Why the Dollar Might Remain Supported

Key takeaways

- Elevated U.S. bond yields, the hawkish Fed pivot, and the relatively resilient U.S. economy may keep the dollar supported in the near term.

- While many other central banks have also pivoted to a hawkish bias, U.S. yields have generally increased more than other developed market government bond yields.

- The resilient U.S. economy should continue to attract capital, helping to support the dollar.

- Geopolitical risk remains a wild card. The recent re-escalation of the Iran war should support the dollar, while any de-escalation could reduce dollar demand.

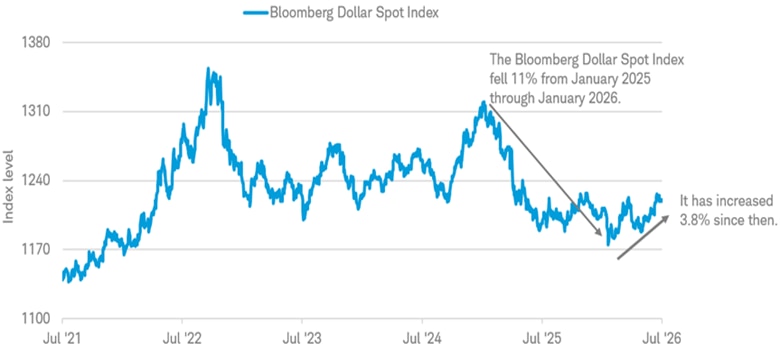

The dollar has rebounded lately after falling to its lowest level in nearly four years this past January. A lot has changed over the last few months, however, and much of the recent increase is likely due to the Federal Reserve's hawkish pivot.

Dollar rebound generally driven by hawkish Fed pivot

Source: Bloomberg.

Bloomberg Dollar Spot Index (BBDXY Index). Daily data from 7/10/2021 to 7/10/2026. The BBDXY tracks the performance of a basket of leading global currencies versus the U.S. dollar. Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

Coming into 2026, we expected the dollar to weaken gradually as the U.S. interest-rate advantage narrowed. Higher U.S. yields relative to those overseas tend to attract foreign capital and support the dollar. When that advantage declines, the dollar typically faces downward pressure.

We expected the Fed to lower rates gradually while most other developed-market central banks, aside from the Bank of Japan, held rates steady after largely completing their rate-cutting cycles. This could narrow the gap between U.S. and foreign yields, pointing to a modestly weaker dollar.

But that outlook has changed and we currently see three key factors that might keep the dollar supported:

- The Fed—along with other central banks—has shifted to a more hawkish monetary policy.

- The rising gap between U.S. and global bond yields. U.S. Treasury yields have risen sharply since the low in February.

- Stronger U.S. growth relative to other developed markets globally.

These forces may support the dollar in the near term, but they don't necessarily make the case for a much bigger rally. A larger move would likely require stickier inflation, stronger U.S. growth, or further widening in the U.S. yield advantage.

Geopolitical risk could complicate the longer-term case. The Iran war has been a wild card, and any escalation or de-escalation can affect the direction of the dollar, but we acknowledge that the situation is fluid and outcomes are highly uncertain.

The role of Fed policy

Fed policy is a key near-term driver of the dollar because it shapes expectations for short-term interest rates. When investors expect U.S. rates to stay high—or potentially move even higher—the dollar usually gets support since dollar-based assets might offer more attractive income than many foreign alternatives.

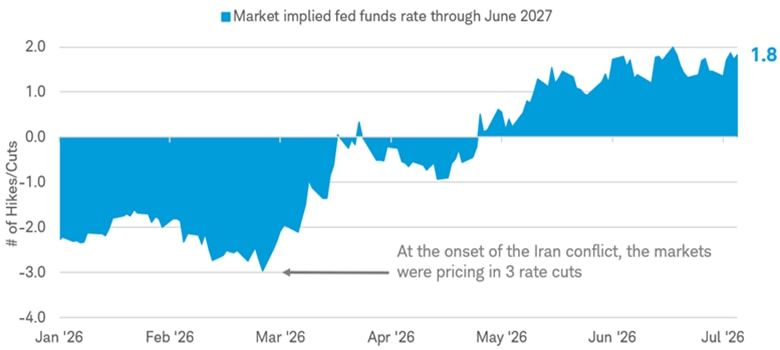

Expectations for Fed policy have shifted since earlier this year. Coming into the year, the fed funds futures market was pricing in two or three rate cuts this year, but expectations have shifted from cuts to hikes following the Iran war.

The chart below illustrates the number of 25-basis-point moves (up for a hike or down for a cut) by June 2027. The negative readings earlier this year implied rate cuts, but now the most recent reading of 1.8 implies 1.8 rate hikes by next June.

Fed expectations have shifted from cuts to hikes

Source: Bloomberg.

