Who Owns Treasury Bonds—and Why Does It Matter?

When President Trump announced his sweeping Liberation Day tariffs back in April 2025, the U.S. Treasury bond market whipsawed in response, calling into question Treasuries' reputation as one of the world's safest, most stable assets.

Fixed income investors, in particular, were rattled by the volatility of Treasury prices and yields—and analysts were eager to know what was behind it. One potential answer: the expanding ownership of U.S. Treasuries by private investors.

A shifting landscape

The Federal Reserve, which doubled its holdings of Treasuries during the COVID-19 pandemic, has since stepped back and pared its holdings1 from mid-2022 through December 2025. At the same time, domestic and foreign private investors—including, but not limited to, hedge funds, individual households, money market funds, mutual funds, and nonprofits—increased their exposure and now account for 60% of the market, up from 37% in 2014.

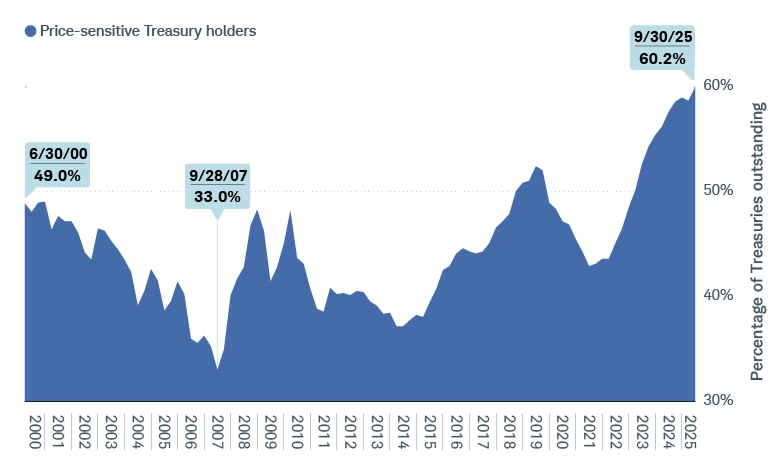

Shifting ownership

Private investors now hold the majority of U.S. Treasuries.

Source: Schwab Center for Financial Research with data from the Federal Reserve's "Z.1 Financial Accounts of the United States" report. Data from 9/30/2000 through 09/30/2025.

Price-sensitive Treasury holders include foreign private investors, households, insurance companies, money market funds, mutual funds, nonfinancial businesses, nonprofits, pension funds, and other domestic financial holders.

However, while the Fed, financial institutions, and foreign central banks and governments buy U.S. Treasuries to maintain market stability, manage liquidity, and satisfy a variety of policy objectives, private investors are primarily motivated by income and total return. Consequently, demand for Treasuries may decline if investors can find higher risk-adjusted returns elsewhere, potentially resulting in increased volatility.

If that happens, those who rely on U.S. Treasuries for their fixed income needs could experience much greater swings—in both their income and in the value of their portfolio holdings—particularly since the Congressional Budget Office is projecting federal budget deficits from 2025 through 2034 of more than $21 trillion.2 Because deficits drive the issuance of Treasury securities, this is likely to result in the net issuance of approximately $2 trillion in Treasuries annually over the next decade, potentially putting upward pressure on yields (and thus lowering prices) to attract buyers, especially if supply outpaces demand.

