Target Date Funds: Benefits, Risks, and More

Key takeaways

- Target date funds are all‑in‑one mutual funds that automatically adjust asset allocation over time based on a selected target year.

- They are most commonly used for retirement savings but can support other long‑term goals with a defined time horizon, including education.

- A fund’s glide path determines how its mix of stocks, bonds, and cash shifts before and after the target date.

- Target date funds offer diversification, ongoing investment management, and automatic rebalancing in a single investment option.

- They are not risk‑free, and investors should review fees, investment objectives, and glide path differences across providers.

Target date funds are designed to make retirement investing simpler. By choosing a fund tied to the year you expect to retire, the investment mix automatically shifts over time to balance growth and risk. Ahead, we'll explore how target date funds work, their advantages and risks, and how to determine whether one may fit your strategy.

What is a target date fund?

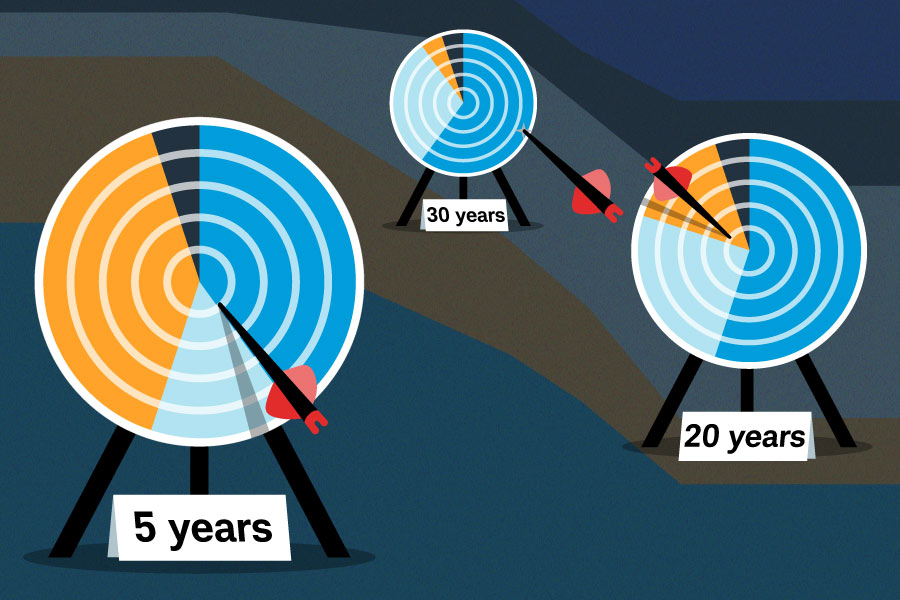

A target date fund (TDF) is an all-in-one mutual fund. It adjusts its mix of stocks, bonds, and cash over time, gradually becoming more conservative as the target date approaches. This planned shift in asset allocation over time is known as the fund's glide path.

Investors typically choose a target date fund based on the year they expect to begin withdrawing money. While they're most often used for retirement savings, target date funds can also support other long‑term goals with a defined time horizon, like saving for education.

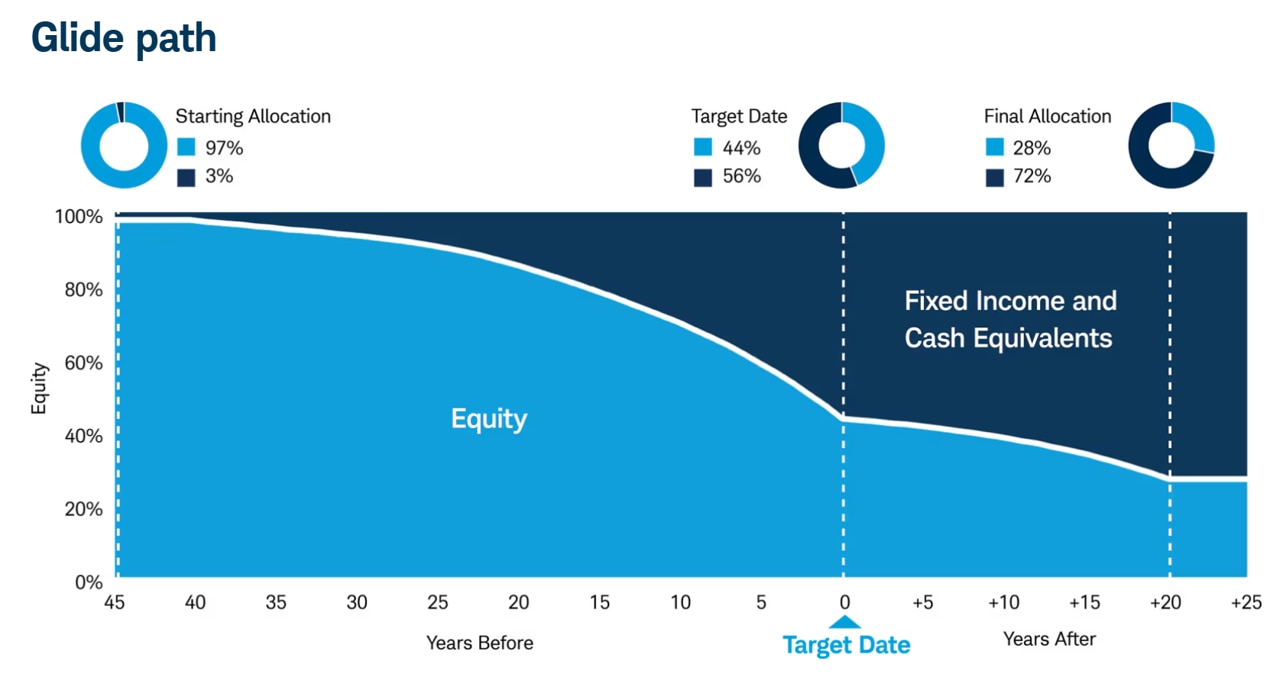

Example of target date fund

Here's an example of the glide path in action, showing how the asset mix slowly becomes more conservative over time.

