A Guide to the Covered Strangle Options Strategy

Markets aren't always defined by the dramatic rallies and brutal sell-offs that capture headlines. Sometimes they can slowly grind higher or remain range-bound for extended periods. Seasoned traders often look to more advanced options strategies like covered strangles to manage their positions or potentially generate income during these times.

However, it's important to be aware of the greater risk involved with advanced options strategies. Qualified traders who use covered strangles should understand the profit and loss potential involved before placing an order.

What is a covered strangle?

A covered strangle combines two common options strategies—a covered call and a cash-secured put.

To execute a covered strangle, a trader must either own or acquire at least 100 shares of a security. Then, they sell a call and a put on that underlying security. These contracts should have different out-of-the-money strike prices but the same expiration dates.

Typically, traders employ this strategy while simultaneously holding enough cash to cover the short put if assigned. However, the short put in a covered strangle can also be secured by margin, rather than cash, if the trade is executed in a margin account. In a retirement account like an IRA, the short put must be cash-secured.

A covered strangle is considered a credit trade, because traders receive a net premium (minus any transaction fees) to enter the trade. However, unlike a short strangle, traders should consider that the cost of buying the underlying security will more than offset the options premiums collected.

A covered strangle is also a neutral to moderately bullish strategy because it profits if the underlying remains within a narrow range or moves slightly upward.

Potential results of a covered strangle

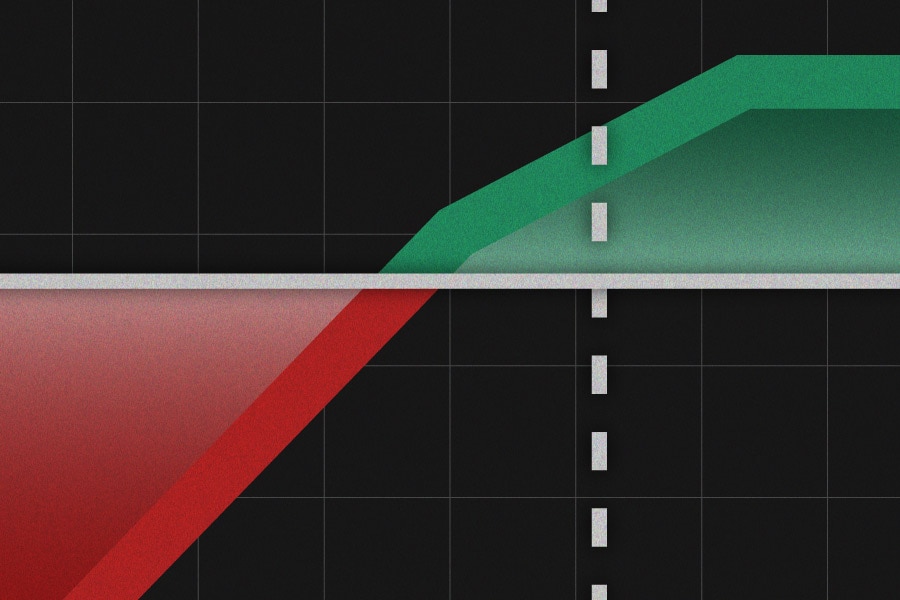

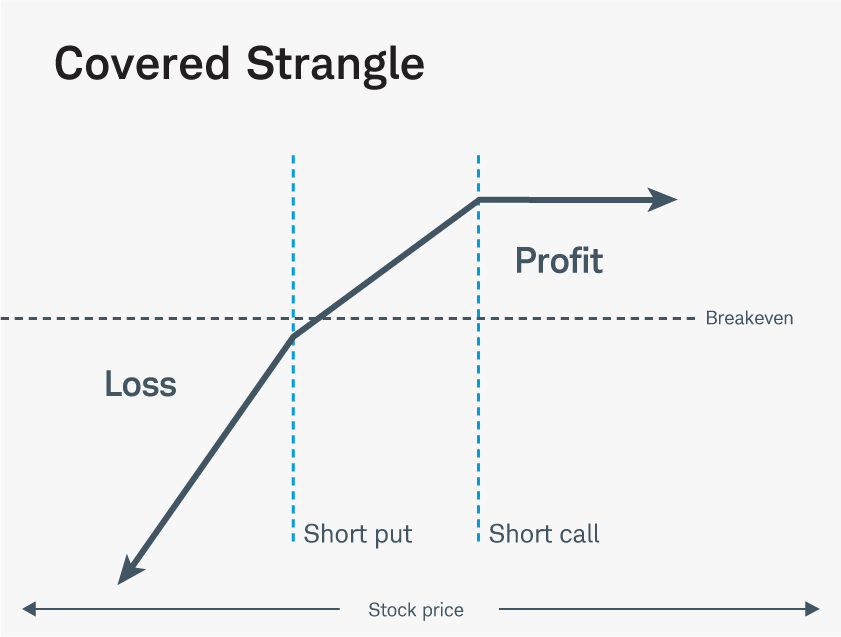

The maximum profit of a covered strangle, excluding transaction fees, is equal to the total premium collected, plus the difference between the call's strike price and the underlying security's purchase price. Maximum gains occur if the underlying's price rises to or above the call's strike at expiration.