Complicating factors

What's more, leveraged hedge funds and stablecoin issuers are increasingly adding Treasuries to their holdings. (In fact, in July 2025 two stablecoin issuers became among the top holders of U.S. Treasury debt, surpassing some nation-states.) However, their buy-and-sell strategies, too, can differ greatly from the traditional buy-and-hold approach of most central banks and governments:

- Hedge funds, for example, borrow large sums to purchase Treasuries while simultaneously selling Treasury futures to profit from potential price differences. Extreme market disruptions, however, can force hedge funds to quickly sell their Treasury holdings to meet collateral requirements or investor redemptions, pushing Treasury yields even higher. Such was the case in March 2020 at the onset of the COVID-19 pandemic, according to Brookings, an economic think tank.3

- Stablecoins are designed to maintain a steady value—such as $1 per coin—and are backed by reserve assets like short-term Treasury bills. Be that as it may, cryptocurrencies are highly volatile, speculative instruments. They are not backed by any central bank, deposits are not protected by the Federal Deposit Insurance Corporation, and they are not securities shielded by the Securities Investor Protection Corporation. And because stablecoins are influenced by overall crypto sentiment,4 a market shock could force stablecoin issuers to sell their Treasury reserves when faced with sudden redemptions, further fueling volatility in the Treasuries market—and potentially causing the stablecoin itself to collapse.

Mounting competition

It's arguable that there's no safer alternative for income investors than U.S. Treasuries, given that they're backed by the full faith and credit of the U.S. government. That said, other nations are on the cusp of issuing more debt than they have in years, which could test the U.S. advantage. For instance:

- Germany and other NATO countries have committed to significantly increase their defense spending—to the tune of 5% of gross domestic product annually by 2035—with an expected rise in debt issuance.5

- Governments in developed countries—including the U.S.—were on track to issue a record $17 trillion in bonds in 2025 as the higher cost of refinancing existing debts pushed their interest obligations higher.6

Moreover, nearly half the outstanding bonds issued by member governments of the Organization for Economic Cooperation and Development (including the U.S.) will mature by 2027, and the new bonds that replace them could potentially pay much higher rates.7 Thus, the ongoing surge in the global supply of debt may force the U.S. government to pay higher yields to remain competitive.

What to consider now

Treasuries may be in for a bumpy ride, but it's unlikely to cost them their reputation as one of the most secure assets around. For those who hold individual bonds to maturity, there's not much to do.

For those who invest in Treasuries through ETFs and mutual funds, however, higher volatility could have an impact on not only coupon payments but also the prices of their underlying bonds. If you're in this camp, you may want to take a more active approach, including:

- Consider corporates: As of November 28, 2025, adding some exposure to investment-grade corporate bonds can get you attractive yields from companies with strong financials and relatively low credit risk, depending on the credit rating.

- Diversify with munis: Municipal bonds generally have high credit quality and, for investors in the top tax bracket, were offering tax-equivalent yields as of December 31, 2025, that were roughly on par with or potentially higher than those of corporates and Treasuries.

- Rebalance more often: Instead of rebalancing annually, you could instead rebalance anytime your allocations shift beyond their targets by, say, 5 percentage points. This helps ensure your allocations don't drift too far from your targets during periods of heightened volatility, so that your risk exposure continues to match your risk tolerance.

- Shorten up: Focusing on short- and intermediate-term maturities, which are less susceptible to price changes than longer-term Treasuries, can also help insulate your portfolio against extreme volatility.

1Federal Reserve Board, "Plans for Reducing the Size of the Federal Reserve's Balance Sheet," federalreserve.gov, 05/04/2022.

2Congressional Budget Office, "The Budget and Economic Outlook: 2025 to 2035," cbo.gov, 01/17/2025.

3Nellie Liang, "What's going on in the US Treasury market, and why does it matter?" brookings.edu, 04/14/2025.

4Victor Xing, "Stablecoins and Treasuries: A Fragile Funding Link Investors Can't Ignore," cfainstitute.org, 08/28/2025.

5Robin Fehrenbach, Jakob Flemming, and Julia Friedlander, "Waiting for the Big Bang: Executing the European Defense Build-Up in Germany," atlantik-bruecke.org, 09/29/2025.

6,7Paul Hannon, "Debt Issuance by Governments of Rich Countries to Hit Record High, OECD Says," wsj.com, 03/20/2025.

Discover more from Onward

Keep reading the latest issue online or view the print edition.