Source: Schwab Asset Management

This hypothetical example is only for illustrative purposes.

At the beginning of the timeline, the portfolio emphasizes stocks to support long-term growth. As the target date approaches, stock exposure gradually declines while bonds and cash equivalents increase to help reduce volatility.

After the target date, the allocation typically becomes more focused on income and stability. Throughout this process, the fund automatically adjusts and rebalances the portfolio, so investors don't have to manage the shifts themselves.

What happens after the target date?

Reaching the target date does not mean the fund stops investing or shifts entirely to cash. Most target date funds continue investing in a mix of stocks and bonds beyond the target year, with an allocation designed to support income needs while maintaining some growth potential. Because strategies vary by provider, reviewing the fund's glide path can help you understand how risk is managed after the target date.

Ready to take the next step?

Check out these target date fund options.

Advantages of target date funds

Professional management

You don't have to determine the right mix of cash, bonds, and stocks. These funds handle asset allocation and rebalancing while distributing investments across a broad range of asset classes to reduce concentration risk and portfolio volatility.

Automated management reduces emotional investing

By automating investment decisions, target date funds can help you avoid making emotional decisions that can negatively impact their financial goals. Panic-selling when markets are down, or attempting to time market entries and exits, has historically lowered returns.

Built-in diversification

Target date funds typically invest in both U.S. and international stocks and bonds, helping reduce reliance on any single market or sector. This broad diversification can help smooth returns over time and reduce concentration risk.

Age-appropriate allocation

By allocating assets with age in mind, target date funds seek to prevent younger investors from being too conservative and keep older investors from taking too much risk.

Automatic rebalancing

As markets move, portfolios can drift away from their intended asset mix. Target date funds automatically rebalance, helping maintain the fund’s target allocation without requiring action from the investor.

Designed to support long-term discipline

By providing a single, age‑based solution, target date funds can make it easier for investors to stay invested through market cycles. This simplicity may help reduce the temptation to frequently change investments in response to short‑term market movements.

Well-suited for tax-advantaged accounts

Target date funds are commonly used in 401(k) plans and IRAs, where they are often among the core investment options available to participants. In many employer-sponsored retirement plans, target date funds are used as a qualified default investment alternative. This means that if employees are automatically enrolled and do not make an investment selection, their contributions may be directed into a target date fund aligned with their expected retirement year.

Risks of target date funds

As with all investments, you can incur loss

Target date funds are subject to market risk and possible loss, even near or after the target date. Most funds maintain some exposure to stocks throughout retirement, which can result in volatility during market downturns.

Investment strategies vary by provider

Target date funds with the same target year can differ meaningfully in asset allocation, stock exposure near retirement, and post‑retirement strategy. These differences can lead to varying levels of risk and return.

Limited flexibility and customization

Because asset allocation is managed automatically, investors have less control over portfolio decisions. Those who want to actively adjust risk levels or tailor their investments may find target date funds restrictive.

How to select a target date fund

Pick the date

Choose the target date fund with the date that is closest to when you expect to begin withdrawals. For example, if you plan to retire in year 2055, you might consider investing in a target date 2055 fund. Target date funds are generally available in 5-year increments.

Review the fees

Fees vary by provider and underlying investments, and even small differences can compound over time and affect long-term outcomes.

Evaluate the glide path and investment strategy

Glide paths vary by provider. Review how quickly the fund reduces equity exposure as the target date approaches, how much stock exposure remains after retirement, and whether the strategy is actively managed, passively managed, or a blend of both. Make sure the fund's asset allocation and investment objective align with your risk tolerance, time horizon, and broader financial goals.

Are target date funds right for you?

Target date funds may be appropriate for investors who prefer a simplified, professionally managed portfolio aligned to a long-term goal. They can be especially useful for those saving primarily for retirement in a 401(k) or IRA who want automatic asset allocation and rebalancing without ongoing oversight.

However, they may be less suitable for investors who want to customize their asset allocation, coordinate multiple accounts with different risk levels, or take a more hands-on approach to portfolio management. Reviewing your overall financial situation, time horizon, and comfort with market fluctuations can help determine whether a target date fund fits your strategy.

Ready to invest in a target date fund?

Check out these options for your portfolio.

Target Date Funds FAQ

Are target date funds good investments?

Target date funds can be appropriate for long-term investors who want a diversified, professionally managed portfolio aligned to a specific time horizon. Whether they are a good fit depends on your risk tolerance, financial situation, and desire for customization.

Can you lose money in a target date fund?

Yes. Target date funds are subject to market risk and can experience losses, even near or after the target date, because most maintain some exposure to stocks.

What's the difference between "to" and "through" retirement funds?

Funds designed "to" retirement typically reach their most conservative allocation at the target date. Funds designed "through" retirement may continue reducing equity exposure after the target date.

" id="body_disclosure--media_disclosure--675911" >Funds designed "to" retirement typically reach their most conservative allocation at the target date. Funds designed "through" retirement may continue reducing equity exposure after the target date.

Should I choose a different target date based on risk tolerance?

Some investors select a target date earlier or later than their expected retirement year to align with their preferred level of risk. Reviewing the fund's glide path can help determine whether the allocation matches your comfort with market fluctuations.

Can target date funds be used outside retirement accounts?

Yes, but they are most commonly used in tax-advantaged accounts such as 401(k)s and IRAs. In taxable accounts, investors should consider potential tax implications from underlying fund activity.