Covered Call Strategy Considerations

The covered call is one of the most popular options strategies for investors and traders with a variety of goals. At its core, it is a defined-risk, defined-reward strategy that combines stock ownership with options selling. While some traders may turn to this straightforward strategy as a way to potentially generate income, others may sell covered calls to offset losses from a declining stock position.

Regardless of how a trader chooses to use covered calls, there are important considerations to understand before getting started—especially for those new to options trading.

Mechanics of the covered call strategy

A covered call is typically a neutral-to-bullish options strategy created by selling an out-of-the-money (OTM) or at-the-money (ATM) call option against 100 shares of stock that a trader already owns (hence the "covered" description).

By selling a call, the trader collects premium upfront in exchange for agreeing to sell their shares at the contract's strike price if the call option is assigned.

Depending on how the trade progresses and whether a trader wants to sell or hold the underlying stock, some traders will buy the call back to close their position prior to expiration or roll it to a later expiration date.

If the covered call expires OTM, the trader keeps the 100 shares and the options premium collected. If the stock moves above the call's strike price, the call option is in the money (ITM) and will likely be assigned, though not guaranteed, requiring the covered call holder to deliver the underlying shares at the strike price.

If assignment isn't the desired outcome, a trader has some choices to make before expiration. They can look to maybe roll the call to a later expiration date—sometimes at a higher strike price—or potentially buy the short call back before it expires, possibly taking a loss on the call but continuing to keep the stock.

It's important to note that short options can be assigned at any time before expiration, regardless of the amount by which they're ITM when using American-style options. An ITM option has a higher risk of being assigned early. Once assigned, it's too late to close the call and the stock will be called away, which caps any potential profits above the strike price.

Common goals of covered call traders

Traditionally, the covered call strategy has been used for one of two primary goals:

- Generate income

- Offset a portion of a stock's potential decline

Let's look at two examples and explore how the strategy works in each case.

