.

Some index options are AM-settled, meaning they're settled Friday morning but typically stop trading Thursday afternoon. But the settlement price isn't computed until Friday morning. The monthly option AM settlement value isn't based on the opening price of the index, but rather on the price determined by the opening trade price in each stock that comprises the index. This is known as "the print."

What if a market-moving event happens between Thursday night and Friday morning? So-called print risk is the overnight risk of AM-settled options.

Other options are PM-settled, meaning they trade later on expiration day and settle based on the closing value of the underlying security (or the index's closing value). On their final trading day, trading in expiring PM-settled options typically ends at 3 p.m. CT, apart from some broad-based exchange-traded fund (ETF) options, which trade until 3:15 p.m. CT.

On expiration day, options are typically automatically exercised if they're ITM by $0.01 or more as of 3 p.m. CT. In general, the option holder has until 4:30 p.m. CT on expiration day to exercise the contract. These times are set by the Options Clearing Corporation (OCC), the central clearing house for the options market. But some brokerage firms might have an earlier cutoff than this threshold.

If a trader's long option is ITM at expiration but their account doesn't have sufficient funds to support the resulting position, their brokerage may, at its discretion, issue a do-not-exercise (DNE) instruction on their behalf. Any gain the trader may have realized by exercising the option will then be wiped out. DNEs—which can be submitted by any option holder—instruct the broker not to auto-exercise ITM options at expiration. A broker may also, at its discretion, close out (sell) the position without notifying a trader. Meanwhile, all OTM options expire worthless.

Did you know?

On expiration day, options will be automatically exercised if they're ITM by $0.01 or more as of the 3 p.m. CT price. In general, the option holder has until 4:30 p.m. CT on expiration day to exercise the contract. These times are set by the Options Clearing Corporation (OCC), the central clearing house for the options market. But some brokerage firms might have an earlier cutoff than the OCC threshold.

If your long option is ITM at expiration but your account doesn't have enough money to support the resulting long or short stock position, your broker may, at its discretion, issue a do not exercise (DNE) on your behalf, and any gain you may have realized by exercising the option will be wiped out. DNEs can be submitted by any option holder and instruct the broker not to auto-exercise ITM options at expiration. A broker may also, at its discretion, close out (sell) the position without prior notice to you. Meanwhile, OTM options expire worthless.

Expiration checklist: Manage and monitor your expiration risk

Everybody loves a long weekend, but if you've ever taken an unwanted position into the weekend due to an options expiration mishap, that time between Friday expiration and the Monday open can feel like a painful, gut-wrenching eternity.

Now that you've been introduced to the lingo and logistics, here's a list of things to know, check, and perhaps double-check as you go into expiration.

Do your research. Are there news alerts like ex-dividend dates, earnings, or other announcements expected on a company in which you hold expiring options?

Check your specs. Do your options settle American- or European-style? Is settlement in the morning or afternoon? What are the trading hours? Does the underlying trade outside of regular market hours? For example, options that are ITM as of the close are typically automatically exercised, and OTM options aren't. However, if the price of the underlying changes after the close, you might have a short option go from OTM to ITM. The option holder may choose to exercise, leaving you with an unwanted (or at least unexpected) position. However, there is also no guarantee that an ITM short option you hold will be assigned.

Liquidate (or have enough cash on hand). To avoid any margin calls or unwanted overnight or weekend exposure, make sure you plan ahead for any positions you might acquire on expiration. For example, to exercise a long equity call option, you need to have enough cash in your account to pay for the shares. Alternatively, if your account is approved for margin trading, you need to hold cash or securities to satisfy the "Reg T" margin requirement. If you're unsure, or if you don't want the position, liquidate the option before market close. Just remember, there’s no guarantee of a liquid market.

Leave yourself some time. Unlike some video games, in options trading, it's not always a good thing to be the last person standing. As you get closer to 3 p.m. CT on expiration day, liquidity can often dry up and bid/ask spreads may widen. So, if you're considering liquidating, or even rolling to another expiration date, sooner may be better.

Risks and returns

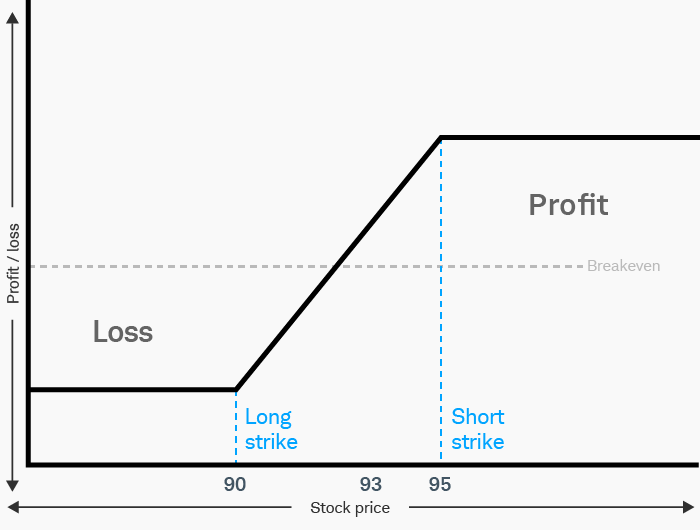

Here's one crucial final item for an options trader's expiration checklist: Know and understand the specific risk profile and potential maximum loss of the strategy. For example, the risk profile below shows a long vertical call spread, which is created by being long the 90-strike call and short the 95-strike call. Note that if, at expiration, the price of the underlying security is below the 90 strike, both options will likely expire worthless.

On the other hand, if the underlying security is above $95 at expiration, then the spread will likely be closed without a resulting position in the underlying security, as the $90-strike call is exercised, and the $95 strike is assigned (the stock would then be called at $90, then immediately sold at $95). However, there is no guarantee that the ITM 95-strike call will be assigned (if the holder submits a DNE request, for example), which could result in an unexpected long stock position at $90 per share.

Vertical call spread risk profile

For illustrative purposes only. Past performance does not guarantee future results.

But what about the area in between the strikes? Or the points of uncertainty right around the 90 and 95 strikes? Will a trader have a position, or won't they?

If the 90-strike call is ITM and the 95-strike call is OTM at expiration, the lower-strike call will be subject to automatic exercise and the 95-strike call will likely expire worthless. Therefore, a trader would buy the shares for $90 unless they close the position by selling the spread prior to expiration (or submit a DNE for the ITM call). If the underlying security is at a point of uncertainty around either strike, and the trader doesn't want to exercise the contract or get assigned, then they'll likely want to try to close the spread before expiration or submit a DNE to their broker.

Now that we've introduced the language and logistics of expiration, option traders may be able to approach it with a greater understanding of the risks and how they might manage them. Keep the checklist in this article in handy—just in case.