WIRP Implied Overnight Rate for the U.S. - Futures Model (US0ANM JUN2027 Index). Daily data from 1/1/2026 to 7/10/2026. This data represents the estimated forward rate for the United States using the futures model. Futures and futures options trading involves substantial risk and is not suitable for all investors. Please read the Risk Disclosure Statement for Futures and Options prior to trading futures products.

We aren't yet in the "hike this year" camp. We expect the Fed to remain patient—the recent inflationary impulse may have peaked with the price of oil down from recent highs, but it's not yet clear whether inflation is moving sustainably back to target. Whether the Fed actually hikes may be less important than the pivot away from potential cuts this year.

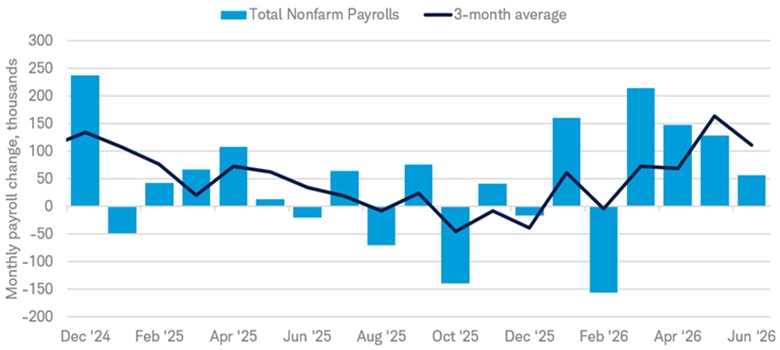

We believe the labor market—which isn't too hot or too cold—is also giving the Fed room to be patient. Hiring began picking up in March, but then the pace of job gains slowed in June. The unemployment rate has been steady recently but declined modestly in June because the participation rate fell—meaning workers took themselves out of the workforce. This mix doesn't necessarily call for rate cuts, but we don't believe it means there will be further tightening in the coming months.

June payrolls disappointed, but job growth remained positive

Source: Bloomberg.

U.S. Employees on Nonfarm Payrolls Total MoM Net Change SA (NFP TCH Index). Monthly data from 12/31/2024 to 6/30/2026.

Fed policy remains supportive for the dollar, but that support may have its limits. If the inflation outlook improves, or hiring slows, markets may shift from pricing in hikes to a longer hold—in-line with our view—and may eventually begin pricing in policy easing. In that scenario, the dollar would likely have a harder time extending its gains.

The Fed isn't the only central bank that has turned more hawkish recently. The European Central Bank hiked rates last month in response to the rise in inflation, and the Bank of Japan has been gradually raising rates since early 2024. Even against that backdrop, the interest rate differentials—or yields offered on U.S. Treasuries relative to other developed markets—have been increasing.

The 2-year Treasury yield has risen to the 4.2% range, its highest level in more than a year and up over 80 basis points since before the Iran war began in February. That's a larger increase than a blended yield that averages the 2-year yields for Germany, Japan, and the United Kingdom in that same period.

US 2-year Treasury yields remain above other developed markets

Source: Bloomberg.

U.S. Generic Govt 2-year yield (USGG2YR Index), and average yield of the 2-year German yield (GTDEM2Y Govt), the 2-year Japanese yield (GTJPY2Y Govt), and the 2-year United Kingdom yield (GTGBP2Y Govt). Daily data from 7/8/2021 to 7/8/2026. Past performance is no guarantee of future results.

The chart below shows the yield differential between the two series above, highlighting that U.S. yields remain high compared with other large developed markets. When U.S. government bonds offer higher income alongside a generally more resilient economy, demand for dollar-based assets can stay firm, generally helping to support the dollar.

U.S. yield advantage has widened since April

Source: Bloomberg.

U.S. Generic Govt 2-year yield (USGG2YR Index), and average yield of the 2-year German yield (GTDEM2Y Govt), the 2-year Japanese yield (GTJPY2Y Govt), and the 2-year United Kingdom yield (GTGBP2Y Govt). Daily data from 7/8/2021 to 7/8/2026. Past performance is no guarantee of future results.

The U.S. economic growth outlook also favors the dollar

The U.S. economy has slowed a bit over the last few quarters, with fourth quarter 2025 and first quarter 2026 gross domestic product (GDP) rising 0.5% and 2.1%, respectively, on an annualized basis, which is down from the previous two quarters. But on a year-over-year basis, GDP has grown by 2% or more for 13 straight quarters.