Example 1: Using covered calls to generate income

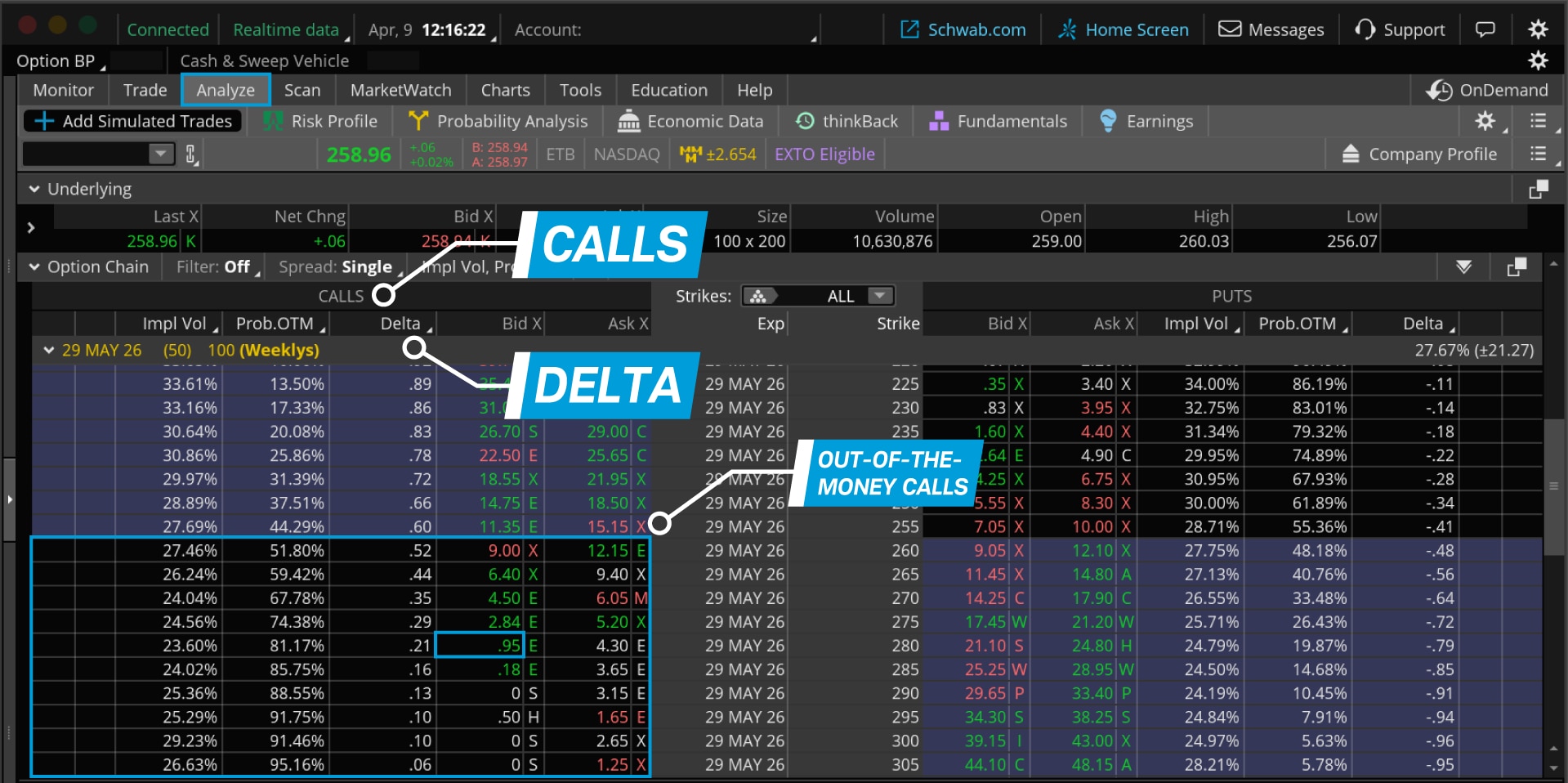

Here's a basic covered call example in which a trader owns 100 shares of ZYX that is trading around $260 per share. As shown in the Option Chain below, there are several strikes in an expiration month. In this example, the trader is focused on OTM calls, or calls with strike prices above the current underlying stock price.

Some traders take the OTM approach in hopes of lowering the odds of seeing the stock get called away or assigned. Others choose strike prices closer to the stock price or even ATM calls to try and collect a larger premium for selling the calls.

In this example, with ZYX at roughly $260 per share, the trader decides to sell a 280-strike call.

Source: thinkorswim® platform

By selling this call, the trader immediately collects $0.95 per contract ($95) minus transaction fees. In return, they accept the obligation to sell the stock at $280 if assigned—roughly $20 more than the current stock price. Before placing the trade, the trader should be comfortable with that potential outcome.

If the stock price remains below the call's strike price through expiration, the option will likely expire worthless, at which point the trader keeps the $95 premium and their ZYX shares.

Options premiums can vary widely from one expiration to the next depending on factors like time value and implied volatility (IV). Options with longer expirations typically have more time value, which can increase premiums. Meanwhile, higher IV generally leads to higher options premiums, while lower IV can reduce the potential premium earned from selling the covered calls.

Example 2: Using covered calls to offset a portion of a stock's decline

Some traders use covered calls to help offset losses on stocks they own when the stock price declines. In this scenario, the covered call seller hopes the short call expires OTM so the premium received offsets, at least partially, the long stock's loss.

However, downside protection is limited. If the stock drops more than the premium received from selling the call, the covered call position begins to lose money. In fact, the maximum possible loss is the stock's original purchase price minus the premium received (excluding transaction fees).

If the stock declines sharply, the short call offers only minimal protection.

Strike selection tactics

The outcome of a covered call often hinges on whether the trader gets assigned, making strike selection a key decision. Timing matters as well. If a trader thinks the stock is ready for a big upside move, a covered call may not be appropriate. Conversely, if a trader thinks a stock's upward momentum is limited, the covered call strategy might be more attractive.

When selecting a strike price, traders should consider the following:

- A strike price at which they'd be comfortable selling the stock.

- A strike price that aligns with an area of potential resistance on the underlying stock's chart.

- The contract's delta, which can provide insight into assignment risk. Delta helps traders determine how much an option may move if the underlying stock moves by a dollar, but it can also be used to gauge the likelihood an option will expire ITM. In the above example, the call had a 0.21 delta, which could be interpreted as having a roughly 21% chance of expiring ITM. While not an exact science—and always changing over time—some traders use delta as a rough guide.

Exploring potential outcomes

Because a covered call foregoes the upside beyond the strike price, it may not be suitable if a trader thinks the stock has potential for significant near-term gains. In more range-bound or slowly rising markets, though, this strategy may be used to potentially generate modest income or offset losses in the underlying stock.

Past price behavior does not guarantee future results, however, so a market moving incrementally in the past won't necessarily continue to do so. If the stock does rise, the call option will typically increase in value as well, and losses on the short call may offset some or all of the gains in the stock price.

If a trader holds an ITM covered call through expiration, the stock will likely be called away. The overall result may still be profitable if the strike price is higher than the break-even point, which (excluding transaction fees) is the stock's purchase price minus the premium collected from selling the call.

If the stock finishes just below the strike price at expiration, the trader typically keeps both the stock shares and the full premium of the now-worthless option.

And if the stock falls, the call will likely expire worthless if it remains OTM. The result might be a gain or loss at expiration, depending on whether the premium received offsets the loss in the stock.

Bottom line: Weighing risk and return

Like all trading strategies, a covered call has trade-offs: Profits are capped at the strike price of the option, and the trader may be required to sell a stock they wanted to keep. Some traders repeatedly sell covered calls to generate ongoing income, while others are cautious about missing out on significant rallies.

Ultimately, covered calls are a study in risk versus return. Understanding how the strategy works—and how different outcomes can affect a position—can help traders decide whether it aligns with their goals and risk appetite.