Oil Edges Up, Stocks Down on Lack of Iran Progress

Published as of: August 10, 2026, 9:17 a.m. ET

Listen to this update

Listen here or subscribe to the Schwab Market Update in your favorite podcast app.

| The markets | Last price | Change | % change |

|---|---|---|---|

| S&P 500® Index | 7,757.64 | +47.68 | +0.62% |

| Dow Jones Industrial Average® | 54,036.93 | +151.83 | +0.28% |

| Nasdaq Composite® | 26,690.61 | +342.26 | +1.30% |

| 10-year Treasury yield | 4.67% | +0.01 | -- |

| U.S. Dollar Index | 99.72 | +0.23 | +0.24% |

| Cboe Volatility Index® | 15.42 | +0.52 | +3.49% |

| WTI Crude Oil | $79.58 | +$1.40 | +1.78% |

| Bitcoin | $65,145 | -$30 | -0.07% |

(Monday market open) After crude oil fell nearly 8% last week and stocks hit record highs, Monday brings new challenges. Lack of weekend Middle East progress lifted oil toward $80 per barrel and investors brace for inflation data and Treasury auctions in coming days with yields still elevated. Wall Street slipped early to kick off a week that also includes earnings from several AI-related firms.

"From a technical perspective, one could say we are overbought on a very-near term basis given the strong week, but the momentum is to the upside," said Nathan Peterson, director of derivatives research and strategy, at the Schwab Center for Financial Research (SCFR), in his Weekly Trader's Outlook. "I believe the outlook favors the bulls due to bullish technical factors and momentum, potential performance chasing, and potential short covering."

The S&P 500 Index posted a record close Friday after the strongest week since April, lifted by strong earnings and falling oil. An unexpected drop of 23,000 jobs in July sent rate hike odds falling, providing another boost for equities, but yields didn't ease much and $125 billion in debt goes on the block this week. Overseas early today, Iran outlined demands in return for reopening the Strait of Hormuz, including the withdrawal of U.S. forces and payment of reparations, The Wall Street Journal reported.

To get the Schwab Market Update in your inbox every morning, subscribe on Schwab.com.

Three things to watch

- More jobs fallout: Several Fed speakers took a hawkish tone last week, some saying it would be better to begin hiking early than to take more dramatic action later. However, those comments came when jobs growth appeared moderately higher. Now it's conceivably a different picture with monthly jobs growth averaging a dismal 34,000 over the last year. Also, July's extremely light wage gain suggests a rate hike might worsen conditions for struggling consumers. It could be worth listening to Fed speakers this week for updated thoughts, with rate hike odds at 46% for September, according to the CME FedWatch Tool, down from 67% a week ago. Looking ahead, the government's sharp downward revisions to May and June jobs growth could mean skepticism if the August jobs report shows a rebound in growth, though with the immigration crackdown fewer new jobs are needed now to keep pace with population growth. The report followed a surge in second quarter productivity, and while correlation isn't causation, this could reflect companies producing more with less labor.

- Earnings strong, but market unforgiving: The second quarter earnings scorecard is still impressive, with broad earnings per share and revenue beats and strong blended growth. At the same time, expectations are extremely high in software, storage, semiconductors, and AI-adjacent winners. Companies are being rewarded only when results, guidance, and commentary signal an all clear. It's a high bar. To date, 88% of S&P 500 companies have reported, with an 85% beat rate and year-over-year earnings growth of 45%, though that includes one-time investment gains reported by several "hyperscaler" firms. Even with those extracted, organic second quarter earnings growth tracks near 30%. Several software companies reported better-than-expected results Friday, providing cheer for that downtrodden sector after investors punished memory chip stocks last week in response to outlooks that didn't appear to impress enough. The key report this week is from Cisco (CSCO) late Wednesday. Cisco has its footprint across so many technology applications around the globe that it's a helpful barometer. On the chip side, Taiwan Semiconductor Manufacturing (TSM) just reported a 45% annual July revenue gain.

- Small caps appear to discount yields: One rule of thumb on Wall Street is that higher Treasury yields hurt small-cap stocks. Smaller companies can depend more on borrowing to finance growth, which means they might face higher costs when yields rise. These firms also typically have a more domestic focus than larger firms, making them vulnerable if U.S. consumers retreat on higher borrowing costs. The 30-year yield remains well above 5% and the 10-year yield is around 4.6%, both near long-term highs posted late last month. Still, the Russell 2000® (RUT) small-cap index holds its own, up 21% year-to-date versus about 13% for the S&P 500 Index and 18% for the Nasdaq-100® (NDX). The resilience could reflect relatively solid economic growth so far this year, though that thesis got challenged by Friday's jobs report. The weak report, however, initially helped lower yields, giving small caps another lift. The Russell 2000 includes many debt-laden companies with negative earnings, meaning the S&P 600 may be a better way to track performance.

On the move

- Berkshire Hathaway (BRK.B) rose after quarterly operating profit jumped 16% to $12.98 billion, a stronger-than expected performance generated mainly by its railroad and service businesses. The conglomerate bought more stock than it sold, including a large purchase of Alphabet (GOOGL) shares. It also repurchased more than $4 billion worth of its own shares.

- Hewlett Packard Enterprise (HPE) popped 5.6% early after Morgan Stanley lifted its rating to overweight from equal weight. The firm cited strong hardware spending.

- Lumentum (LITE) climbed 4% early after a 6% rise Friday, driven by investor optimism about the optics and laser maker's earnings report tomorrow afternoon.