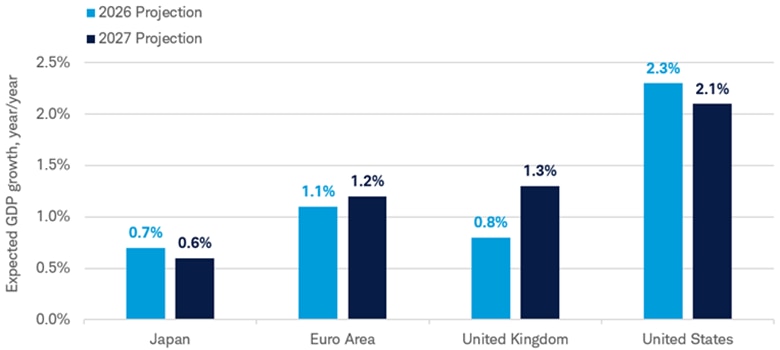

U.S. growth is expected to outperform many other developed markets. Forecasts from the International Monetary Fund (IMF) show that the U.S. economy is expected to grow at a faster rate than Japan, the Euro area, and the United Kingdom in both 2026 and 2027. Relative growth of that kind helps support confidence in U.S. assets, potentially attracting capital and supporting the dollar.

U.S. growth is expected to lead other developed markets

Source: International Monetary Fund (IMF) and World Economic Output, April 2026.

Light blue columns represent the expected GDP growth rate for 2026 and the dark blue columns represent the expected GDP growth rate for 2027.

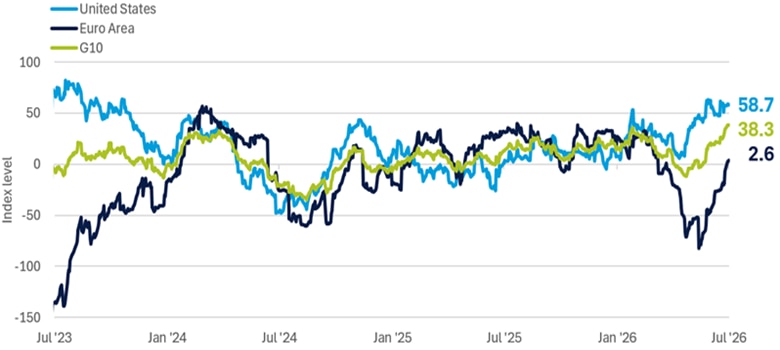

We're also seeing the stronger growth story in real time. The U.S. has generally been seeing positive economic surprises over the last few months—and at a higher rate than the euro area and the Group of Ten (G10).

Positive U.S. economic surprises outpace global peers

Source: Bloomberg and Macrobond.

ECO U.S. Surprise Index (ECSURPUS Index), Citigroup Economic Surprise Index – Eurozone (CESIEUR Index), Citigroup Economic Surprise Index – G10 (CESIG10). Daily data from 7/9/2023 to 7/9/2026.

A potential risk is that the U.S. growth advantage narrows or that positive surprises turn to negative surprises. Other central banks are also dealing with inflation pressures, and yields have moved higher in some markets. If stronger growth abroad pulls up foreign bond yields, the dollar could lose some of its relative appeal.

This doesn't suggest the dollar is headed for a sharp decline, but it does mean the dollar needs more than just high U.S. yields—it might also need the U.S. to keep looking decidedly stronger than the rest of the developed world.

Fiscal and geopolitical risks

There are risks, of course, like geopolitical and fiscal risks.

Geopolitical uncertainty—like the re-escalation in Iran—can help the dollar in the short run. When global uncertainty rises, investors often move toward highly rated, easy-to-trade assets, and the dollar still plays that role. But if tensions de-escalate, the dollar may lose support as investors may no longer feel the need to own a safe-haven currency. The situation in Iran is fluid. We don't know what will happen, but we do know that both good news and bad news could drive the dollar's direction.

Our fiscal situation also poses a risk. The U.S. is running large deficits, interest costs are rising, and Treasury supply remains heavy. Despite concerns to the contrary, we don't believe that points to a potential dollar crisis. The U.S. still has large, highly liquid capital markets and no clear replacement for the dollar's reserve-currency role. But these appear to be more long-term risks than short-term risks.

What to consider now

Elevated U.S. bond yields, the hawkish Fed pivot, and the relatively resilient U.S. economy may keep the dollar supported in the near term, but we don't expect a big move higher.

If inflation cools, hiring slows, or foreign yields rise, the dollar's rate advantage could narrow. Fiscal concerns add another constraint, especially if higher Treasury yields reflect more than steady growth and attractive income. And while the U.S. still has large, highly liquid markets and no clear replacement for the dollar's reserve-currency role, the recent rebound does not look like the start of a new, extended dollar bull market.

Global bond investing appears less favorable when the dollar is expected to hold steady or rise modestly since it may limit potential appreciation in local currencies. Developed market government bonds generally offer lower yields than U.S. bonds, so investors typically sacrifice income when considering foreign bond alternatives.