The maximum loss of a covered strangle, excluding transaction fees, is equal to the put's strike price plus the underlying security's purchase price, minus the total premium collected from both options. This occurs if the underlying falls as low as $0.

The covered strangle strategy has two break-even points. The upper break-even point is equal to the call strike price plus the total premium collected.

Determining the lower break-even point is more complex because it depends on whether the total premium collected is greater or less than the difference between the underlying security's purchase price and the put's strike price.

If the total premium collected is less than the difference between the underlying security's purchase price and the put's strike price, the lower break-even price is equal to the underlying security's purchase price minus the total premium collected.

However, if the total premium is greater than the difference between the underlying security's purchase price of and the put's strike price, the lower break-even price is calculated by using the following formula: Lower strike price – 1/2 *[Total premium – (initial stock purchase price – put strike price)].

The image below illustrates the risk and reward possibilities of a covered strangle at expiration.

When to use a covered strangle—and other considerations

Traders typically use covered strangles when they have a neutral-to-bullish outlook on the underlying and are looking to potentially generate income in their brokerage or retirement accounts.

The strategy is best suited for periods when traders expect the underlying to remain range-bound, or when they're forecasting a drop in implied volatility (IV)—a measure of the market's expectation of future volatility in the underlying asset.

For example, a trader might expect a stable mega-cap stock to remain within a well-defined range, or rise only slightly, during a period of sideways trading in the broader market. A trader might also expect a significant drop in IV after an earnings report that comes without a substantial move in the underlying.

Because rising IV lifts options premiums, some traders look to initiate covered strangles in a high IV environment. The goal is to sell higher premium, or "rich", options and then profit as volatility falls back to normal levels.

Covered strangles also benefit from theta decay (the decrease in the value of an option over time). As time passes, the options sold in these strategies lose value, making them cheaper to buy back if a trader closes their position prior to expiration.

Covered strangles aren't just about collecting premiums, however; they can also be a systematic way to manage exposure to the underlying. If the underlying falls, assignment on the put can increase long exposure at lower prices; if it rises, assignment on the call can trim exposure and realize gains.

Essentially, traders can earn income while effectively setting predetermined points at which they'd be comfortable selling or buying the shares.

Risks of covered strangles

While covered strangles might help traders generate income and serve as portfolio management tools, they aren't without risk.

The portfolio management feature of covered strangles can be a double-edged sword.

If the underlying falls sharply beyond expectations and the short put is assigned, it can force a trader to buy more shares at the strike price, even though the market price is much lower. Conversely, if the stock rallies more than anticipated and the short call is assigned, a trader may be forced to sell shares at a price that is significantly below market value.

While the additional income of a covered strangle may be appealing, the strategy can expose traders to outsized losses if the underlying makes a volatile move.

Beyond this primary concern, there are several other risks to consider:

- Early assignment risk. When American-style options settlement applies, the options in a covered strangle can be assigned prior to expiration if the underlying moves above the call's strike or below the put's strike. Early assignment can potentially force a trader into or out of a position at a time and price that doesn't align with their plan.

- Illiquidity. A lack of trading volume can increase trading costs, heighten assignment risk, or make it difficult to open or close the positions at fair market prices.

- Margin call risk. If traders use margin instead of cash to implement the put leg of the strategy in a brokerage account and the underlying drops significantly, they might receive a margin call or have to close their trade.

- Tax implications. The premiums collected in a covered strangle will generally be treated as short-term capital gains. And if the short call is assigned, traders may face either long- or short-term capital gains taxes, depending on their initial purchase date. However, the tax treatment of a covered strangle strategy can be complex. Consulting a qualified tax advisor to ensure compliance with IRS regulations is advisable.

- Pin risk. If the underlying trades at or very near the short call's or put's strike price at expiration, there could be uncertainty about whether the options contract will be assigned, potentially leaving a trader with an unintended short or long position in the underlying.

Example of a covered strangle

Given the option chain for ZYX in the table below, a trader who owned 100 shares of ZYX stock and had at least $9,800 cash in their account could establish a covered strangle by selling a 98-strike put for $0.85 and a 102-strike call for $0.85 for a total credit of $1.70 (not including any transaction fees).

If the stock closed at $101 at expiration, the trader would receive $1.70 in premium, and their stock position would appreciate by $1 per share. This could net them a profit of $170 in premiums, not including transaction fees, plus $100 from their long stock position for a total profit of $270—if they sold their shares at a gain.

If the stock closed at $99 at expiration, the trader would still receive the $1.70 premium from both options, but their stock would lose value. This would leave them with $170 in premiums, not including transaction fees, and a $100 loss from their stock holding for a total profit of $70—again, assuming they sold their shares at this time.

Note: This example does not take IV into account, particularly around earnings.

Bottom line

Covered strangles can be a portfolio management tool and potentially generate income, helping traders take advantage of range-bound trading, falling IV, and/or theta decay. But the strategy is more appropriate for experienced traders who understand and are comfortable with the risks involved.

Covered strangles come with real hazards, particularly if the underlying makes an unexpected and sharp move, leading to assignment at inopportune levels. That makes it critical to use the strategy with a clear plan and a disciplined approach.