- Varex Imaging (VREX) surged 48% early as Teledyne Technologies (TDY) said it would buy the maker of x-ray imaging components for about $1.1 billion, The Wall Street Journal said.

- SpaceX (SPCX) got a 2.3% early lift amid apparent relief that the end of the share lockup period might ease bearish pressure. Shares rose 16% Friday when heavy selling didn't occur as anticipated after the lockup expiry, Barron's reported. The end of the lockup also allowed large institutional funds to accumulate positions. Competitor Rocket Lab (RKLB) reports after the closing bell.

- Intel (INTC) dropped about 4.6% after the company announced a $15 billion common stock offering, putting more shares on the market. The proceeds are expected to go for capital expenditures and working capital.

- Apple fell 1% early following a downgrade to underperform from hold at Jefferies, which said it doesn't expect Apple to launch an all-glass iPhone, a setback in the firm's efforts to offer higher-priced phones as it wrestles with rising memory costs. Also, Apple is testing Chinese memory chips, The Wall Street Journal reported.

- Semiconductor firm Ceva (CEVA) fell nearly 7% despite slightly better-than-expected earnings per share and revenue. Investors appeared to have hoped for even stronger results.

- The Cboe Volatility Index (VIX) fell below 15 Friday to its lowest level since early this year but ticked higher today on fresh Iran worries. A weak VIX suggests little uncertainty in the market.

- Circle Internet Group (CRCL) rose 5% Friday, lifted by earnings earlier last week that topped Wall Street's expectations.

- Technically, the S&P 500 Index last week broke out of its trading range of between 7,250 and 7,600, which had held for three months. When the SPX hits fresh all-time highs, additional buying pressure can occur due to performance chasing by fund managers and short covering, my colleague Peterson noted.

- Market breadth remains healthy with 72% of S&P 500 stocks above their respective 200-day moving averages, possibly reflecting earnings growth that's looked solid across multiple sectors.

More insights from Schwab

Bitcoin money flows in balance: Investors are putting money into and pulling money out of bitcoin at roughly the same pace as the coin moves sideways and stocks attract more attention and money. Get a full rundown in our fresh cryptocurrency analysis.

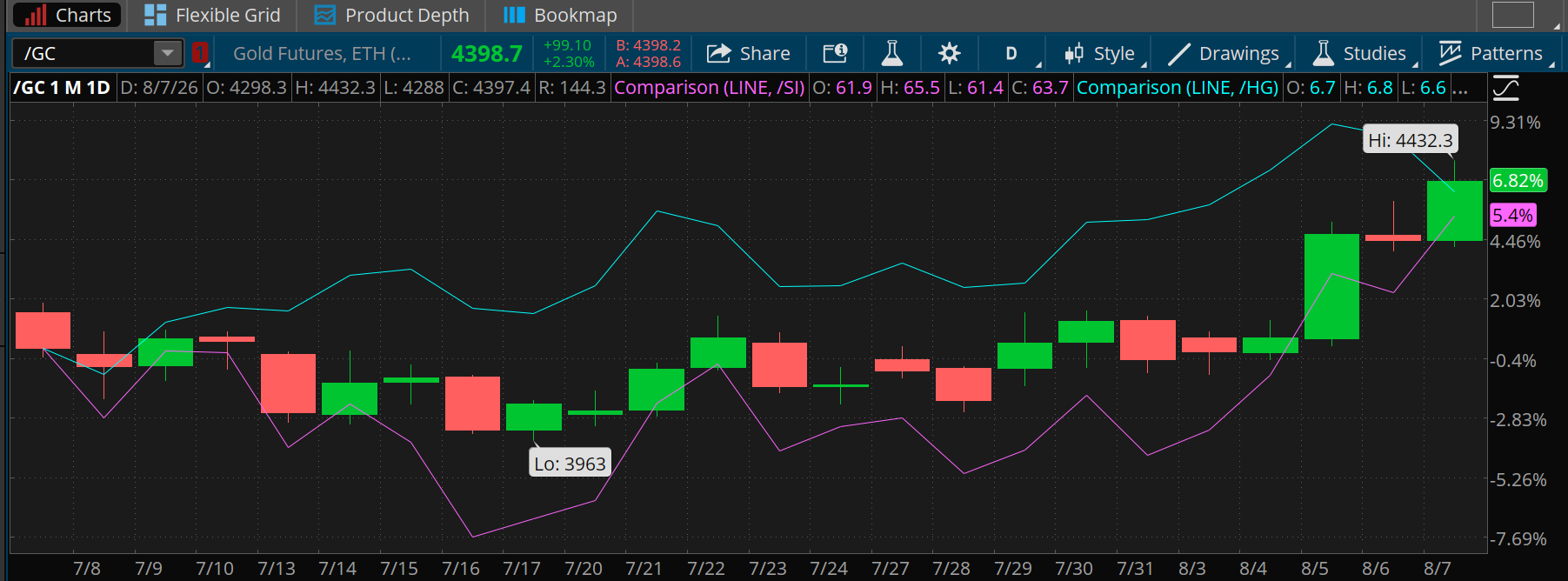

Chart of the day

Data source: CME Group. Chart source: thinkorswim® platform.

Past performance is no guarantee of future results.

For illustrative purposes only.

Metals prices are all up over the last month as the dollar has fallen and rate hike odds have come down. Gold (/GC—candlesticks) is up almost 7% from a month ago. Silver (/SI—purple line) is up 5.4%. Copper (/HG—blue line) has risen 6.53%. Copper also got a boost from reports of supply constraints.

The week ahead